- Monthly index tracks currency misalignment based on latest market rates

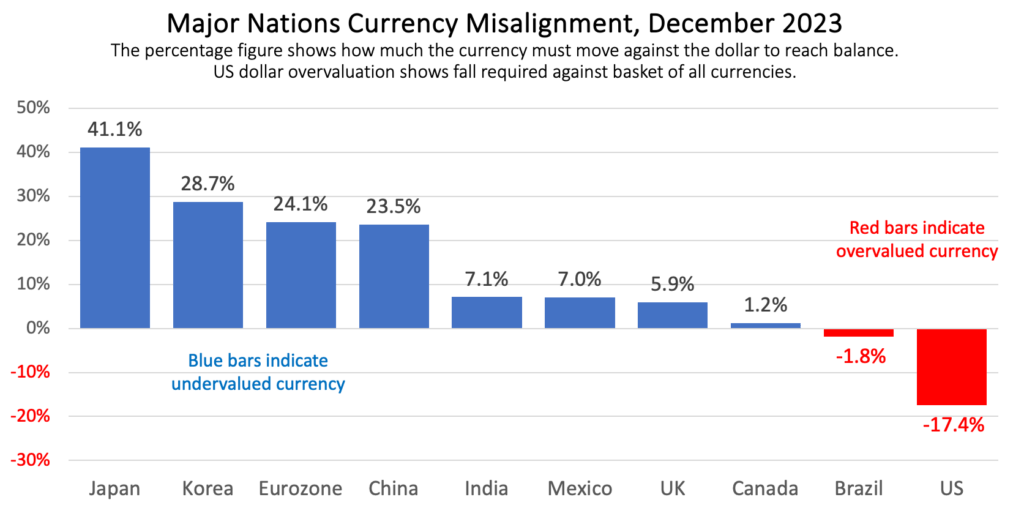

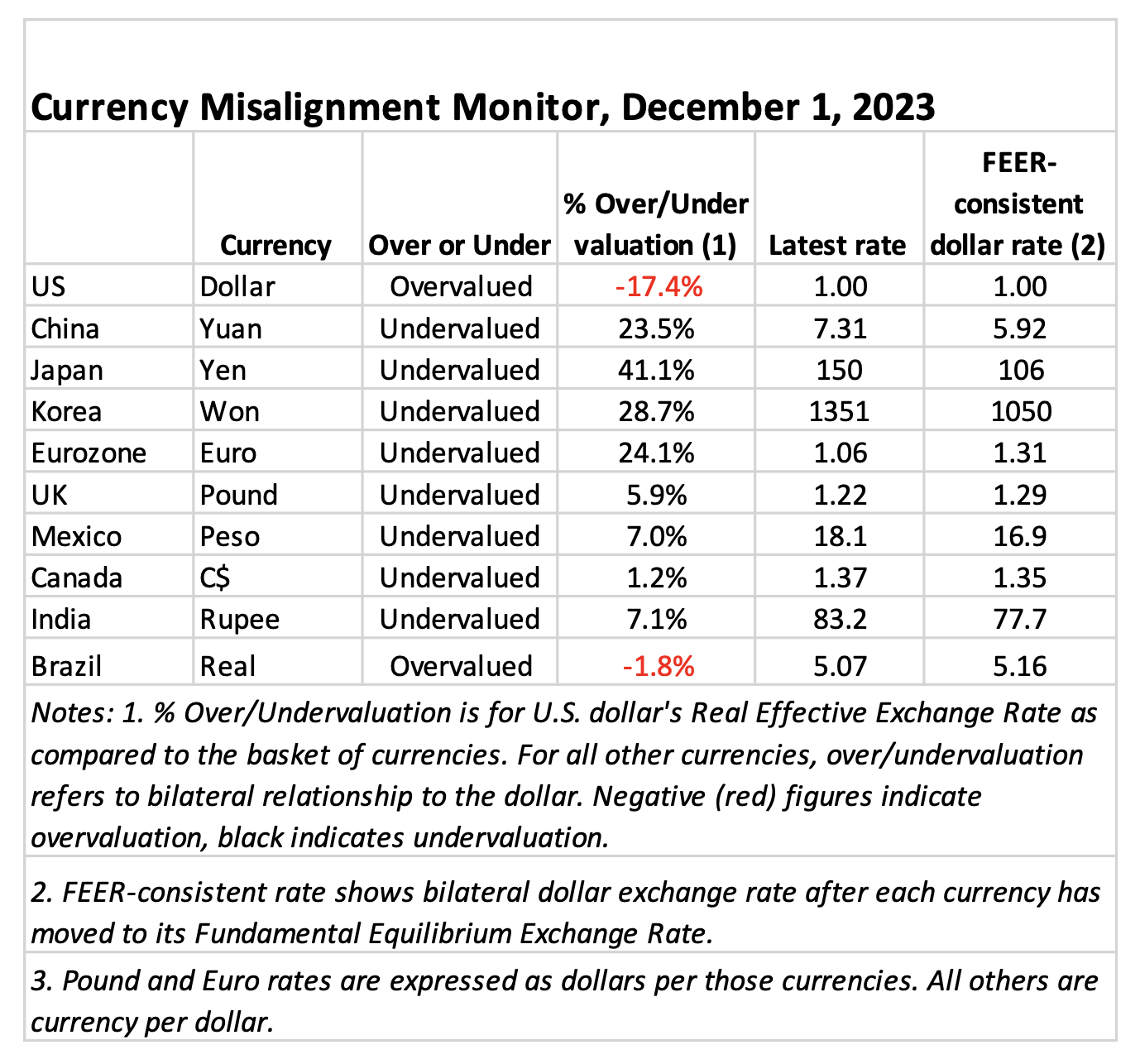

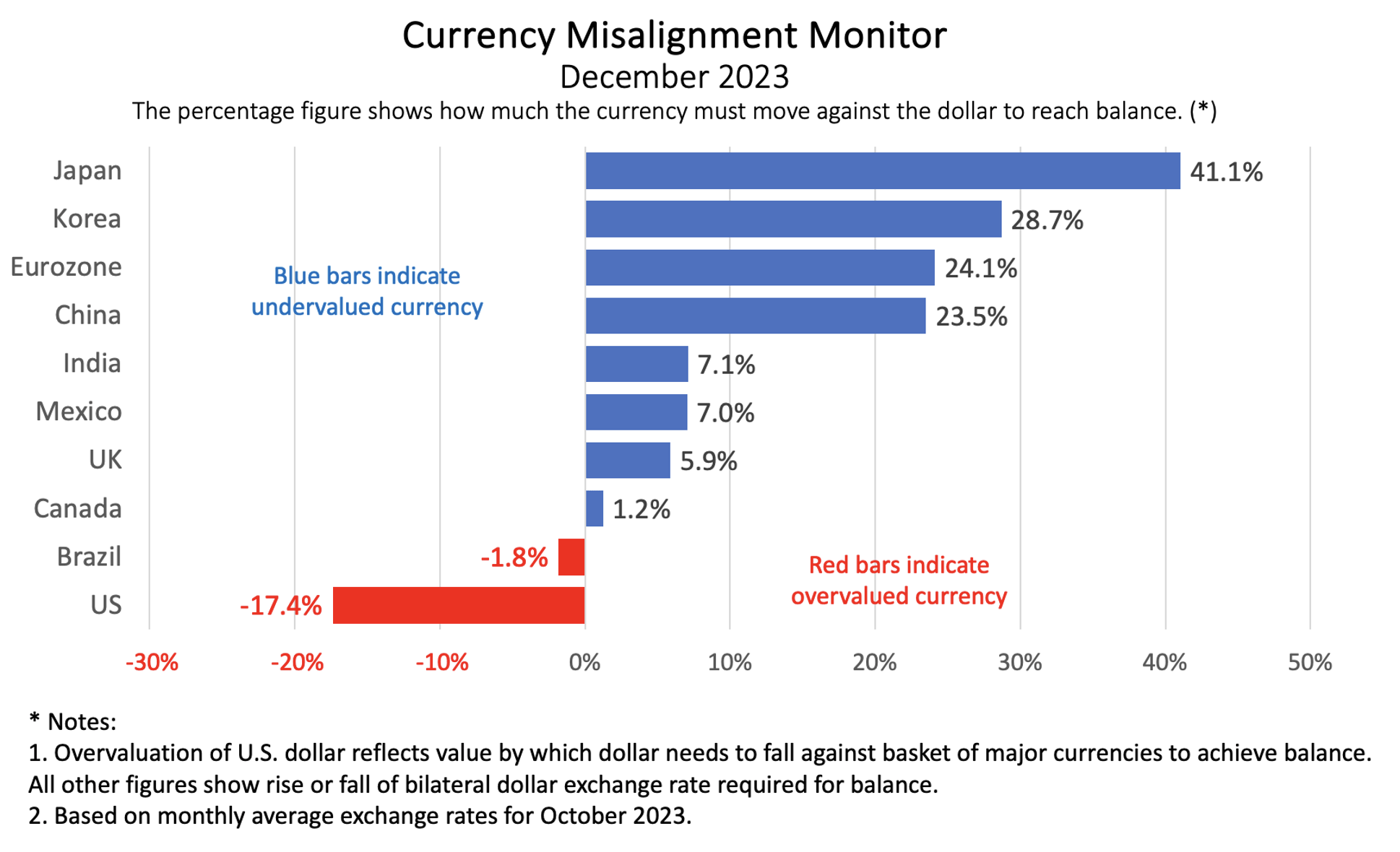

- Dollar overvaluation moves up again, to 17.4% on robust U.S. economic growth

- Japanese yen undervaluation at 41.1% as yen reaches 150 to the dollar.

- Chinese yuan undervaluation edges up to 23.5%, as capital outflows are said to be driving the yuan down.

- New IMF forecast showing China’s and Japan’s large current account surpluses shrinking by 2028 may be excessively optimistic.

- CMM is a partnership between the Coalition for a Prosperous America (CPA) and the Blue Collar Dollar Institute (BCDI).

The December Currency Misalignment Monitor – a monthly index that tracks currency misalignment among major economies – found dollar overvaluation edging up once again, to 17.4% against the basket of 33 other currencies included in our model. The overvalued dollar makes imports less expensive in the U.S. and our exports more expensive on world markets. Our overvalued currency is the biggest single contributor to our huge trade deficit, set to come in at more than $750 billion this year.

