- Monthly index tracks currency misalignment based on latest market rates

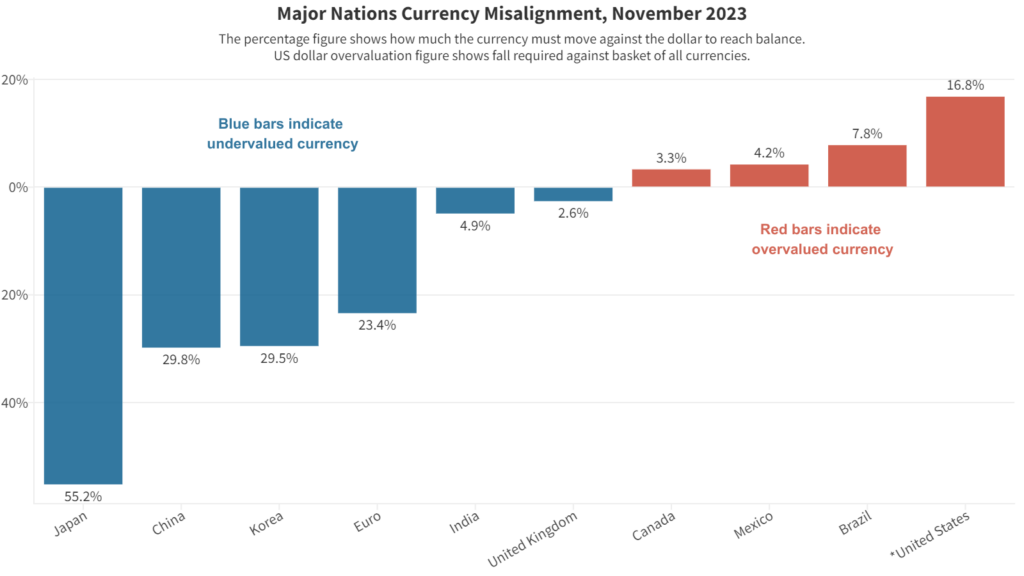

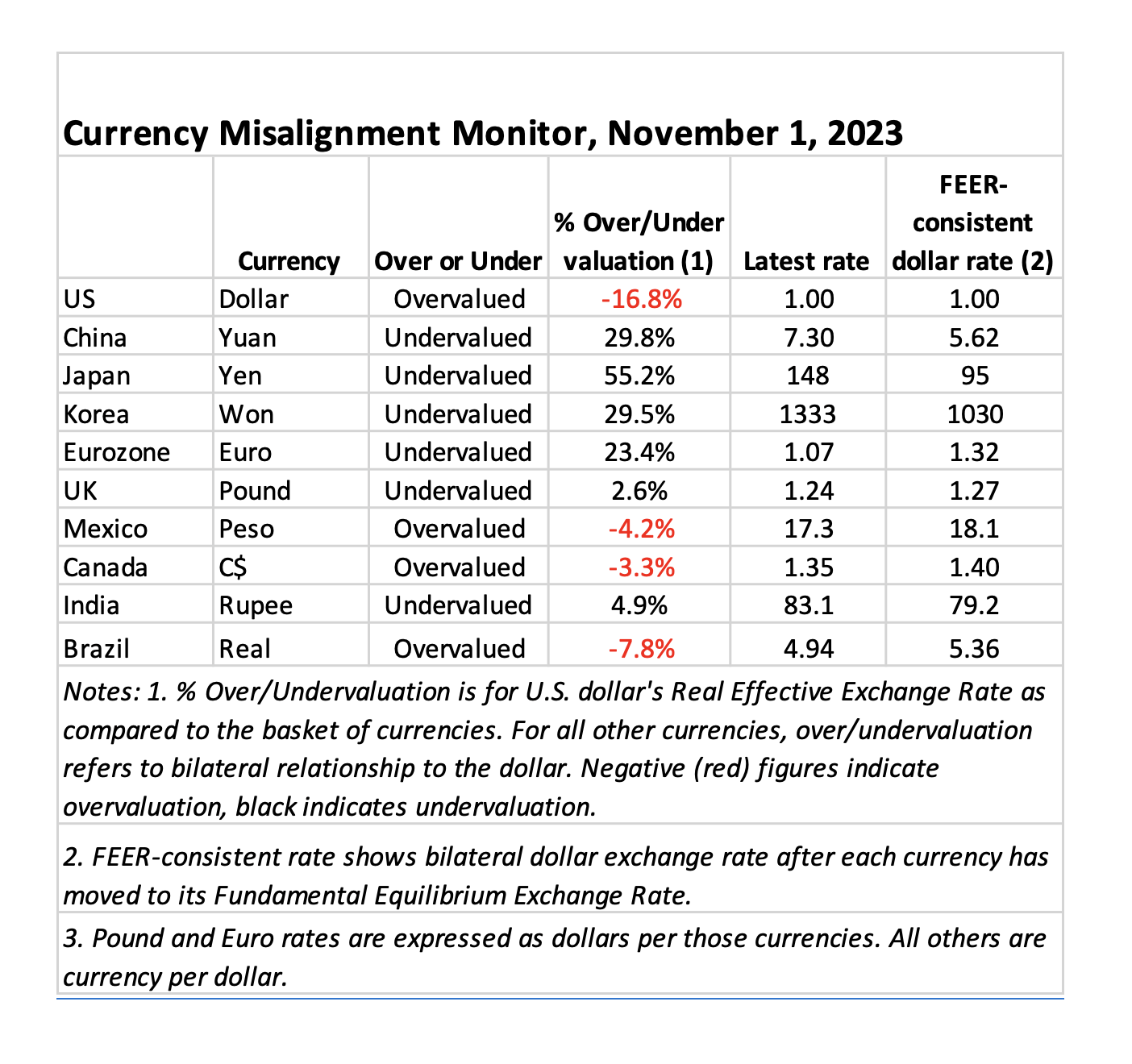

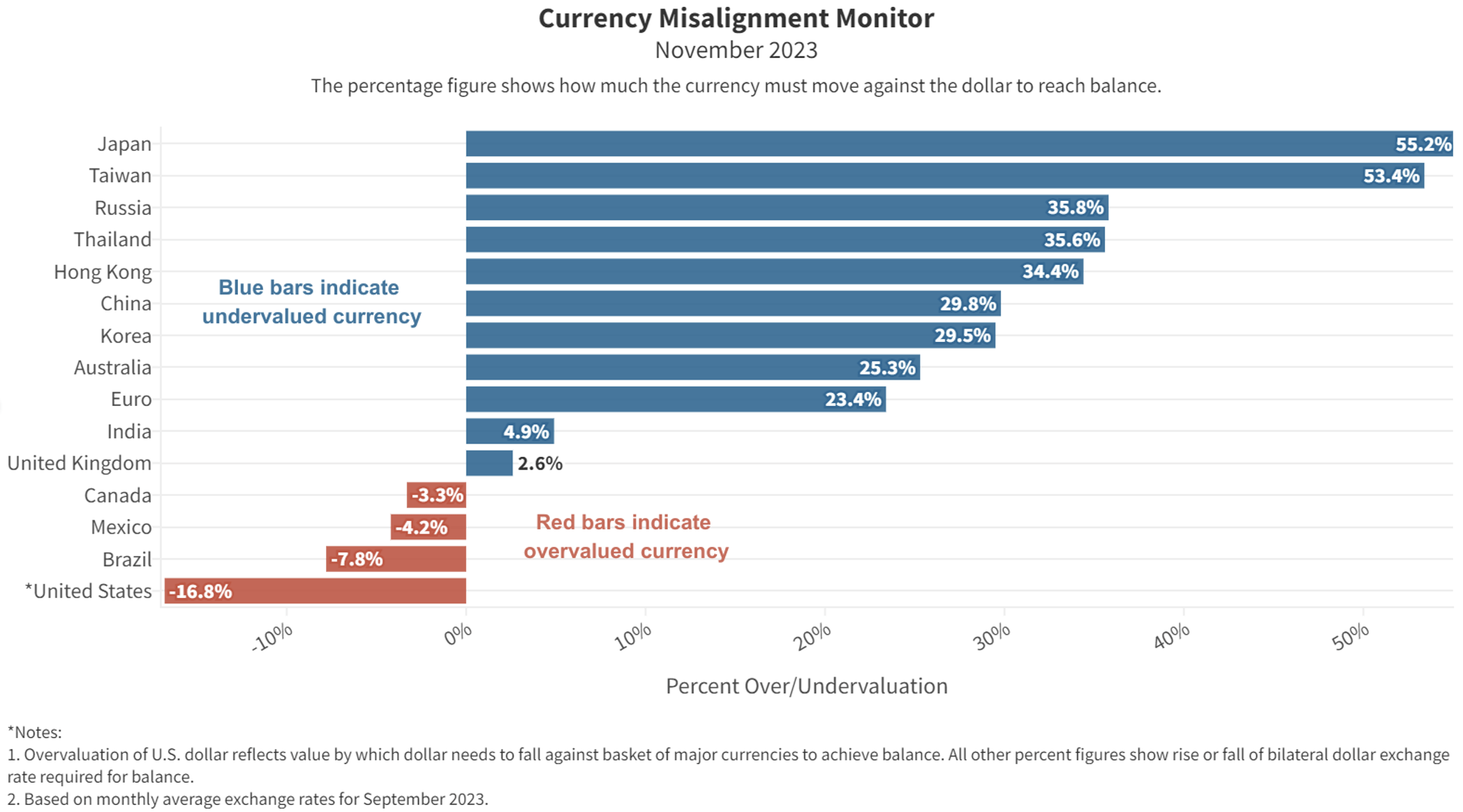

- Dollar overvaluation rises further, to 16.8% on robust U.S. economic growth

- Japanese yen undervaluation reaches 55.2%

- Chinese yuan undervaluation edges up to 29.8%, further expanding China’s trade advantage

