KEY POINTS

- U.S. imports of data center equipment reached $653 billion in 2025, more than double their 2020 level. That total breaks into two distinct supply chains: nearly $580 billion in computing hardware (servers, chips, networking, cooling) and more than $70 billion in power infrastructure (transformers, switchgear, lithium-ion batteries). Tariffs and export controls have reshaped the first. The second remains dangerously exposed.

- Shortages of transformers, switchgear, and batteries are already threatening to delay the buildout. Lead times for large power transformers have stretched to as long as five years, and roughly 40% of planned U.S. data center capacity faces delays tied to equipment and power availability. The equipment the United States cannot manufacture fast enough is the same equipment it increasingly sources from China.

- The power supply chain tells the opposite story. China’s share of U.S. lithium-ion battery imports peaked at 71% in 2023 and remains at 59%. China controls 99% of global lithium iron phosphate (LFP) cathode production, the battery chemistry of choice for data centers and grid-scale storage. Transformer imports show signs of rerouting through Southeast Asia to circumvent tariffs.

- Tariffs proved they can redirect trade flows. They have not yet proved they can rebuild domestic production. The computing stack needs to be reshored, not just rerouted. The power stack needs both: strengthening 45X production incentives, enforcing FEOC restrictions at the processing stage, investing in allied cathode processing networks, and investigating transformer rerouting through Southeast Asia.

