Does Wall Street, Congress, and to some extent, the American business community fully grasp the political and economic risks of engagement with China? For some, talk of decoupling is more talk than reality. What’s real: more coupling. The world’s No. 1 and No.2 economies are enmeshed. What to do? Only a relative few in Congress believe the pre-Trump era China relationship should stand. Big businesses and Wall Street seem to think otherwise.

Last week, the U.S. China Economic and Security Review Commission held a day-long, four-panel meeting titled, “U.S. China Relations in 2021: Emerging Risks.”

It was a long discussion about recent capital markets sanctions against dozens of Chinese companies that Wall Street firms like Vanguard can no longer invest in, and whether or not businesses want to leave China and reshore.

For the most part, the U.S. is far behind Australia and Japan on reshoring efforts, noted Dan Harris, a partner at the Harris Bricken law firm and the main writer behind the ChinaLaw blog.

Those two countries are actively paying their companies to bring supply chains back home. The U.S. is not. Larry Kudlow said this would happen in May 2020, but it was shelved due to the pandemic.

More American companies are either sourcing from southeast Asia, which is one reason why our trade deficit with Vietnam is bigger than our trade deficit with Germany, or they are moving to Mexico.

Here is a quick look at what questions were raised in a highly animated, emotional panel session titled: “The CCP’s Control of Markets and Data.”

~Michael Wessel, Commissioner. U.S. China Economic and Security Review Commission.

On Delisting China from American Capital Markets

China is like one big Enron, noted Commissioner Bob Borochoff: funky investment vehicles like the Variable Interest Entities (VIE’s) offer investment that looks like an investment in a company in the Caymans (or elsewhere) but is really an investment in a shell company that invests in the real company in China. There’s that issue, and then there’s the issue of the PCAOB. For years it tried to convince China that it had to be compliant with the Sarbanes-Oxley Act (SOX) but largely abandoned those pursuits after an MOU was signed giving China special rights and avoiding compliance. If compliant, they would have to open their company’s books to third-party audits by a company like PWC. China refuses, stating state secrets. This is why lawmakers passed the Holding Foreign Companies Accountable Act, signed into law in 2020, to require Chinese companies to comply with the same oversight and accounting standards as U.S. and allied companies.

The financial battlefront in the China trade war is about delisting companies that are tied to the Chinese military; delisting those that don’t follow SOX compliance on audits; and – in the future – delisting bad actors put on the Commerce Department’s Entity List or DOD’s Chinese Military Companies list – or even a yet-to-be-created State Department list for issues such as espionage concerns, military activity, or even labor and human rights abuses. Wheels are in motion.

Commissioner Alex N. Wong: I understand why these investors wouldn’t want to see this, but if you are a U.S. regulator, diminishing a few China companies whose listings make up maybe 4% of U.S. listings, there will be time for U.S. investors to get out. It’s a healthy decision.

Shaswat Das, counsel, King & Spalding: The CCP knows that U.S. investors are interested in Chinese stocks. Actually, the percentage is 6% to 8% not 4%, so you’d see about $2 trillion go out the door. If it was easy, the decision would have been made a while ago.

Wong: But you posit that a full delisting would have a huge impact. If you went after one or two SOX rules breakers that gives companies a chance to rethink their compliance and yes, they can go to other exchanges, but the reason they want to come here is because of the liquidity. We have leverage here and we should be able to take additional enforcement actions.

Das: I think we can. But there has been collective reticence to do that. When I was at the PBAOC for five years, I had no leverage. Occasionally, I’d get a letter from Congress on the subject, but rarely. So when I was talking to Beijing about this it carried no weight. We are living in a different environment today.

Commissioner Michael Wessel: There should be no flow of U.S. capital to China Entity List companies. We are busy subsidizing the CCP with billions of dollars in private capital…and taxpayer money.

~ Commissioners Derek Scissors (top) and Roy Kamphausen (bottom).

