A recent House Financial Services subcommittee hearing on the dollar focused primarily on how Washington uses it to enact sanctions on countries like Russia, as well as the risks of emerging economies moving away from the dollar in order to gain reprieve from sanctions regimes. At the heart of the debate was if such moves would weaken the dollar’s dominance in the world, long assumed to be an important source of American geopolitical might.

CPA believes that industrial dominance is what gives America its geopolitical might and that an over-valued dollar makes us weaker. The organization also believes that a dollar that is widely-used in the world can be managed to a competitive and stable exchange rate that no longer disadvantages our real economy.

All the hearing witnesses agreed that there is no near-term risk of the dollar losing its so-called “reserve” status in the short or medium term so long as the U.S. economy was seen as strong and inflation was under control. There were a few quotable moments in the June 7 hearing, titled “Dollar Dominance, Preserving the U.S. Dollar’s Status as the Global Reserve Currency”, that would be of interest to some CPA members.

“The benefits of the dollar as global reserve currency are not without cost,” said Tyler Goodspeed, one of the five witnesses and a Kleinheinz Fellow from the Hoover Institution at Stanford University. [Testimony]

“Lower interest rates means lowers returns on savings, and it damages U.S. companies that compete against imported goods and services,” said Goodspeed. “As demand for the dollar increases in response to adverse events worldwide, that demand leads to a stronger dollar and it hurts the competitiveness of U.S. exporters who will have an increased competitive disadvantage at times when global economic conditions are causing a spike in the dollar’s value.”

Goodspeed said in his opening statement that some 84% of global trade was conducted in dollars; the euro was a distant second. Central banks, mostly in the developing world, hold currencies of foreign nations, including bonds, as a means to protect their own currency against speculative attacks and as a message to global bondholders that they can pay the interest on their sovereign debt owed to them in the form of interest payments. The dollar dominates here, though this is in decline.

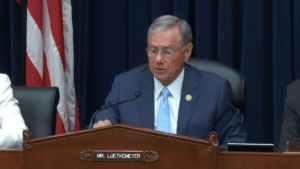

“A strong dollar lowers the cost of imported goods,” said Subcommittee Chairman Blaine Luetkemeyer (R-MO), recognizing the harm it causes US producers and workers

CPA chief economist Jeff Ferry is sending written testimony to the Subcommittee on National Security, Illicit Finance and International Financial Institutions this week. CPA favors a “managed” dollar, which might include the Federal Reserve or Treasury taking similar steps to emerging market banks where they buy or sell dollars and short-term debt in order to influence the exchange rate. Brazil and Mexico are known to do this regularly, for example.

Marshall Billingslea, Senior Fellow at the Hudson Institute, said China can retaliate against dollar sanctions. “We have seen a drop in China’s stock indexes and are seeing reduction in investment in China overall,” he told the Committee. “We need to ensure that our largest investment banks can withstand a shock that would arise from a crisis with China. China owes over $5 billion to Western investors that they could easily hold hostage in a sanctions war. We need to engage with our pension funds so they know the risk of keeping those securities in China,” Billingslea, a former Treasury official in the Trump administration, told Congress this week.

Although not the main focus of Wednesday’s hearing, China came up often. It is seen as the only country that can really entice other markets to move away from the dollar. It is clear Washington wants to keep the dollar as the go-to currency for world trade and in global central bank forex accounts.

No one thought, however, that the renminbi was a serious challenger to the U.S. at this time, though many in government and media have worried that this is about to change. The hearing witnesses debunked this fear stating that China’s bilateral agreements with, for example, Saudi Arabia to buy oil in yuan have not and will not meaningfully affect dollar dominance.

The renminbi is also unlikely to grow as a global currency because Beijing is interested in maintaining a stable, and undervalued currency. Making it rival the dollar with more financial transactions would mean a stronger currency and that would hurt China as an export-driven economy. Further, General Secretary Xi is unlikely to relinquish capital outflow controls and let Davos Fat Cats flood China’s financial sector any time soon.

Rep. Roger Williams (R-TX) called China a currency manipulator.

Rep. Roger Williams (R-TX) called China a currency manipulator.

“They have been manipulating their currency and one way they do this is to put limits on outbound capital which keeps the renminbi weak,” he said in the Q&A period with Billingslea. “How can we hold them accountable?”