The Import Surge

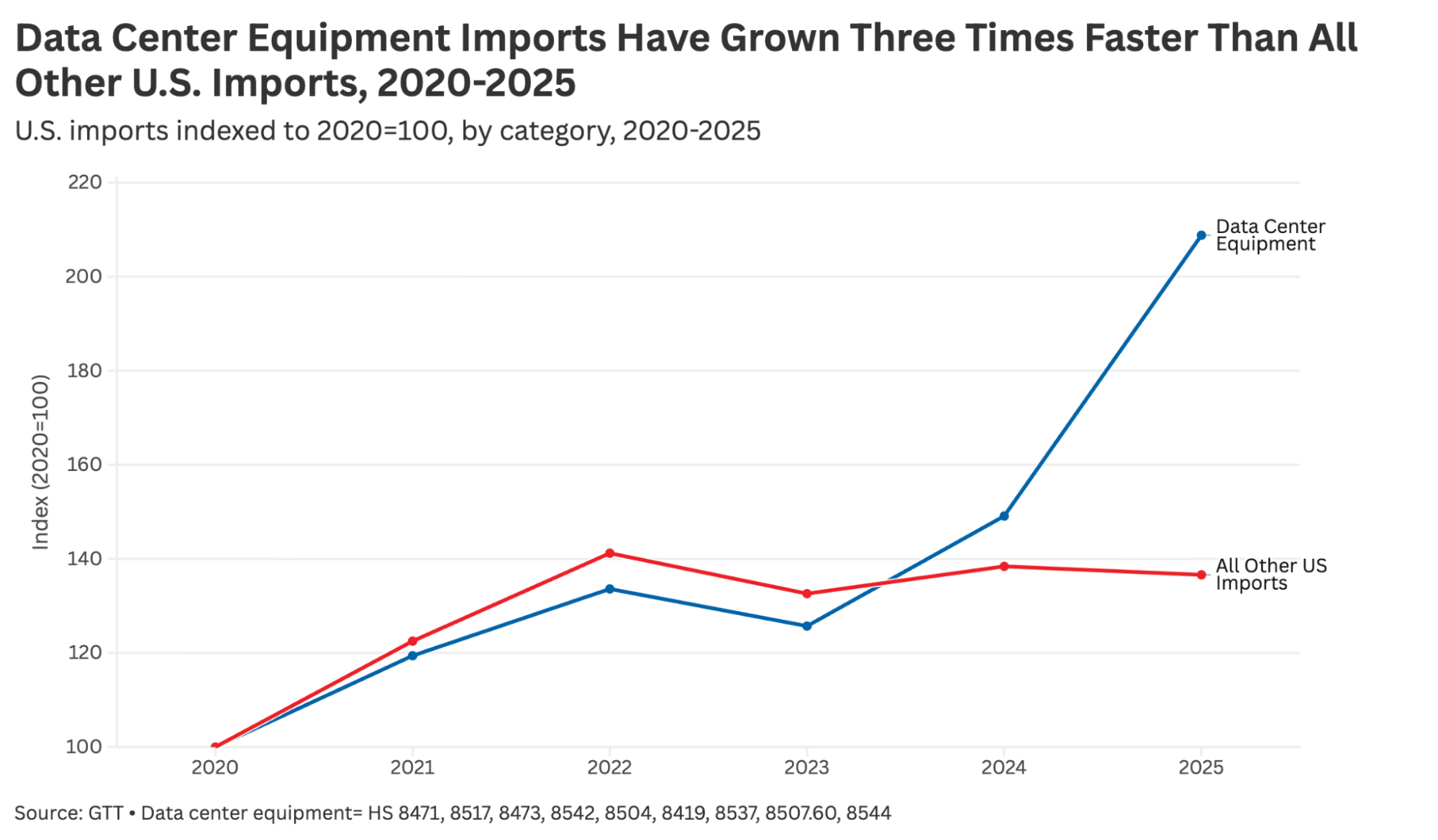

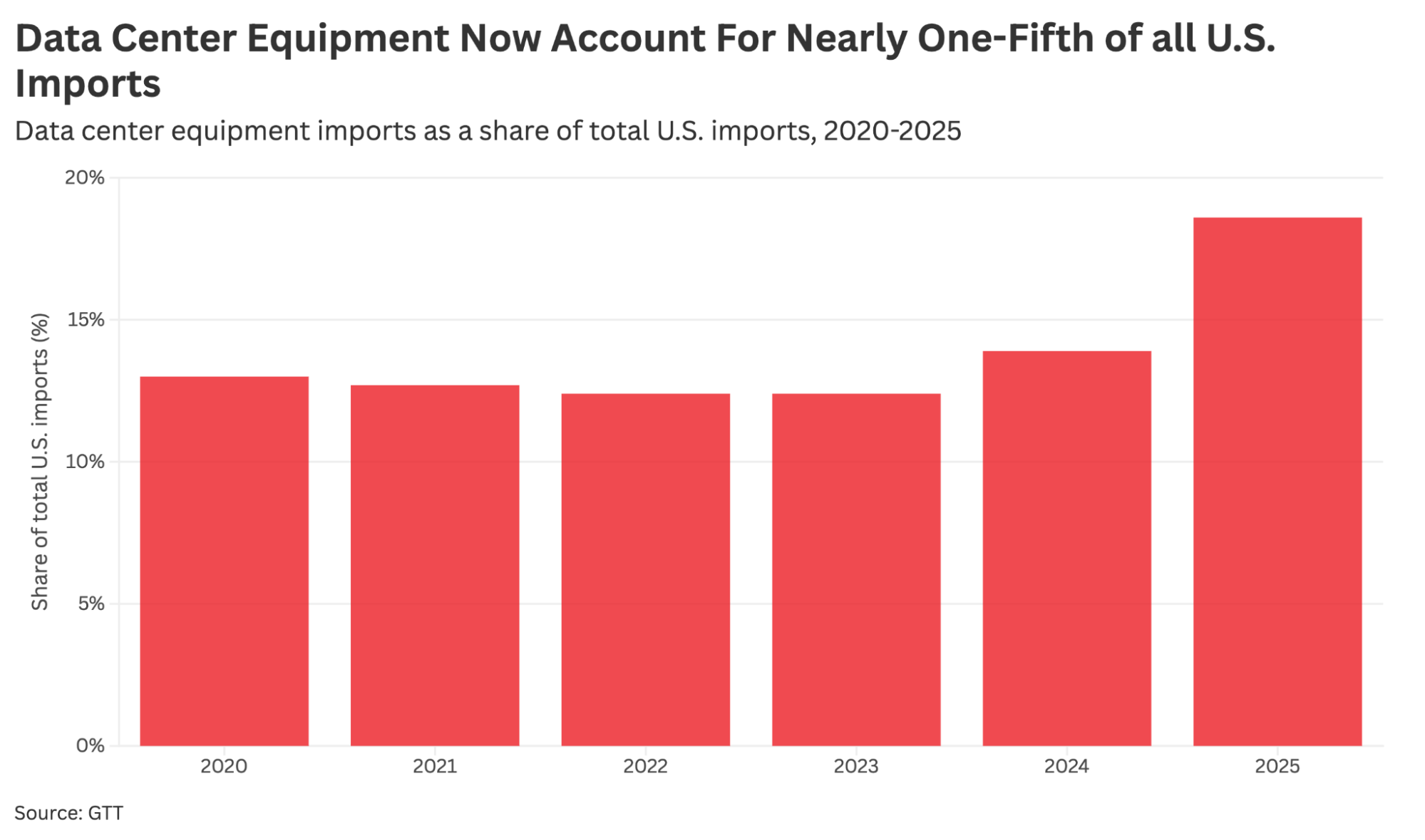

The AI data center buildout is reshaping the U.S. trade balance. Between 2020 and 2025, U.S. imports of nine categories of data center equipment grew from $312.7 billion to $653.1 billion, an increase of 109% (Figure 1). Over the same period, all other U.S. imports grew by just 37%. Data center hardware now accounts for 18.6% of total U.S. merchandise imports, up from 13% in 2020 (Figure 2).

FIGURE 1:

FIGURE 2:

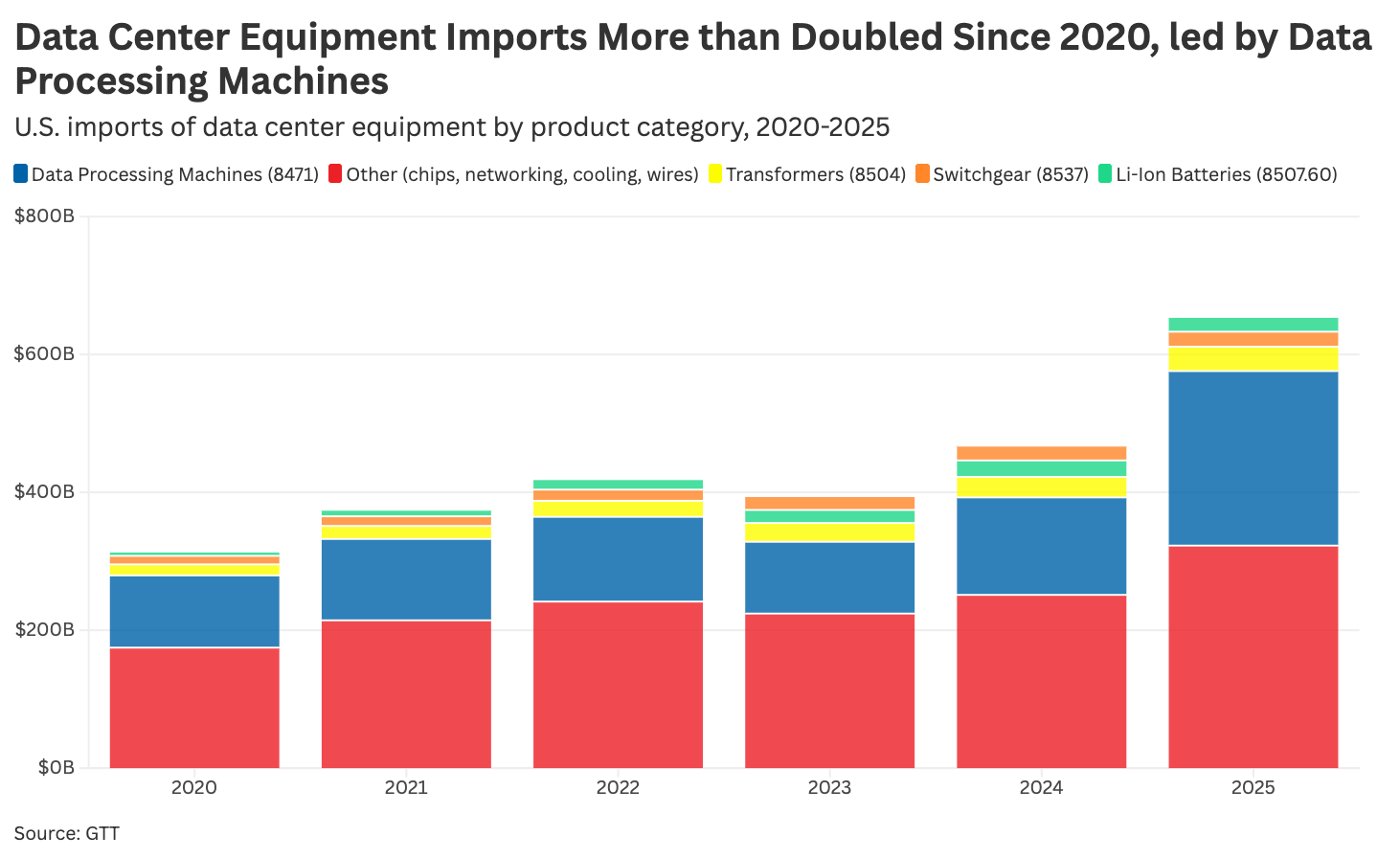

That $653 billion breaks into two supply chains with fundamentally different trajectories. The computing stack accounts for nearly $580 billion: servers and GPU clusters ($253 billion), integrated circuits, networking equipment, cooling systems, and cabling ($328 billion). The power stack accounts for the remaining $70-plus billion: transformers ($30 billion), switchgear ($22 billion), and lithium-ion batteries ($20 billion) (Figure 3).

FIGURE 3:

Every data center requires both halves to function. Tariffs and export controls have redirected the computing stack away from China, though not toward domestic production. The power stack remains heavily import-dependent, and in the case of batteries, China’s dominance has actually deepened.

The scale of this import dependence reflects the capital intensity of the buildout itself. McKinsey estimates global spending on data center construction will reach $7 trillion through 2030. The World Trade Organization reported in late 2025 that imports account for 70-90% of the value of U.S. AI investment, a level of import intensity with few parallels in modern American industrial history. FDI Intelligence data published by the Financial Times show that $320 billion in data center projects were announced globally during 2025, with the United States capturing the largest share of this activity driven by massive AI infrastructure proposals and a surge in equipment imports.