* * *

Wall Street Rabbit vs China Hare

The short-term view of Wall Street and mostly every publicly traded multinational corporation is at odds with the long-term view of China. Both sides have different goals. Does Wall Street understand that? Because until they do, China’s slow and steady will win the race.

~Dan Harris, panelist and partner in the Harris Bricken lawfirm.

Former Sen. Jim Talent (R-MO): What we have here between the United States and China is a conflict between a rising hegemon and an established hegemon who define their vital national interests in mutually exclusive and contradictory ways. For the Wall Street and the investment community to be going on thinking ‘let’s find this great return in this IPO for our clients’…I don’t think they’re dealing in the real world. Do the big firms who run Wall Street and the hedge funds…do they really get this?

Harris: It took an investment banker to explain to me how it is that these very smart people don’t get it and his explanation was that ‘we are trained to look at companies and industries, very few of us look at the big picture.’ Like governments. Like conflicts. Like what is actually going on policy-wise in China essentially moving farther along the path to various stages of communism.

Das: Many retail investors gain their exposure through the big mutual funds, through 401ks and various other investment vehicles and they are relying on investment advisors and managers who are functioning as fiduciaries. I think retail investors get it, but they see it as high risk, high reward, and for them, so far, it’s been high reward.

Talent: I agree. But they saw that when there was a good U.S.-China relationship on both sides, when the U.S. was about engagement. That ended about five years ago. I don’t think the investment community has caught up with it.

