- Monthly index tracks currency misalignment based on latest market rates

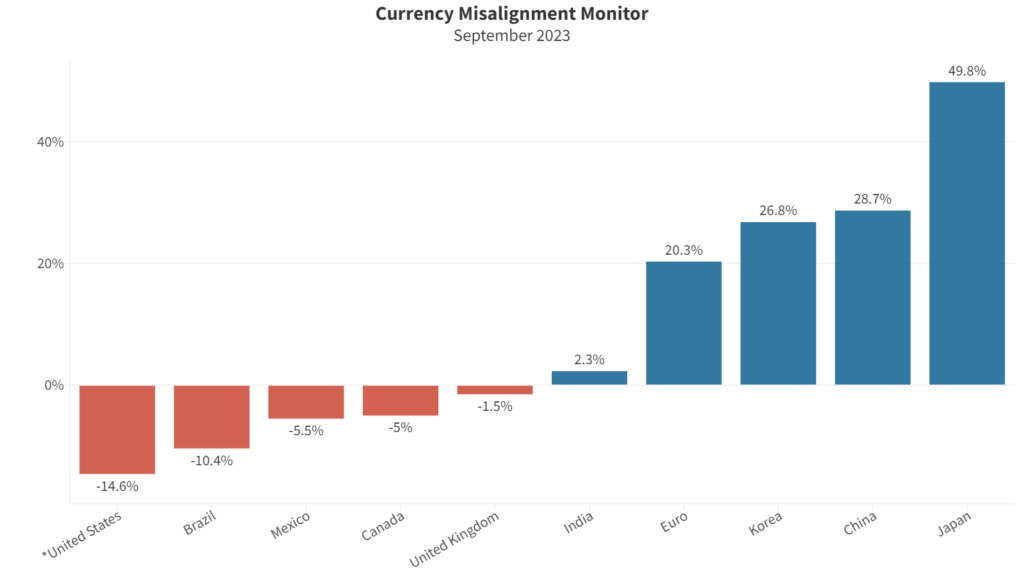

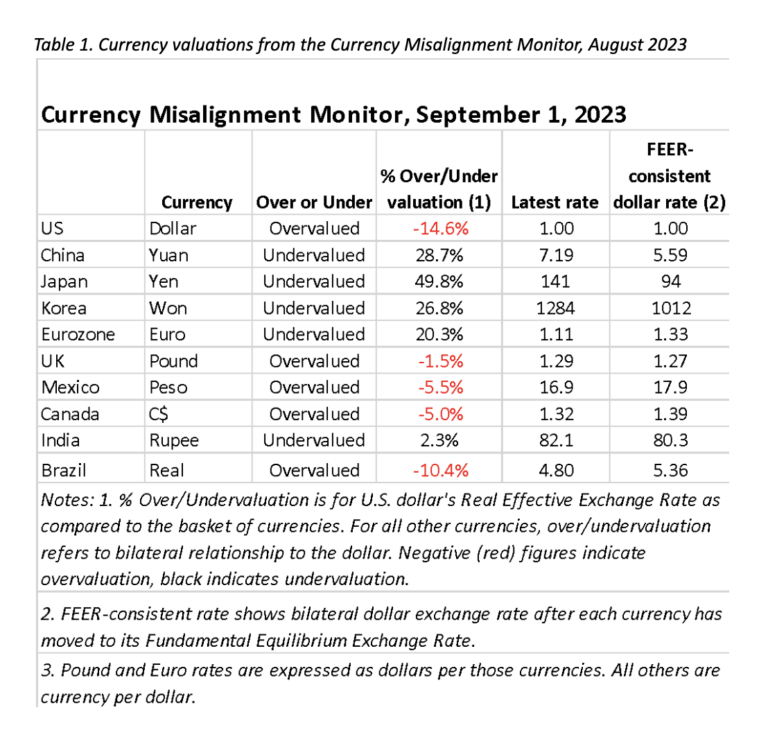

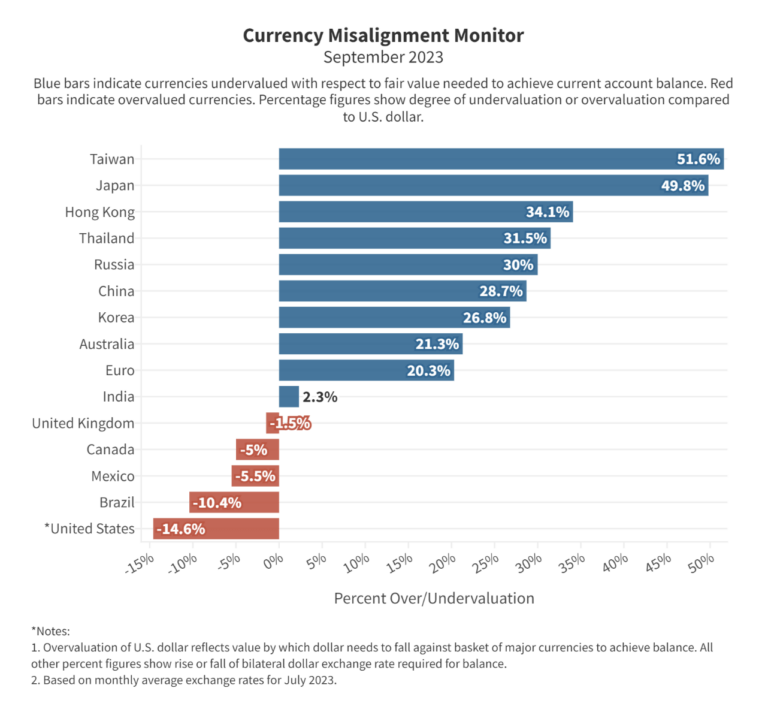

- Dollar overvaluation ebbs slightly to 14.6% as U.S. inflation moderates

- Japanese yen, Chinese yuan, Korean won, Eurozone euro all enjoying 20%+ undervaluation against the dollar