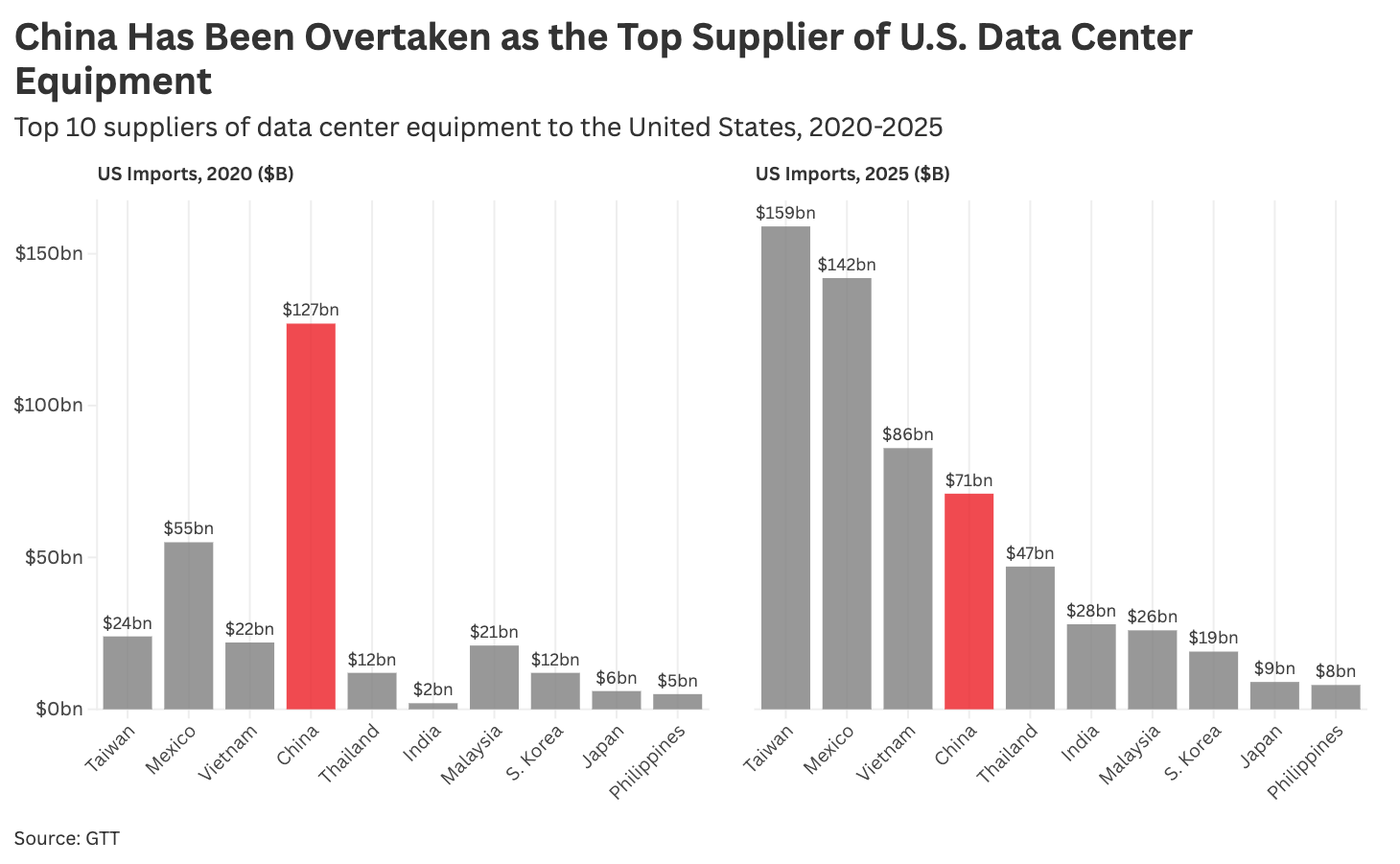

Where these goods originate has changed substantially. In 2020, China was the largest single supplier of data center equipment to the United States, accounting for 41% of imports by value. By 2025, that share had fallen to 11%. Taiwan ($159 billion), Mexico ($142 billion), and Vietnam ($86 billion) have emerged as the dominant suppliers (Figure 4). The shift reflects the cumulative impact of Section 301 tariffs, IEEPA tariffs, and export controls on advanced semiconductors. But the aggregate masks a critical divergence: the computing stack is a partial policy success, where tariffs moved sourcing away from China without building domestic capacity, while the power stack has not even achieved that much.

FIGURE 4:

Computing Stack: Servers and Shifting Suppliers

The computing stack accounts for the vast majority of U.S. data center equipment imports — nearly $580 billion in 2025. It includes the servers and GPU clusters that run AI workloads, the semiconductors inside them, and the networking, cooling, and cabling infrastructure that connects and sustains them. This is where U.S. tariff and export control policy has had its most visible impact. China’s share of U.S. data center computing imports collapsed from over 40% to single digits in five years, replaced by Taiwan, Mexico, and Vietnam. The shift is real, driven by substantial capital investment from Taiwan’s leading contract manufacturers. It is also incomplete: the production moved countries, but it did not move home.