Billingslea fired back instantly. “Treasury should call them what they are…a currency manipulator,” he said. “We run a trade deficit with the Chinese and that means they export more to us than we import. All of that delta goes into China’s war chest, into their forex reserves. Under the Biden administration, the deficit with China is rising again so we need to look at how we become more competitive and we must insist on a more balanced trade with China.” [Testimony]

Witnesses warned Committee members to tread lightly on sanctioning dollar transactions, as it is pushing countries that are otherwise U.S. allies to seek out alternatives to the dollar in order to protect from sanctions policies.

Washington has used dollar sanctions with increasing frequency. In the year 2000, only four countries were targeted and now it is 20 countries facing restrictions on access to dollars, either through sanctions against individuals or companies. Adversaries like China, and countries who are reliant on China for trade, are more aware as to why they need to reduce their reliance on the dollar for domestic investment and in cross-border transactions, warned Daniel McDowell, Associate Professor at the Maxwell School of Citizenship & Public Affairs at Syracuse University.

“We need to reconsider financial sanctions, and not politicize the dollar,” McDowell said. [Testimony]

Senior Fellow at The Atlantic Council, Carla Norrlof, said that dollar dominance is in decline.

“I can tell you that the dollar is not as strong in private transactions. It averages 45% of private transactions and issuance for international debt and securities, and cross border banking,” she said. [Testimony]. “Chinese renminbi is only 3% of overall central bank reserves, but they have been successful in getting it used in trade with them, so it is potentially a long-term challenger. If the renminbi is increasingly used by their trade partners. it will be a threat to the dollar,” she said, adding that the U.S. needs economic inducements instead of sanctions because sanctions are alienating allies in the developing world.

The hearing also highlighted two bits of legislation, though neither would impact dollar valuation. One was about China’s advancement into a programmable central bank digital currency and the other was a messaging bill, called the “21st Century Dollar Act”, which would require Treasury to report on China’s actions on the dollar – such as trading dollars in its central bank account, and signing commercial agreements priced in another currency.

* * *

A Dominant Dollar Need Not Be an Overvalued Dollar

Chairman Luetkemeyer said the strong dollar enables cheaper imports. The U.S. trade deficit continues to rise, hitting over $1 trillion for the last two years in a row.

The dollar is dominant because of well-regulated financial markets and other financial assets sold to the world. The dollar is and will remain dominant because of its deep investment market – stocks, bonds, real estate, venture capital, and more. And the U.S. has a dynamic economy. The U.S. economy is stronger than Europe’s, and it’s securities markets and corporate legal framework are more trusted than the No. 2 economy – China.

This dominance tends to push the dollar exchange rate higher. It will always be strong in comparison to world currencies. This is the main problem, and it hurts U.S. businesses competing with currencies worth pennies (see the Vietnamese dong for example).

The dollar value can be managed to a competitive and stable price, even as it continues to be widely used globally. Dollar assets are liquid, safe, and stable. Managing the exchange rate would increase stability and provide a place that American and global investors can safely store wealth.

CPA’s Currency Misalignment Monitor for June shows the dollar is 14.3% overvalued in relation to a level that would balance trade. The undervaluations of Japan and China have also increased, to 42% and 22%, respectively. These undervaluations make imports more attractive, as witnesses and Chairman Leutkemeyer noted.

The Taiwan dollar is 48% undervalued and is a source of semiconductor imports at a time when the U.S. government is spending billions on reshoring the chips industry. CPA estimates are based on real (inflation-adjusted) exchange rate data for the month of March from the Bank of International Settlements.

Worth noting, U.S. Treasury data shows that foreign purchases of U.S. securities and bank deposits in 2022 were $1.6 trillion, the size of the entire Brazilian economy, and is up 45% from 2021. Financial inflows are the most significant driver of foreign exchange rates. These portfolio investment flows can put U.S. manufacturers at a disadvantage as it leads to an overvalued dollar, making imports more enticing than domestic production.

In the Committee Memorandum about Wednesday’s hearing, the committee staff wrote that “a strong dollar helps American consumers by lowering the price of imported goods, which results in a $25 to $45 billion per year in savings.”

What the staffers failed to note is the dramatic amount of jobs, investment, and production sacrificed due to dollar overvaluation — for these relatively paltry savings in a $23 trillion economy.

“A competitive dollar would increase the attractiveness of the dollar as an international investment and a reserve currency because it would be more stable than the dollar in today’s volatile global economy,” said Ferry. “Interest rate expectations and large capital flows are a destabilizing force,” he said.