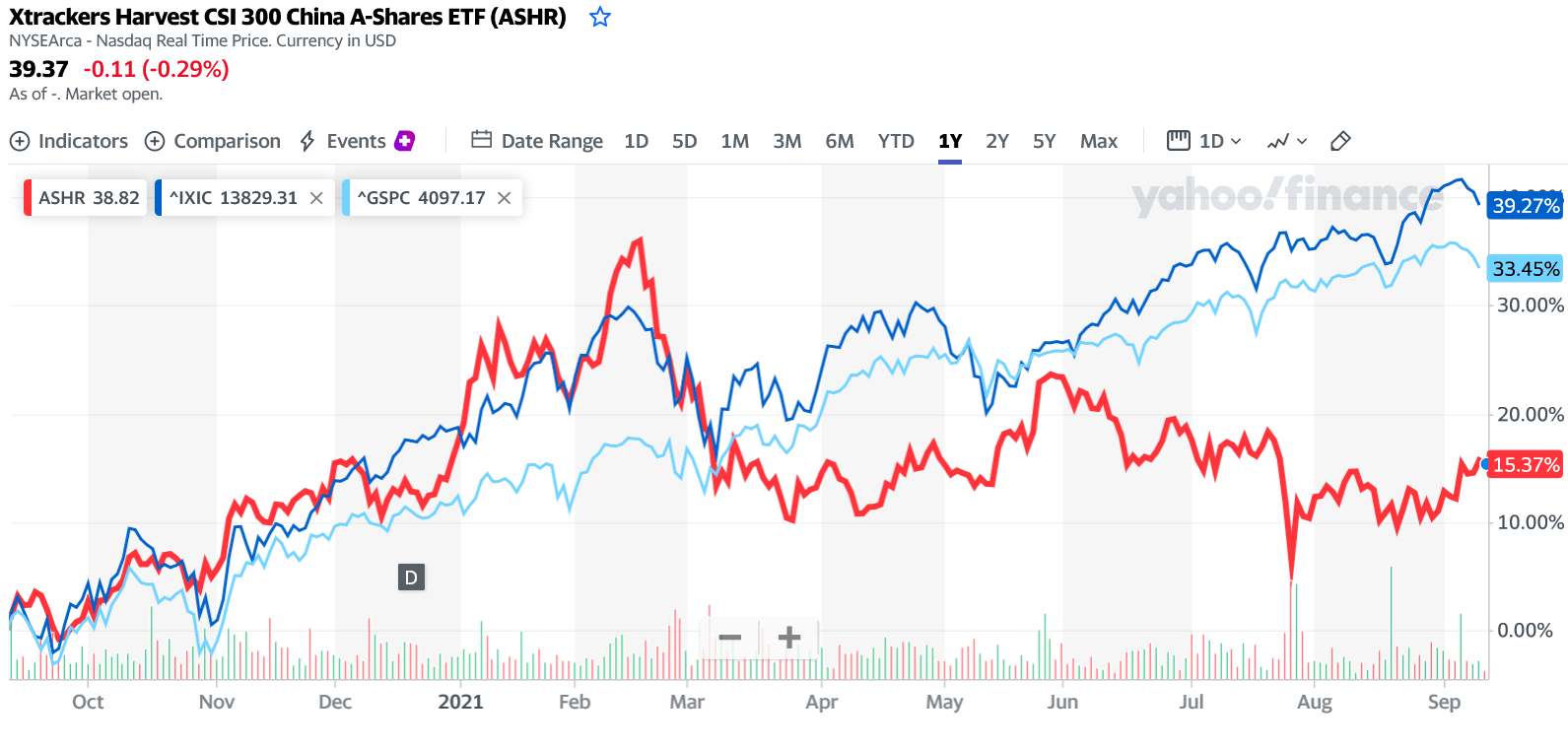

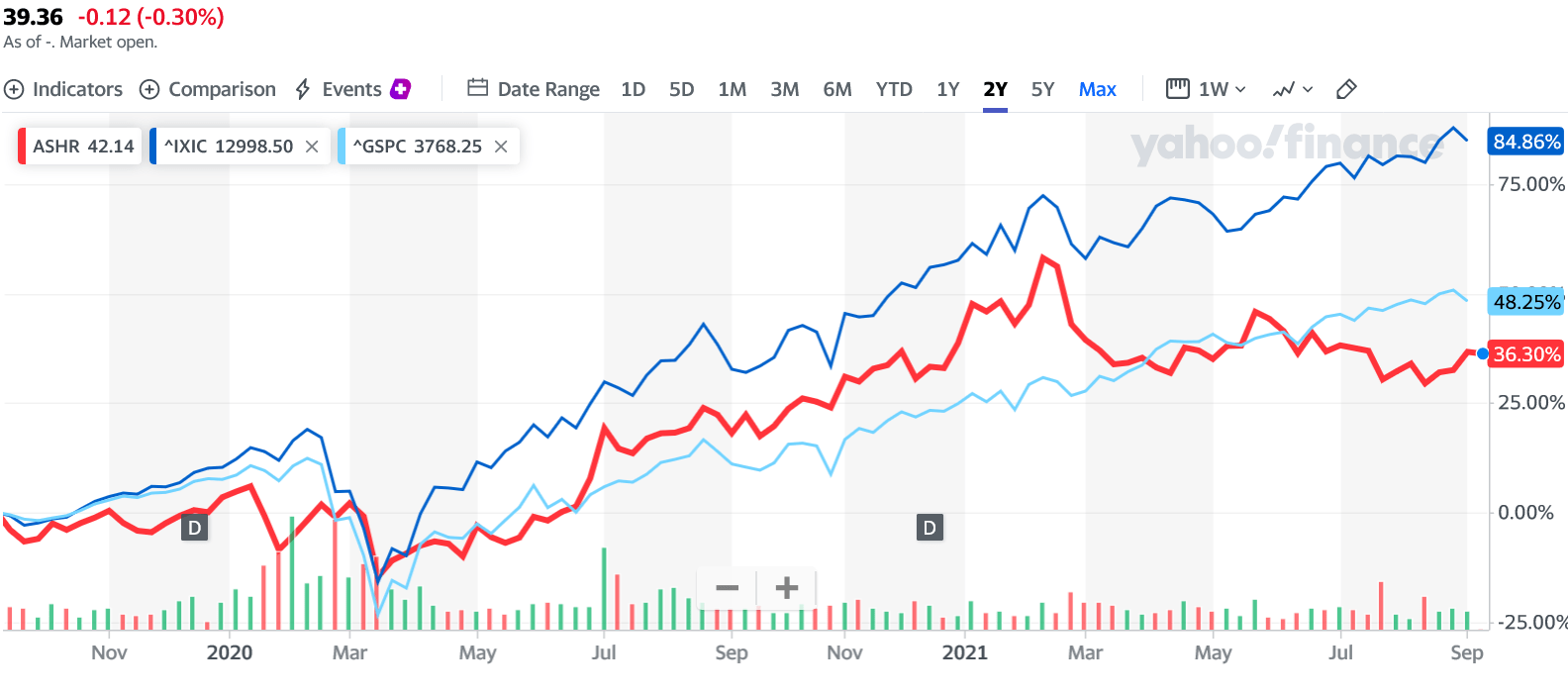

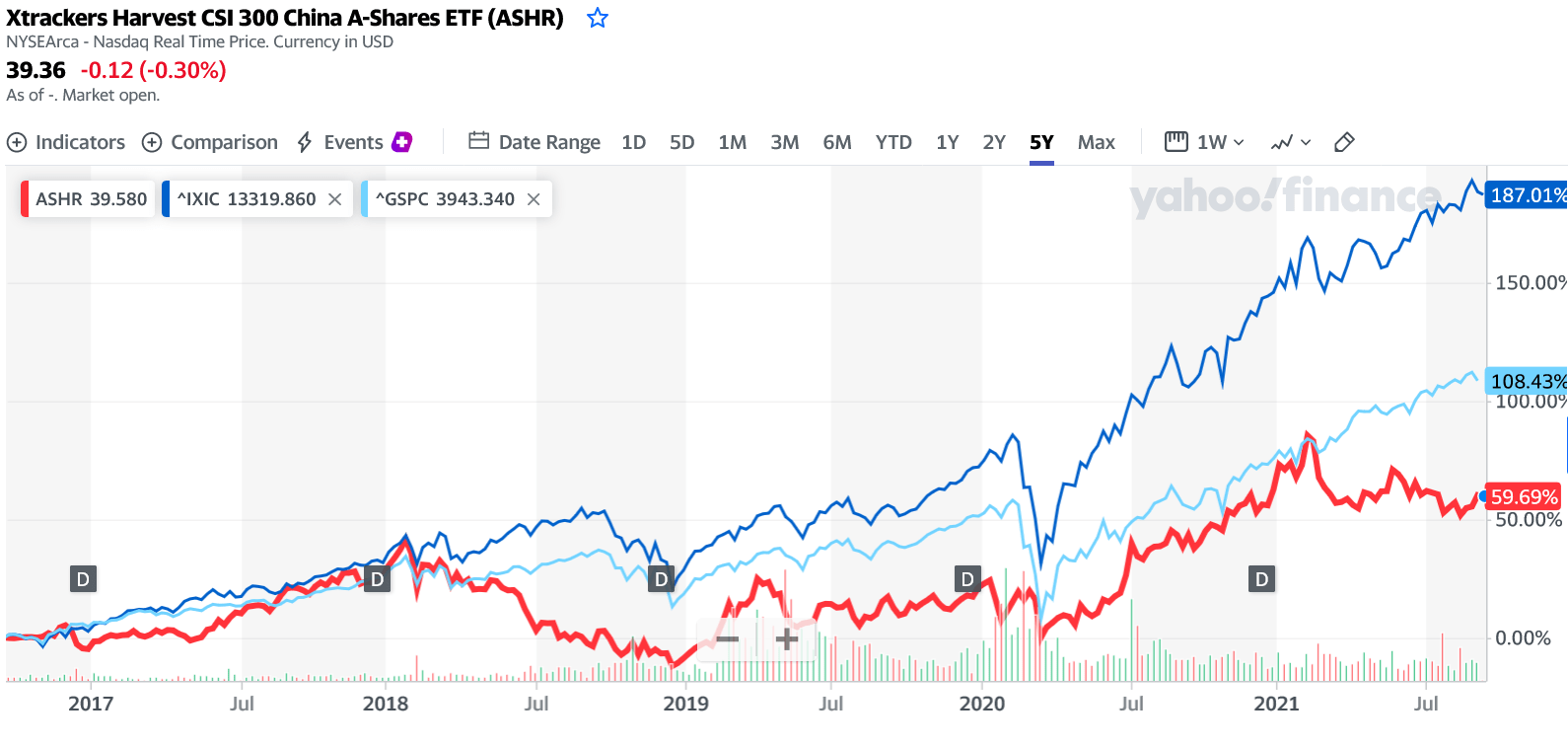

And regarding China being a high-risk, high reward investment. This is the China A-shares over a period of 1 to 5 years. An investment in the S&P 500 or Nasdaq beat them every time.

Limbo: Neither Together, Nor Apart

Commissioner Kimberly Glas wanted to know if companies are moving out of China. Have they started changing their minds on sourcing from there, almost exclusively? Or is it that China’s unmatched infrastructure, built out of decades of understanding that it would be the Western world’s factory, too good to pass up? China makes it easy for companies to stay. But that’s changing as political risks between Washington and Beijing make it harder. Unless you are of the mind that things get better with China, political risks will only increase. This was the general sentiment at last week’s panel discussion.

Glas: Is congress giving this enough attention? This is all making me think there has not been enough attention to companies leaving China. Are they even leaving?