Servers: A Supply Chain in Motion

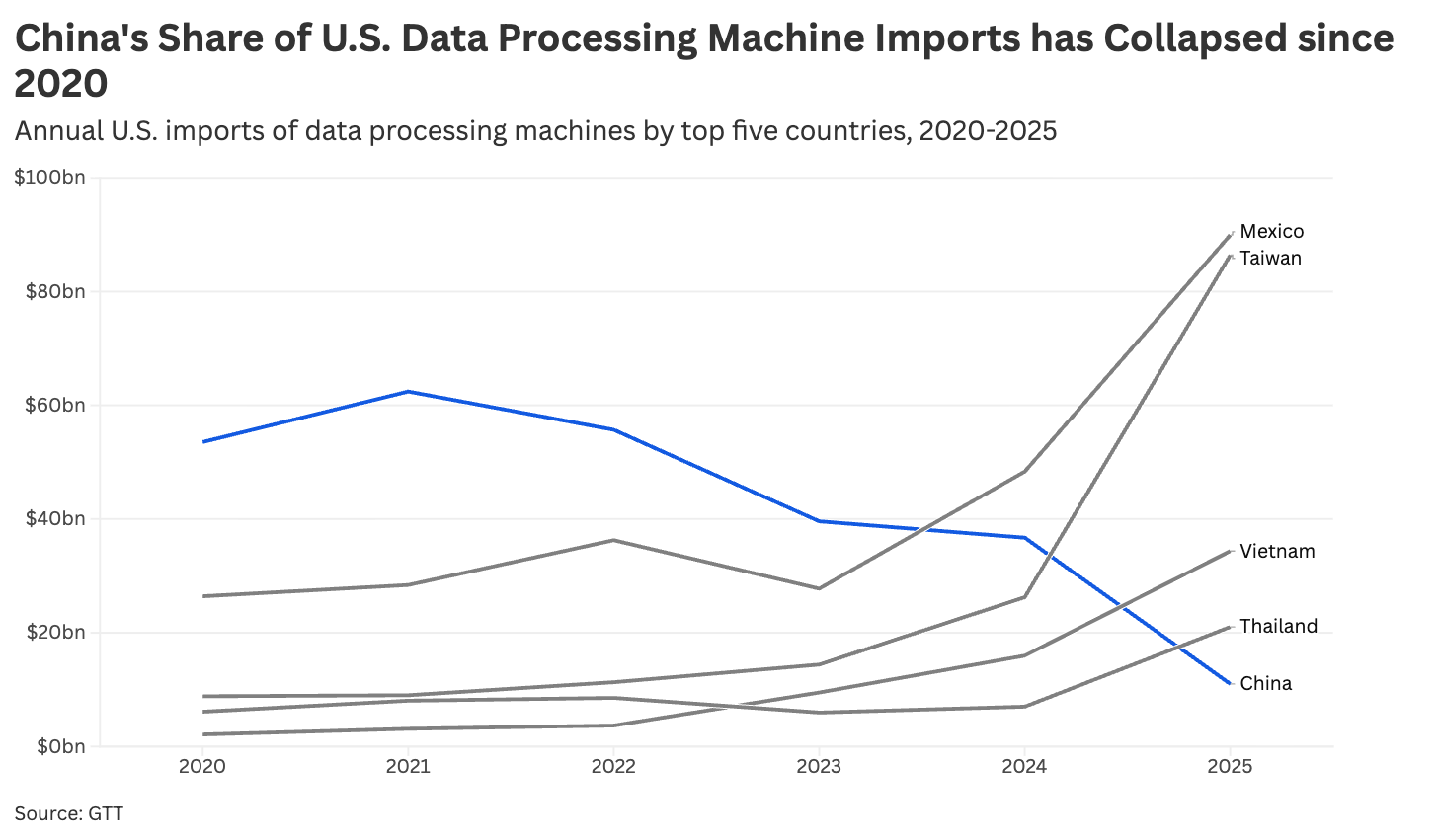

The most dramatic supplier shift has occurred in servers—which are categorized as ADP machines—GPU clusters, and the computing hardware powering AI workloads. In 2020, China supplied 51% of U.S. ADP imports by value, or $53.5 billion. By 2025, that share had collapsed to 4%, just $11 billion (Figure 5).

FIGURE 5:

Three countries absorbed the volume. Mexico’s ADP exports to the United States grew from $26.4 billion to $89.9 billion over the period, raising its share from 25% to 36%. Taiwan’s grew from $8.8 billion to $86.4 billion, a tenfold increase that pushed its share from 8% to 34%. Vietnam’s grew from $2.1 billion to $34.4 billion, moving from a 2% share to 14%. Thailand also expanded significantly, from $6.1 billion to $21 billion.

Several factors drove this reallocation. U.S. tariffs on Chinese-origin servers and computing equipment reached combined rates exceeding 100% at their April 2025 peak under the layered application of Section 301 and IEEPA authorities. At the same time, semiconductor export controls restricted China’s ability to manufacture or assemble the most advanced AI accelerators. NVIDIA, AMD, and their contract manufacturing partners shifted production to Taiwan-based foundries and assembly operations in Mexico, Vietnam, and Thailand. Foxconn and other electronics manufacturers expanded server assembly capacity in Mexico, where proximity to U.S. data center markets and USMCA tariff treatment offered logistical and cost advantages.

The result is a supply chain that has largely decoupled from China for finished computing hardware. That is a necessary first step, but it is not reshoring. The United States still imports more than 95% of its servers. Taiwan alone supplies $86 billion in ADP equipment, and a single disruption in the Taiwan Strait would expose how little the diversification strategy has done to reduce actual import dependence. The power infrastructure feeding those data centers tells a different story still.

Power Stack: Batteries, Transformers, and the Grid Equipment Gap

U.S. imports of the three categories of electrical equipment that power data centers—transformers, switchgear, and lithium-ion batteries—grew from $33.2 billion in 2020 to $77.1 billion in 2025. Unlike the computing stack, where tariffs drove a rapid supplier shift away from China, the power stack tells three different stories.

Lithium-ion batteries remain heavily dependent on China, which supplied 59% of U.S. imports in 2025 and controls 99% of upstream LFP cathode production. Transformer imports have diversified on paper—China’s direct share fell from 27% to 10%—but Chinese exports to Vietnam and Thailand surged in parallel with those countries’ exports to the United States, raising serious transshipment concerns.

Meanwhile, switchgear sourcing is more diversified, though Mexico commands a 40% share backed by real domestic production capacity. Across all three categories, the United States manufactures very little of this equipment domestically, and lead times for critical components like large power transformers already stretch beyond two years.

Grid Stress and the Battery Bottleneck

The power half of the data center supply chain begins with a surge in electricity demand. McKinsey estimates that U.S. data center electricity demand will rise from 147 terawatt-hours in 2023 to 606 terawatt-hours by 2030, consuming nearly 12% of total U.S. power demand.

That surge is colliding with grid infrastructure that was never designed to accommodate it. Data center operators are increasingly turning to on-site battery energy storage systems (BESS) to bridge the gap between what the grid can deliver and what their facilities require. Batteries allow data centers faster interconnection to the grid by agreeing to reduce usage during peak demand periods, and their rapid-response capability matches the highly variable power loads that AI workloads generate.

The buildout is accelerating. Benchmark Mineral Intelligence expects energy storage to account for 41% of total U.S. battery demand in 2026, up from 26% two years earlier. The U.S. Energy Information Administration (EIA) reports that utility-scale battery storage capacity grew 66% in 2024, with 10.4 gigawatts (GW) of new capacity added to the grid. In 2025, developers plan to install a record 19.6 GW, nearly doubling the prior year. In 2022, only a single gigawatt-scale battery facility existed anywhere in the world. By late 2025, 42 were operational, with more than 250 additional gigawatt-scale projects expected to come online by 2027.

Cost declines have accelerated deployment. Lithium-ion battery prices have fallen more than 90% since 2010, and LFP battery prices specifically have halved over the past two years. According to BloombergNEF, the levelized cost of energy from battery storage fell below that of gas turbines for the first time in 2025.

The Chemistry Shift Deepens China Dependence

Lithium-ion batteries are the broad family of rechargeable chemistries powering everything from smartphones to electric vehicles, with LFP and nickel-manganese-cobalt (NMC) as the two dominant variants. Lead-acid batteries, the older technology used in backup power, telecommunications, and defense, occupy a separate category entirely. U.S. trade data on lithium-ion imports capture all lithium-ion chemistries together, but the grid-scale storage pipeline feeding data centers is overwhelmingly LFP.

Much of the data center and grid-scale buildout relies on LFP specifically because these batteries are approximately 35% cheaper to manufacture than NMC alternatives, longer-lasting, and more resistant to overheating, which allows cells to be packed tightly together for stationary storage applications.

LFP chemistry was invented in the United States in the late 1990s but commercialized in China. That distinction now carries enormous supply chain consequences. China controls 99% of global LFP cathode active material production, according to Benchmark Mineral Intelligence. At the cell level, Chinese domestic production accounts for more than 98% of global LFP cell supply.

By 2024, China produced more than six times as many batteries as the United States, according to IEA analysis. Battery manufacturing capacity in the Shanghai area alone exceeded that of the entire European continent. As recently as 2018, U.S. and Chinese battery manufacturing technologies were at a comparable level. Chinese state-backed investment and scale economics have since widened the gap considerably.

China now produces more than three-quarters of all batteries sold globally, and four of the five largest battery storage system manufacturers are Chinese. Tesla is the sole non-Chinese company in that top tier.

There are no large-scale, non-Chinese LFP cathode producers operating today.

As U.S. battery manufacturers convert their EV factories to produce grid-scale LFP storage, they are deepening their dependence on exactly the supply chain that poses the greatest strategic risk. Ford Motor Company is investing $2 billion to repurpose its Kentucky EV battery plant to produce LFP prismatic cells, using technology licensed from Chinese battery giant CATL, the world’s largest battery manufacturer.