As in previous months, China’s and Japan’s currencies are severely undervalued against the dollar, by 23.5% for the Chinese yuan and 41.1% for the yen. That undervaluation supports their export-led growth strategies.

These estimates are based on new forecasts from the International Monetary Fund (IMF) contained in its October World Economic Outlook publication. Our estimates of over- and undervaluation are derived from applying our model to the IMF forecasts to calculate what exchange rates would be needed to set all major world economies to balance in the current account (equivalent to the trade balance plus investment income and foreign remittances) five years from today. The exchange rate model was developed at the Peterson Institute. However the original model only called for exchange rate adjustment if the 2028 current account balance exceeded 3% of the nation’s GDP in 2028. That’s a large number–$810 billion in the case of the U.S.

Our model targets zero current account balances in 2028 to demonstrate what sort of exchange rate adjustments would be necessary to eliminate the large imbalances between persistent deficit countries like the U.S. and surplus countries like China, Japan, and Germany. Standard economic theory says that exchange rates should be set at levels to balance a nation’s current account over the long term. Further, standard theory suggests that advanced economies like the U.S. should consistently run modest surpluses to provide for capital outflows to invest in emerging economies, which are traditionally capital poor and offer good investment opportunities.

But for decades, the opposite has been the case. Surplus nations like China and Japan manage their exchange rates to generate persistent surpluses on trade and current account bringing in foreign exchange which they then invest overseas. Advanced countries like the U.S. become the main destination for those capital flows, forcing them into persistent deficit. Deficits and surpluses in the major nations have become self-reinforcing phenomena.