- CMM is a partnership between the Coalition for a Prosperous America (CPA) and the Blue Collar Dollar Institute (BCDI).

The November Currency Misalignment Monitor – a monthly index that tracks currency misalignment among major economies – found dollar overvaluation rising further, to reach 16.8% against the basket of 33 other currencies included in our model.

That number underplays the true disadvantage that U.S. producers are suffering. For the major importing nations into the U.S., the U.S. handicap has expanded. Japan’s undervaluation has reached a new record level of 55.2%. According to the CMM model, which is based on official data from the International Monetary Fund and the Bank for International Settlements (BIS), a fair exchange rate for Japan would be 95 yen to the dollar instead of the BIS’s September average of 148 (or the nearly identical 149 figure as at the end of October). China’s undervaluation (29.8%) has also expanded. Euro undervaluation reached 23.4% in today’s CMM, which indicated an equilibrium rate of $1.32 for the euro, compared with recent euro exchange rates in the $1.06-$1.08 range.

The relentless rise of the dollar is due primarily to the positive economic outlook in the U.S. Last week’s strong Q3 gross domestic product growth figure of 4.9% was surprisingly high, but even before that, there were other indications of a strong economy, including recent data on consumer spending and jobless claims. In addition, the rise in long-term U.S. interest rates, coupled with comments by Federal Reserve Chairman Jerome Powell that he expects to let high interest rates continue as long as inflation is above the 2% target, have made international investors more willing to buy dollars and dollar assets to enjoy the high yield.

Meanwhile, greater uncertainty has made foreign currencies less attractive to the international investment community. Japan is fighting high inflation, while weaker economic growth in the European Union has undermined the case for holding euro assets. On top of all this, geopolitical uncertainty rose following the Hamas raid on Israel on October 7th. Fears of higher oil prices or even a regional war drive investors towards safety, which means dollar assets.

All these trends are increasing the plight of U.S. manufacturers and farmers who have to compete with foreign imports without the benefit of an undervalued currency. Standard economic theory suggests that with last year’s U.S. trade deficit at a record $951 billion, and a goods-only trade deficit at a record $1.18 trillion, those deficits should have exerted downward pressure on the U.S. dollar. Instead, the dollar, already overvalued at the start of this year, has continued to rise.

Table 1. Currency valuations from the Currency Misalignment Monitor, November 2023

The CMM is based on a mathematical model in which 34 major currencies all move simultaneously to bring global current accounts into balance over a five-year time horizon. If the dollar had to move on its own, the dollar would need to move by approximately twice as much, or around 25%, to achieve fair value for the U.S. economy, i.e. a value that eliminated the current account deficit. The current account deficit is dominated by the trade deficit, but also includes some other financial flows into and out of the U.S.

METHODOLOGY

The Currency Misalignment Monitor is based on pioneering work done by William Cline at the Peterson Institute for International Economics. The Cline model, also known as SMIM for Symmetric Matrix Inversion Method, uses IMF forecasts for current account balances for 34 nations to derive a simultaneous solution for all exchange rates that will minimize national current account balances, including surpluses and deficits. The CMM uses this methodology. However, the Cline version sets a target of plus or minus 3% of GDP for each nation’s current account. We believe this is too flexible for a properly functioning global trading system. Our model sets a target of 0% current account balance for each nation. Most nations do not achieve 0% in year five, but the model seeks to get them as close to zero as possible and in so doing gives us a realistic sense of each currency’s over or undervaluation.

Note also that this methodology is dependent on IMF forecasts, which currently run from 2023 data out to 2028. The IMF has a history of optimism, including for example expectations that the U.S. current account deficit and the China surplus will both contract over time. If those forecasts turn out to be over-optimistic, then the misalignment estimates in the Monitor could well be understated. Nevertheless the Cline SMIM model is an innovative method for incorporating a large amount of global data into a single model.

The Currency Misalignment Monitor (CMM) is published in partnership between the Coalition for a Prosperous America (CPA) and the Blue Collar Dollar Institute (BCDI).