General Motors is importing CATL’s LFP batteries for its next-generation Chevrolet Bolt despite total tariffs of approximately 80%, because GM and its partner LG Energy Solution will not have domestic LFP production capacity until 2027. LG Energy Solution is producing cells for Tesla’s energy storage business from a Michigan factory originally built for GM’s EV batteries, at a cost of $4.3 billion. Samsung SDI announced a $1 billion deal to supply batteries to an American energy company from its Indiana factory.

Beijing has already demonstrated its willingness to weaponize these chokepoints. In 2024-2025, China imposed export licensing requirements and an outright ban on antimony shipments to the United States. Antimony is a non-substitutable alloying input for lead-acid batteries, which provide approximately 88% of backup power for telecommunications systems and meet roughly 90% of U.S. uninterruptible power supply (UPS) demand, including the backup systems inside data centers themselves.

In July 2025, China’s Ministry of Commerce restricted exports of technologies used to produce LFP and lithium manganese iron phosphate (LMFP) cathode active materials. The controls target production know-how rather than physical shipments, but they signal Beijing’s awareness that LFP technology is a strategic asset and its willingness to use that advantage against downstream industries including AI data centers, electricity networks, and defense. The Democratic Republic of Congo’s February 2025 decision to halt cobalt exports in response to a prolonged price collapse further illustrates how concentrated supply chains create leverage for producing countries.

The Scale of Battery Import Dependence

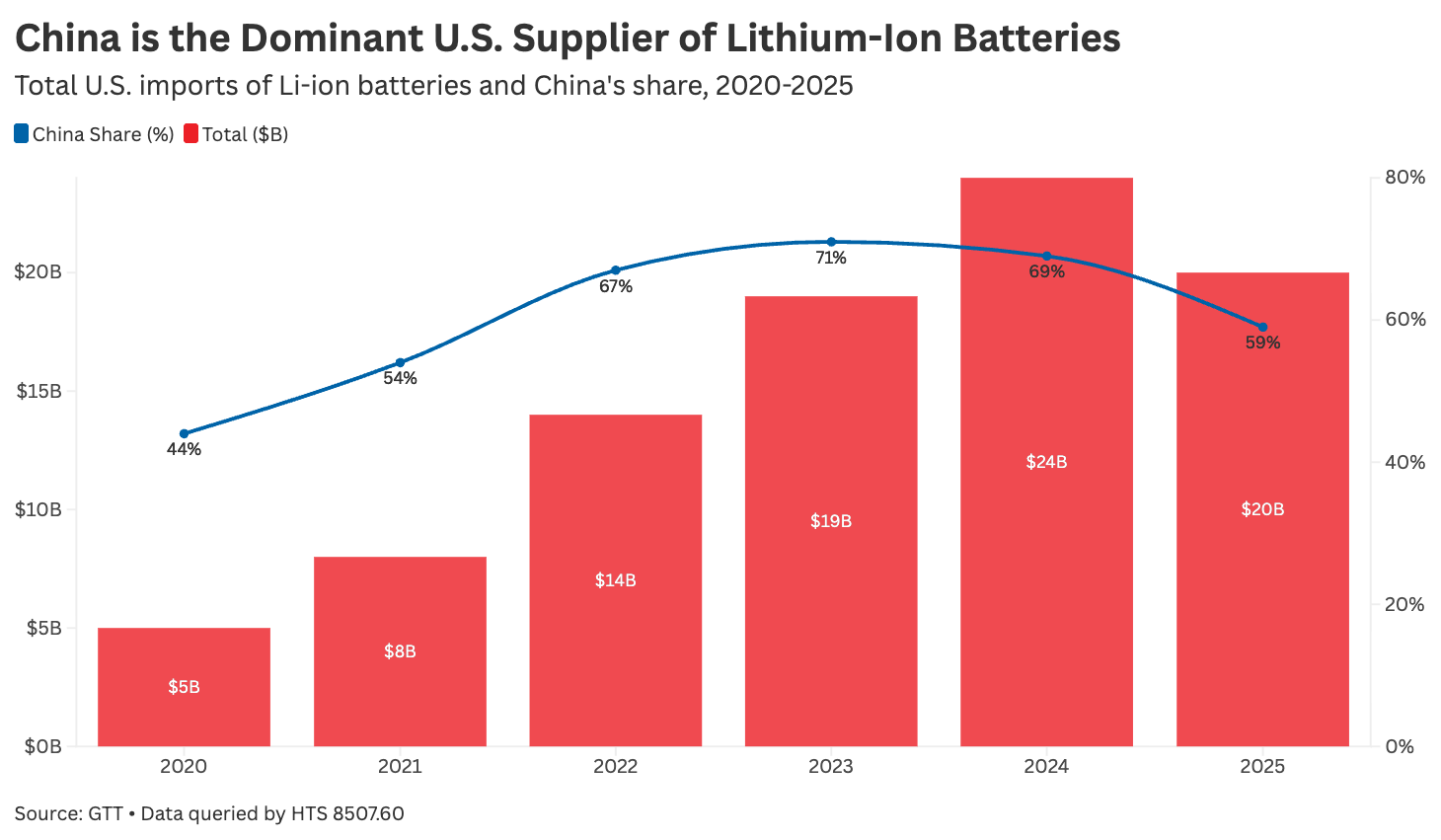

The trade data confirm the scope of this dependence. U.S. Census Bureau data show that total lithium-ion battery imports under HTS 8507.60 nearly quintupled from $4.8 billion in 2020 to $23.8 billion in 2024. China’s share of those imports by value rose from 44% in 2020 to a peak of 71% in 2023, before declining to 69% in 2024 and 59% in 2025 as tariffs began to take effect (Figure 6).

FIGURE 6:

In dollar terms, Chinese lithium-ion battery shipments to the United States grew from $2.1 billion in 2020 to $16.5 billion in 2024, an eightfold increase in four years. CATL is the leading supplier of large-scale energy storage systems to the United States, where official data show China accounts for the majority of battery and energy storage system imports.

The midstream concentration extends well beyond cathodes. China refines approximately 73% of global cobalt, 68% of nickel, 59% of lithium, and processes roughly 90% of battery-grade graphite. The United States and its allies possess substantial mineral resources and retain competitive manufacturing capabilities, but the refining and chemical conversion stages are heavily concentrated in China.

Chinese manufacturers have been able to absorb tariffs because their export margins are far higher than their domestic margins. BofA Global Research estimates that profit margins on energy storage system exports are three to five times greater than on domestic sales. HSBC noted in late 2025 that there had been significant “frontloaded installation in the U.S. ahead of the implementation of the foreign entity of concern requirements.”

Total U.S. lithium-ion imports jumped 26% from $18.9 billion in 2023 to $23.9 billion in 2024, with December 2024 marking an all-time high for monthly Chinese battery exports to the United States as buyers rushed to secure supply before new restrictions took effect.

The Iran-Israel war that erupted in March 2026 has since added more than $70 billion to the combined market capitalization of CATL, BYD, and Sungrow, as analysts project the conflict will accelerate global battery demand and with it China’s pricing leverage over buyers who have few alternative suppliers.

Transformers and Switchgear: The Rest of the Power Chain

Every data center requires three categories of electrical equipment to function. Transformers step voltage down from the transmission grid to levels the facility can use. Switchgear distributes power safely across the building. Batteries smooth load spikes and provide backup during grid interruptions. Where those components come from matters for the resilience of the buildout.