Japan provides a good example of how an undervalued exchange rate can support exports to the U.S. The Japanese yen is currently around 150 to the dollar while our model says it should be at 106. Today Toyota might sell a Japanese-produced car in the U.S. at $40,000 based on the current 150 exchange rate. If the yen rate moved to its equilibrium rate of 106, then to achieve the same 6 million yen sales price would require raising the U.S. price to $57,000, which would either cut back dramatically on Toyota’s U.S. sales or reduce Toyota’s profits if it attempted to hold the U.S. price to $40,000.

The new IMF forecasts raise another interesting question over our valuation methodology. The October forecasts show Japan’s current account surplus declining from the 2021 level of 3.9% of Japan’s GDP to 3.2% in 2028. But it was back in 2021 when the yen began its steep fall from around 105 to the dollar to today’s 140-150 range. That depreciation should increase Japan’s exports and its current account surplus.

Similarly, China’s current account surplus is forecast to fall from 2.0% in 2021 and 1.5% this year to only 0.68% in 2028. The IMF has a history of being optimistic in its forecasts, perhaps because it does not want to provoke member nations by publishing alarming forecasts. However, if those forecasts are over-optimistic, and the current account surpluses in the out-years turn out larger, then the currencies are even more severely undervalued and a greater rise in their value against the dollar than that shown in our current Misalignment Monitor would be needed to bring their surpluses down to zero.

For the United States, the IMF forecast shows the current account balance improving from this year’s -3.0% to -2.4% in 2028. Since the IMF forecast shows U.S. GDP rising more rapidly than other large nations in the next couple of years, one could expect that a rising GDP will raise U.S. consumption and suck in more imports, leading to an even worse current account balance.

Of course, it’s hard to forecast figures like current account balances five years out, so the Currency Misalignment Monitor is not intended to contain precise recommendations of the correct exchange rates, but more ballpark figures and a demonstration of the severe misalignment that exists today.

On a more positive note, the current exchange rates in this month’s Monitor are based on Bank of International Settlements average exchange rates for the month of October, the latest published figures. The U.S. dollar has edged down slightly during November, as international investors begin to think that the Federal Reserve has finished raising interest rates and the U.S. is now close to the targeted 2%. However, a slide of a couple of points in U.S. dollar overvaluation will not alter the fundamental, longstanding problem of a trading disadvantage with countries with undervalued currencies.

Table 1. Currency valuations from the Currency Misalignment Monitor, December 2023

The CMM is based on a mathematical model in which 34 major currencies all move simultaneously to bring global current accounts into balance over a five-year time horizon. If the dollar had to move on its own, the dollar would need to move by approximately twice as much, or around 25%, to achieve fair value for the U.S. economy, i.e., a value that eliminated the current account deficit. The current account deficit is dominated by the trade deficit, but also includes some other financial flows into and out of the U.S.

METHODOLOGY

The Currency Misalignment Monitor is based on pioneering work done by William Cline at the Peterson Institute for International Economics. The Cline model, also known as SMIM for Symmetric Matrix Inversion Method, uses IMF forecasts for current account balances for 34 nations to derive a simultaneous solution for all exchange rates that will minimize national current account balances, including surpluses and deficits. The CMM uses this methodology. However, the Cline version sets a target of plus or minus 3% of GDP for each nation’s current account. We believe this is too flexible for a properly functioning global trading system. Our model sets a target of 0% current account balance for each nation. Most nations do not achieve 0% in year five, but the model seeks to get them as close to zero as possible and in so doing gives us a realistic sense of each currency’s over or undervaluation.

Note also that this methodology is dependent on IMF forecasts, which currently run from 2023 data out to 2028. The IMF has a history of optimism, including for example expectations that the U.S. current account deficit and the China surplus will both contract over time. If those forecasts turn out to be over-optimistic, then the misalignment estimates in the Monitor could well be understated. Nevertheless the Cline SMIM model is an innovative method for incorporating a large amount of global data into a single model.

The Currency Misalignment Monitor (CMM) is published in partnership between the Coalition for a Prosperous America (CPA) and the Blue Collar Dollar Institute (BCDI).