Harris: When President Trump initiated the tariffs we started talking to our clients saying this is the beginning of what we see as decoupling and literally only one client believed us. It was not until Biden became president and did not roll back the tariffs that businesses started realizing en masse that the tariffs looked like they were here to stay. Most SMEs are too busy scrambling to deal with long-term risk. But with all that has gone on lately, they are steadily starting to deal with that risk. The ongoing tariffs; the increasing shipping costs; the inability to go to China more orderly because of Covid; China cracking down on businesses left and right. Our clients are starting to see it. They’re trying to figure out what to do. There was a period of about two weeks when I asked 15 of my clients who manufactured in China whether they wanted to get out. And they all said yes.

~ Shaswat Das, counsel, King & Spalding. He worked with the Public Accounting Oversight Board in the Obama years.

* * *

In the end, Commissioner Borochoff, who is in favor of more capital markets sanctions and delisting, especially of China VIEs, was the one who made the Enron comparison.

He recalled meeting Enron executives Ken Lay and Jeff Skilling between 1997 and 2001. They were a client of his firm the Borochoff Group. In 1999, they stopped paying and were always in deferment. At the time, he noted, people thought Enron “was a super strong company.” Ken Lay ‘retired’ because rumor had it that he would be appointed to the cabinet of George W. Bush. He did not. Then a year later, Enron went broke.

Borochoff compared that to the China of today. Many people think investing in China, both as a portfolio investment and as a business partner, is great. Until it isn’t.

“Thousands of people lost their money, jobs, and retirement and the net effect to the economy was gigantic,” he said. “When something ripples, even if it is small, it really hurts the economy. I remember asking Ken Lay about those Special Purpose Vehicle investments of Enron and he couldn’t explain to me what they did. It was just too complicated, he said. I join with my colleagues who think that sanctions and greater enforcement are needed for China’s VIEs. I see them as no different than those Special Purpose entities that Sarbanes Oxley worked so hard to straighten out.”

Harris fired a final warning on the day.