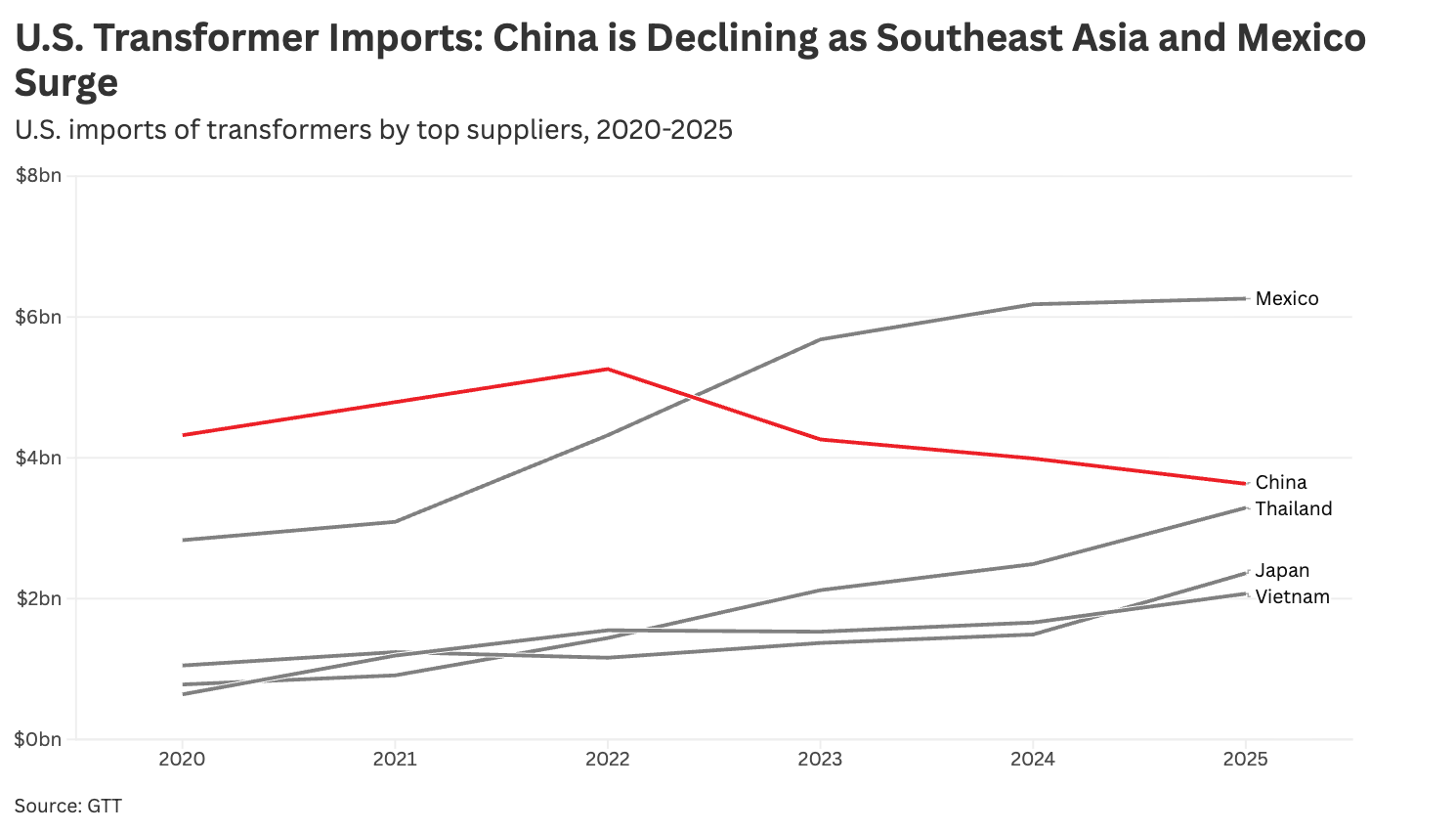

U.S. transformer imports (HTS 8504) have more than doubled since 2020, from $16.1 billion to $35.4 billion in 2025. The supplier story is markedly different from batteries. Mexico is the leading supplier at $6.3 billion, followed by China at $3.6 billion, Thailand at $3.3 billion, and Japan at $2.4 billion. China’s share of U.S. transformer imports has declined steadily, from roughly 27% in 2020 to 10% in 2025, as tariffs reduced the competitiveness of direct Chinese shipments (Figure 7).

FIGURE 7:

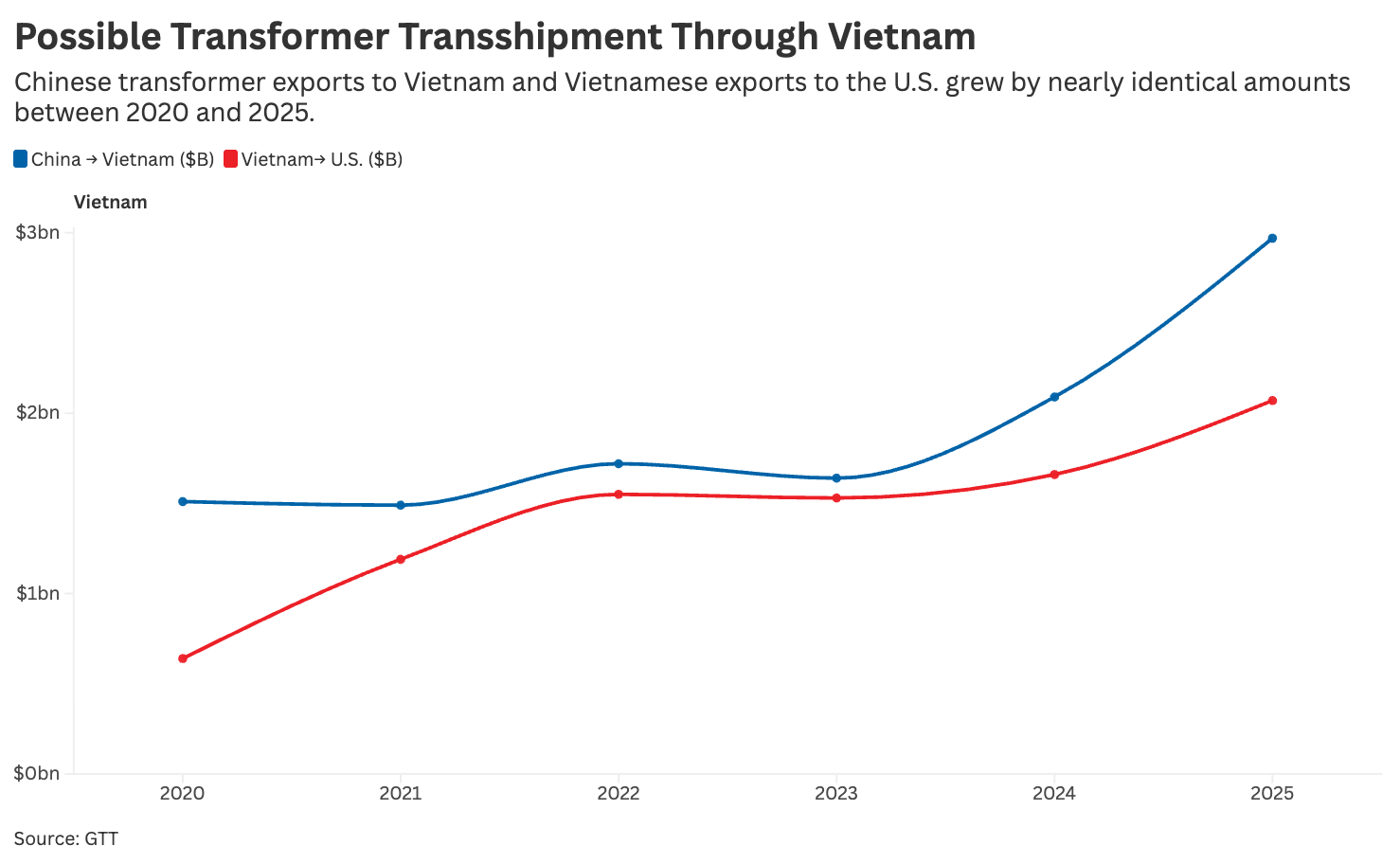

The decline in direct Chinese transformer exports to the United States, however, coincided with a surge in Chinese transformer exports to third countries that are simultaneously expanding their own exports to the United States. Chinese transformer exports to Vietnam grew from $1.5 billion in 2020 to $3.0 billion in 2025. Over the same period, U.S. imports of transformers from Vietnam grew from $0.6 billion to $2.1 billion, an increase of $1.4 billion that nearly matches the $1.5 billion increase in Chinese shipments to Vietnam. The near 1:1 correspondence between these flows is a signature of potential transshipment, where Chinese-origin goods are routed through a third country to avoid U.S. tariffs (Figure 8).

FIGURE 8:

Thailand presents a mixed picture. Chinese transformer exports to Thailand grew by $1.1 billion, while Thai transformer exports to the United States grew by $2.5 billion, suggesting a combination of genuine Thai production expansion and some pass-through of Chinese goods.

Switchgear (HTS 8537) follows yet another pattern. U.S. switchgear imports grew from $12.3 billion in 2020 to $21.7 billion in 2025. Mexico dominates this category with a 40% share ($8.8 billion), followed by Canada (9%), Germany (6%), and China (6%). China’s share is small and declining, falling from 14% to 6% over the period. Analysis of Chinese export data to Mexico confirms that Mexican switchgear production is genuine: China exported just $0.46 billion in switchgear to Mexico over the full period, compared with $41.5 billion that Mexico shipped to the United States, a ratio of approximately 90:1 that rules out significant transshipment.

The import dependence across these categories is real, even where China is not the primary supplier. Total U.S. imports of transformers, switchgear, and lithium-ion batteries combined grew from $33.2 billion in 2020 to $77.1 billion in 2025. Every new data center built requires this equipment, and the United States produces very little of it domestically.

Equipment Shortages Are Already Slowing the Buildout

The import dependencies documented in this report are already constraining data center deployment. As of April 2026, almost half of U.S. data centers planned for this year are expected to be delayed or canceled, with shortages of transformers, switchgear, and batteries among the primary causes. A separate analysis found that almost 40% of projects due this year are at risk of falling behind schedule by more than three months, including projects tied to Microsoft and OpenAI. Only a third of the 12 gigawatts of data center capacity planned for 2026 is currently under construction, according to Sightline Climate.

These challenges are further benefitting China in its AI competition with the United States. While the U.S. struggles with grid capacity, China has built the equivalent of the entire U.S. power grid in the past four years.

Transformer lead times illustrate the severity. Before 2020, high-power transformers typically arrived 24 to 30 months after an order was placed. That timeline has stretched to as long as five years. U.S. utilities imported more than 8,000 high-power transformers from China through October 2025, up from fewer than 1,500 in all of 2022, according to Wood Mackenzie. A group of U.S. utility executives who visited a Chinese transformer factory in January 2026 found that roughly half the units on the production floor were destined for the United States. Crusoe Energy, the company building OpenAI’s 1.2 GW data center campus in Abilene, Texas, has resorted to refurbishing transformers from shuttered power plants as a stopgap.

Electrical infrastructure accounts for less than 10% of total data center construction costs. It is relatively inexpensive but acutely scarce. The categories of power equipment driving the longest delays are the same ones the United States sources most heavily from abroad.

The Policy Squeeze

Washington is tightening the rules on Chinese battery content in federally subsidized energy projects, but the policy is creating a compliance gap that may be difficult to close.

The One Big Beautiful Bill Act (OBBBA), signed on July 4, 2025, extended Foreign Entity of Concern (FEOC) restrictions to six additional clean energy tax credits, including the Section 48E investment tax credit and Section 45Y production tax credit that energy storage projects rely on. Beginning in 2026, projects must demonstrate that at least 60% of the value of their battery materials comes from sources other than prohibited foreign entities. That threshold will escalate by 5-10 percentage points annually.

At the same time, Section 301 tariffs on Chinese non-EV batteries rose from 7.5% to 25% on January 1, 2026, and the administration has signaled plans to raise the combined tariff rate to 48.4%. Unlike wind, solar, and electric vehicle credits, battery storage production tax credits survived the OBBBA intact.

These policies are producing results at the final assembly stage. U.S. manufacturing capacity for fully assembled energy storage systems jumped from 7 GWh in 2023 to roughly 70 GWh by early 2026, according to the U.S. Energy Storage Coalition, and domestic battery cell manufacturing grew from zero in 2024 to 20 GWh, enough to supply about a third of the domestic cell market. Combined tariffs and tax credits have narrowed the cost gap between domestic and Chinese battery systems enough that utilities are beginning to prefer domestic procurement.

Yet despite this progress at the assembly stage, the supply chain remains exposed; about two-thirds of battery cells installed in the United States last year were imported, and the cathode active materials inside those cells remain overwhelmingly Chinese regardless of where final assembly takes place. System-level self-sufficiency masks the midstream chokepoint that determines actual supply chain security.

U.S. battery manufacturers have aggressive buildout plans that depend on qualifying for these tax credits. They cannot source non-Chinese LFP cathode materials at scale, because no significant non-Chinese supply exists. If manufacturers cannot meet FEOC compliance requirements, much of the announced domestic capacity may never materialize.

At the same time, alternative supply has been so slow to materialize. China’s state-backed overcapacity allows domestic producers to flood global markets at prices well below Western break-even rates, making private investment in alternative refining and processing capacity commercially risky without substantial government support. CATL alone received more than $500 million in Chinese government subsidies in the first half of 2024, according to its filings, capital that underwrites the pricing power Western competitors cannot match. In addition, opaque licensing regimes prevent foreign buyers from building safety stockpiles, keeping them dependent on Chinese supply even as they seek alternatives.

Ford’s partnership with CATL illustrates the tensions. Ford’s existing licensing agreement predates the OBBBA and is reportedly grandfathered under the new FEOC rules. The arrangement means that one of the largest domestic grid-scale battery production programs is built on Chinese technology, raising questions about whether the policy framework is actually reducing strategic dependence or simply deferring it.

Policy Recommendations

Tariffs and export controls have reshaped the computing half of the data center supply chain. They have not yet touched the power half in any meaningful way. Three distinct patterns of import dependence emerged from the data, and each requires a different policy response.

For servers, tariffs and export controls drove sourcing away from China, but production relocated to other import sources rather than to the United States. For transformers, the decline in direct Chinese imports coincided with a surge in Chinese exports to the same Southeast Asian countries now shipping to the United States, raising serious questions about tariff evasion. For batteries, China remains the dominant direct supplier, and its control over upstream cathode materials means that even domestically assembled batteries depend on Chinese inputs. Seven steps deserve immediate attention.