- Chinese yuan dollar undervaluation reaches 28.7% as investors flee weak Chinese economy

CMM is a partnership between the Coalition for a Prosperous America (CPA) and the Blue Collar Dollar Institute (BCDI).

The U.S. dollar fell slightly in our currency model, with overvaluation declining six tenths of a percentage point to 14.6% in this month’s CMM. The data used in our model includes Bank of International Settlements (BIS) monthly average real exchange rates, and the latest available data is for July. The dollar declined in July on a small 0.1% rise in the Producer Price Index and other signs that inflation was coming under control. But in August, signs of a strengthening U.S. economy put further upward pressure on the dollar, which will extend the dollar’s huge overvaluation, expected to be visible in next month’s report. While inflation does appear to be coming under control, other recent data points showing strong consumer spending and a tight labor market raise the possibility of further interest rate increases at the Federal Reserve’s September meeting, putting upward pressure on the dollar once again.

Meanwhile, Asian currencies continue to be steeply undervalued against the dollar, supporting their exports into the U.S. market and creating competitive difficulties for U.S. producers. The Chinese yuan is hitting lows not seen since the 2008 recession, as China eases its domestic interest rates to help out debtors like the large Chinese property companies, some of them teetering on the edge of bankruptcy. A lower yuan supports Chinese exports to other markets, an essential support for China given that the Chinese Communist Party continues to resist boosting internal Chinese demand.

While the Chinese government struggles against possible recession and debt-fueled meltdown, the Japanese government is fighting excessive inflation (3.1% in July, a high figure for Japan). In July, the Bank of Japan announced it would allow yields on long-term government bonds to rise as high as 1%. This historic move produced a jump in the yen, which lasted only a few days. The yen rose above 140 to the dollar before tumbling back to the 145 range, suggesting it will appear even more undervalued in next month’s Currency Misalignment Monitor.

Each of these nations’ individual problems suggest to investors that the world economy is on an unstable footing, encouraging them to increase their holdings of dollar assets, putting upward pressure on the dollar. The U.S. economy’s strength, and confidence that Fed chairman Jerome Powell has a firm focus on getting inflation under control further encourage investing in dollar assets. All of this is bad news for U.S. manufacturers and farmers, who must compete against foreign producers with a currency handicap that we pinpoint at 14.6% on average, but much worse against specific countries like China, which benefit from their own undervaluation on top of dollar overvaluation.

Our model uses BIS and International Monetary Fund data and forecasts to estimate the current account surpluses and deficits of 34 major nations five years from now (2028), and what movement would be required in each exchange rate now to bring those current accounts into balance in five years. In a deficit nation like the U.S., a lower dollar boosts exports and reduces imports, allowing the current account deficit to fall. In a surplus nation like China, the reverse process would occur: a higher yuan would reduce exports and increase imports, wiping out the surplus within five years.

The CMM is based on a mathematical model in which 34 major currencies all move simultaneously to bring global current accounts into balance over a five-year time horizon. If the dollar had to move on its own, the dollar would need to move by approximately twice as much, or around 25%, to achieve fair value for the U.S. economy, i.e. a value that eliminated the current account deficit. The current account deficit is dominated by the trade deficit, but also includes some other flows into and out of the U.S.

METHODOLOGY

The Currency Misalignment Monitor is based on pioneering work done by William Cline at the Peterson Institute for International Economics. The Cline model, also known as SMIM for Symmetric Matrix Inversion Method, uses IMF forecasts for current account balances for 34 nations to derive a simultaneous solution for all exchange rates that will minimize national current account balances, including surpluses and deficits. The CMM uses this methodology. However, the Cline version sets a target of plus or minus 3% of GDP for each nation’s current account. We believe this is too flexible for a properly functioning global trading system. Our model sets a target of 0% current account balance for each nation. Most nations do not achieve 0% in year five, but the model seeks to get them as close to zero as possible and in so doing gives us a realistic sense of each currency’s over or undervaluation.

Note also that this methodology is dependent on IMF forecasts, which currently run from 2023 data out to 2028. The IMF has a history of optimism, including for example expectations that the U.S. current account deficit and the China surplus will both contract over time. If those forecasts turn out to be over-optimistic, then the misalignment estimates in the Monitor could well be understated. Nevertheless the Cline SMIM model is an innovative method for incorporating a large amount of global data into a single model.

The Currency Misalignment Monitor (CMM) is published in partnership between the Coalition for a Prosperous America (CPA) and the Blue Collar Dollar Institute (BCDI).