“What I see as an even bigger risk is China insinuating itself into the United States and doing it via businesses, getting our IP, doing it with spies, doing it by sending people over here to work for American companies who are also working for Chinese companies in China. There is a lot of naivete on that. Our clients will say, ‘look, I’ve been friends with this guy for 10 years, he would never do anything to hurt me’, and my response is always: ‘nothing against your friend, but do you really think that when the CCP knocks on his door and says you need to give us this info, this data, or this IP or your parents pension is going to be cut off; do you really think he is going to be able to withstand that?’ That is an issue that really troubles me,” Harris said.

He later singled out American universities as an open-door invitation to CCP influence, let alone intellectual property theft and espionage.

“My father was a university professor. I very much believed in academic freedom. But I know for a fact that there are Chinese spies in U.S. universities and colleges,” Harris said. “The universities will tell you ‘there is nothing we can do.’ That to me is the systemic risk. We talk about decoupling, but right now there is a coupling. And this is a coupling that does not compare to what we had during the Cold war with the Soviet Union. I don’t know how we handle that.”

CPA wrote about this panel last week, focusing primarily on the testimony of Dan Harris, Shaswat Das, and Rebecca Fair. You can see their full testimonies and bios below:

The CCP’s Control of Markets and Data

Dan Harris, Partner, Harris Bricken [Testimony]

Rebecca Fair, CEO and Cofounder, Thresher [Testimony]

Shaswat Das, Counsel, King & Spalding [Testimony]

China Commission Wonders: Do Congress, Investors, Really Know What’s at Stake in China?

Does Wall Street, Congress, and to some extent, the American business community fully grasp the political and economic risks of engagement with China? For some, talk of decoupling is more talk than reality. What’s real: more coupling. The world’s No. 1 and No.2 economies are enmeshed. What to do? Only a relative few in Congress believe the pre-Trump era China relationship should stand. Big businesses and Wall Street seem to think otherwise.

Last week, the U.S. China Economic and Security Review Commission held a day-long, four-panel meeting titled, “U.S. China Relations in 2021: Emerging Risks.”

It was a long discussion about recent capital markets sanctions against dozens of Chinese companies that Wall Street firms like Vanguard can no longer invest in, and whether or not businesses want to leave China and reshore.

For the most part, the U.S. is far behind Australia and Japan on reshoring efforts, noted Dan Harris, a partner at the Harris Bricken law firm and the main writer behind the ChinaLaw blog.

Those two countries are actively paying their companies to bring supply chains back home. The U.S. is not. Larry Kudlow said this would happen in May 2020, but it was shelved due to the pandemic.

More American companies are either sourcing from southeast Asia, which is one reason why our trade deficit with Vietnam is bigger than our trade deficit with Germany, or they are moving to Mexico.

Here is a quick look at what questions were raised in a highly animated, emotional panel session titled: “The CCP’s Control of Markets and Data.”

~Michael Wessel, Commissioner. U.S. China Economic and Security Review Commission.

On Delisting China from American Capital Markets

China is like one big Enron, noted Commissioner Bob Borochoff: funky investment vehicles like the Variable Interest Entities (VIE’s) offer investment that looks like an investment in a company in the Caymans (or elsewhere) but is really an investment in a shell company that invests in the real company in China. There’s that issue, and then there’s the issue of the PCAOB. For years it tried to convince China that it had to be compliant with the Sarbanes-Oxley Act (SOX) but largely abandoned those pursuits after an MOU was signed giving China special rights and avoiding compliance. If compliant, they would have to open their company’s books to third-party audits by a company like PWC. China refuses, stating state secrets. This is why lawmakers passed the Holding Foreign Companies Accountable Act, signed into law in 2020, to require Chinese companies to comply with the same oversight and accounting standards as U.S. and allied companies.

The financial battlefront in the China trade war is about delisting companies that are tied to the Chinese military; delisting those that don’t follow SOX compliance on audits; and – in the future – delisting bad actors put on the Commerce Department’s Entity List or DOD’s Chinese Military Companies list – or even a yet-to-be-created State Department list for issues such as espionage concerns, military activity, or even labor and human rights abuses. Wheels are in motion.

Commissioner Alex N. Wong: I understand why these investors wouldn’t want to see this, but if you are a U.S. regulator, diminishing a few China companies whose listings make up maybe 4% of U.S. listings, there will be time for U.S. investors to get out. It’s a healthy decision.

Shaswat Das, counsel, King & Spalding: The CCP knows that U.S. investors are interested in Chinese stocks. Actually, the percentage is 6% to 8% not 4%, so you’d see about $2 trillion go out the door. If it was easy, the decision would have been made a while ago.

Wong: But you posit that a full delisting would have a huge impact. If you went after one or two SOX rules breakers that gives companies a chance to rethink their compliance and yes, they can go to other exchanges, but the reason they want to come here is because of the liquidity. We have leverage here and we should be able to take additional enforcement actions.

Das: I think we can. But there has been collective reticence to do that. When I was at the PBAOC for five years, I had no leverage. Occasionally, I’d get a letter from Congress on the subject, but rarely. So when I was talking to Beijing about this it carried no weight. We are living in a different environment today.

Commissioner Michael Wessel: There should be no flow of U.S. capital to China Entity List companies. We are busy subsidizing the CCP with billions of dollars in private capital…and taxpayer money.

~ Commissioners Derek Scissors (top) and Roy Kamphausen (bottom).

* * *

Wall Street Rabbit vs China Hare

The short-term view of Wall Street and mostly every publicly traded multinational corporation is at odds with the long-term view of China. Both sides have different goals. Does Wall Street understand that? Because until they do, China’s slow and steady will win the race.

~Dan Harris, panelist and partner in the Harris Bricken lawfirm.

Former Sen. Jim Talent (R-MO): What we have here between the United States and China is a conflict between a rising hegemon and an established hegemon who define their vital national interests in mutually exclusive and contradictory ways. For the Wall Street and the investment community to be going on thinking ‘let’s find this great return in this IPO for our clients’…I don’t think they’re dealing in the real world. Do the big firms who run Wall Street and the hedge funds…do they really get this?

Harris: It took an investment banker to explain to me how it is that these very smart people don’t get it and his explanation was that ‘we are trained to look at companies and industries, very few of us look at the big picture.’ Like governments. Like conflicts. Like what is actually going on policy-wise in China essentially moving farther along the path to various stages of communism.

Das: Many retail investors gain their exposure through the big mutual funds, through 401ks and various other investment vehicles and they are relying on investment advisors and managers who are functioning as fiduciaries. I think retail investors get it, but they see it as high risk, high reward, and for them, so far, it’s been high reward.

Talent: I agree. But they saw that when there was a good U.S.-China relationship on both sides, when the U.S. was about engagement. That ended about five years ago. I don’t think the investment community has caught up with it.

And regarding China being a high-risk, high reward investment. This is the China A-shares over a period of 1 to 5 years. An investment in the S&P 500 or Nasdaq beat them every time.

Limbo: Neither Together, Nor Apart

Commissioner Kimberly Glas wanted to know if companies are moving out of China. Have they started changing their minds on sourcing from there, almost exclusively? Or is it that China’s unmatched infrastructure, built out of decades of understanding that it would be the Western world’s factory, too good to pass up? China makes it easy for companies to stay. But that’s changing as political risks between Washington and Beijing make it harder. Unless you are of the mind that things get better with China, political risks will only increase. This was the general sentiment at last week’s panel discussion.

Glas: Is congress giving this enough attention? This is all making me think there has not been enough attention to companies leaving China. Are they even leaving?

Harris: When President Trump initiated the tariffs we started talking to our clients saying this is the beginning of what we see as decoupling and literally only one client believed us. It was not until Biden became president and did not roll back the tariffs that businesses started realizing en masse that the tariffs looked like they were here to stay. Most SMEs are too busy scrambling to deal with long-term risk. But with all that has gone on lately, they are steadily starting to deal with that risk. The ongoing tariffs; the increasing shipping costs; the inability to go to China more orderly because of Covid; China cracking down on businesses left and right. Our clients are starting to see it. They’re trying to figure out what to do. There was a period of about two weeks when I asked 15 of my clients who manufactured in China whether they wanted to get out. And they all said yes.

~ Shaswat Das, counsel, King & Spalding. He worked with the Public Accounting Oversight Board in the Obama years.

* * *

In the end, Commissioner Borochoff, who is in favor of more capital markets sanctions and delisting, especially of China VIEs, was the one who made the Enron comparison.

He recalled meeting Enron executives Ken Lay and Jeff Skilling between 1997 and 2001. They were a client of his firm the Borochoff Group. In 1999, they stopped paying and were always in deferment. At the time, he noted, people thought Enron “was a super strong company.” Ken Lay ‘retired’ because rumor had it that he would be appointed to the cabinet of George W. Bush. He did not. Then a year later, Enron went broke.

Borochoff compared that to the China of today. Many people think investing in China, both as a portfolio investment and as a business partner, is great. Until it isn’t.

“Thousands of people lost their money, jobs, and retirement and the net effect to the economy was gigantic,” he said. “When something ripples, even if it is small, it really hurts the economy. I remember asking Ken Lay about those Special Purpose Vehicle investments of Enron and he couldn’t explain to me what they did. It was just too complicated, he said. I join with my colleagues who think that sanctions and greater enforcement are needed for China’s VIEs. I see them as no different than those Special Purpose entities that Sarbanes Oxley worked so hard to straighten out.”

Harris fired a final warning on the day.

“What I see as an even bigger risk is China insinuating itself into the United States and doing it via businesses, getting our IP, doing it with spies, doing it by sending people over here to work for American companies who are also working for Chinese companies in China. There is a lot of naivete on that. Our clients will say, ‘look, I’ve been friends with this guy for 10 years, he would never do anything to hurt me’, and my response is always: ‘nothing against your friend, but do you really think that when the CCP knocks on his door and says you need to give us this info, this data, or this IP or your parents pension is going to be cut off; do you really think he is going to be able to withstand that?’ That is an issue that really troubles me,” Harris said.

He later singled out American universities as an open-door invitation to CCP influence, let alone intellectual property theft and espionage.

“My father was a university professor. I very much believed in academic freedom. But I know for a fact that there are Chinese spies in U.S. universities and colleges,” Harris said. “The universities will tell you ‘there is nothing we can do.’ That to me is the systemic risk. We talk about decoupling, but right now there is a coupling. And this is a coupling that does not compare to what we had during the Cold war with the Soviet Union. I don’t know how we handle that.”

CPA wrote about this panel last week, focusing primarily on the testimony of Dan Harris, Shaswat Das, and Rebecca Fair. You can see their full testimonies and bios below:

The CCP’s Control of Markets and Data

Dan Harris, Partner, Harris Bricken [Testimony]

Rebecca Fair, CEO and Cofounder, Thresher [Testimony]

Shaswat Das, Counsel, King & Spalding [Testimony]

MADE IN AMERICA.

CPA is the leading national, bipartisan organization exclusively representing domestic producers and workers across many industries and sectors of the U.S. economy.

TRENDING

Foreign Supply Shocks – Not U.S. Tariffs – Are Driving the Fertilizer Crisis Threatening American Grocery Bills

Food Security Is Fertilizer Security

The Jones Act: An America First Law, Waived for China’s Benefit

Ranking America’s Duties on Tonnage

House Foreign Affairs Committee Ropes In Japan, South Korea as Solution to U.S. Shipbuilding Woes

The latest CPA news and updates, delivered every Friday.

WATCH: WORTH FIGHTING FOR

Get the latest in CPA news, industry analysis, opinion, and updates from Team CPA.

CHECK OUT THE NEWSROOM ➔