1. Incentivize domestic production of data center computing hardware.

China’s share of U.S. server imports fell from 51% to 4%, but the United States still imports more than 95% of its servers. Taiwan alone supplies $86 billion in ADP equipment. A disruption in the Taiwan Strait would expose how little the diversification strategy has done to reduce actual supply chain risk. Section 48D semiconductor investment credits and 45X advanced manufacturing credits should be extended to cover server and data processing equipment assembly, not just chip fabrication. The Taiwan ODMs now building assembly capacity in Texas and northern Mexico represent an opportunity to anchor more of this production in North America permanently.

2. Investigate transformer rerouting through Southeast Asia.

The near 1:1 correspondence between rising Chinese transformer exports to Vietnam ($1.5 billion increase) and rising Vietnamese transformer exports to the United States ($1.5 billion increase) warrants formal investigation by the U.S. International Trade Commission and U.S. Customs and Border Protection. The Commerce Department should initiate anti-circumvention inquiries under existing antidumping and countervailing duty frameworks. If Chinese-origin transformers are being relabeled in transit, the tariff wall intended to incentivize domestic production is being undermined.

3. Expand domestic transformer manufacturing capacity.

U.S. transformer imports more than doubled from $16.1 billion to $35.4 billion between 2020 and 2025. Every new data center requires step-down transformers, and lead times for large power transformers already exceed two years.

On April 20, 2026, the White House issued a Presidential Determination under Section 303 of the Defense Production Act finding that grid infrastructure — including transformers, substations, high-voltage circuit breakers, and electrical core steel — is essential to national defense and that domestic industry cannot meet demand in a timely manner. Federal procurement preferences and the authorities unlocked by this determination should be directed toward expanding domestic transformer production, particularly for the high-voltage units data centers require.

4. Strengthen 45X production incentives for midstream battery processing.

Section 45X of the Inflation Reduction Act provides production credits for domestic manufacturing, but its effectiveness for battery materials depends on extending eligibility beyond 2030 and aligning credit horizons with the capital investment cycles required to build refining infrastructure. Cathode active material production should be an explicit priority within the 45X framework.

5. Enforce FEOC restrictions based on ownership and control at the processing stage.

Current rules can be circumvented through layered ownership structures and intermediary jurisdictions. Federal tax credits, procurement programs, and clean energy incentives should treat minerals as adversary-origin when Chinese entities exercise ownership or control over refining or processing, regardless of where extraction occurs or where the processing physically takes place.

6. Invest in allied cathode processing networks.

The United States cannot build sufficient LFP cathode capacity domestically in the near term. Coordinated investment with allied partners in South Korea, Japan, Australia, and Taiwan should be structured through the Minerals Security Partnership and supported by long-term offtake commitments that give allied processors confidence to invest.

7. Accelerate support for alternative battery chemistries and use the Defense Production Act for critical battery materials.

Sodium-ion and iron-air batteries use inputs that are more geographically diversified and less dependent on Chinese-controlled processing. Google’s partnership with Form Energy for a 300-megawatt iron-air battery system in Minnesota demonstrates commercial viability. Federal research investment through ARPA-E and the Department of Energy should prioritize scaling these technologies. Simultaneously, LFP cathode materials should be designated as critical to national defense, enabling Title III investments, government offtake agreements, and strategic stockpiling.

8. Support a Section 232 investigation into power grid equipment.

The United States imports 80% of its power transformer supply, and demand for this equipment has surged 116% since 2019. Data centers, renewable energy projects, and EV charging infrastructure are all competing for the same limited domestic manufacturing base.

A Section 232 finding that power grid equipment imports threaten national security would give the administration legal authority to impose tariffs or quotas specifically designed to incentivize domestic transformer and switchgear production, complementing the DPA Title III approach in recommendation #3. The Commerce Department has already launched Section 232 investigations into semiconductors, critical minerals, and other strategic sectors in FY 2025; power grid equipment warrants the same treatment.

Conclusion

The data center buildout has exposed three distinct failures in U.S. trade and industrial policy. For computing hardware, tariffs and export controls succeeded in moving sourcing away from China but failed to bring production home — the United States still imports virtually all of its servers. For transformers, tariffs appear to have moved the shipping route rather than the supply chain, with Chinese exports flowing through Vietnam and Thailand on their way to U.S. data centers. For lithium-ion batteries, tariffs have barely dented China’s dominance, and the upstream cathode materials that determine actual supply chain security have no non-Chinese source at any scale.

Across the full data center equipment stack, the United States imported $653 billion worth of hardware in 2025, more than double the $313 billion it imported five years earlier. The buildout is accelerating, not slowing. Every new facility requires servers, transformers, switchgear, and batteries, and the United States manufactures very little of any of them domestically.

The policy tools exist. Production tax credits can make domestic manufacturing competitive. FEOC restrictions can ensure federal dollars flow to genuinely independent supply chains. Anti-circumvention investigations can close the transformer rerouting loophole. The Defense Production Act can designate critical battery materials for strategic stockpiling. Allied investment partnerships can build cathode processing capacity outside China. Washington proved it can redirect trade flows. It has not yet proved it can rebuild industrial capacity. The data center buildout will determine which matters more.

REFERENCES

Benchmark Mineral Intelligence. “China Implements Export Restrictions on Cathode and Lithium Production Technologies.” July 2025. https://source.benchmarkminerals.com/article/china-implements-export-restrictions-on-cathode-and-lithium-production-technologies.

Benchmark Mineral Intelligence. “What’s the Impact of China’s Proposed Export Controls on Lithium and Cathode Technologies?” Cathode Forecast, 2025. https://source.benchmarkminerals.com/video/watch/whats-the-impact-of-chinas-proposed-export-controls-on-lithium-and-cathode-technologies.

Bipartisan Policy Center. “Unpacking the FEOC Provisions in the One, Big, Beautiful Bill Act.” 2025. https://bipartisanpolicy.org/explainer/unpacking-the-feoc-provisions-in-the-one-big-beautiful-bill-act/.

Birol, Fatih. “Batteries Are Crucial Technology for the 21st Century.” Financial Times, October 30, 2025. https://www.businesstimes.com.sg/opinion-features/batteries-are-crucial-technology-21st-century.

Coalition for a Prosperous America and Responsible Battery Coalition. Securing the Battery Supply Chain: Wartime Footing — How the United States Can Reverse China’s Dominance of Battery Minerals Processing. Washington, DC: CPA, 2026. https://prosperousamerica.org/wp-content/uploads/2026/03/CPAxRBC-Economics-Report-Wartime-Footing-How-the-United-States-Can-Reverse-Chinas-Dominance-of-Battery-Minerals-Processing.pdf.

Chan, Kyle I. “Testimony before the U.S. House Select Committee on Strategic Competition Between the United States and the Chinese Communist Party, Hearing on ‘China’s Campaign to Steal America’s AI Edge.'” April 16, 2026. https://democrats-selectcommitteeontheccp.house.gov/sites/evo-subsites/democrats-selectcommitteeontheccp.house.gov/files/evo-media-document/mr-kyle-chan-written-testimony-scc-hearing-4.16.pdf.

“Americans’ Electricity Bills Are Up. Don’t Blame AI.” The Economist, March 5, 2026. https://www.economist.com/finance-and-economics/2026/03/05/americans-electricity-bills-are-up-dont-blame-ai.

fDi Intelligence (Financial Times). “Data Centers by the Numbers.” 2025. https://www.fdiintelligence.com/content/07d8bc90-96c9-4978-bea9-72e2f0185c11.

Forgash, Naureen S., and Akshat Rathi. “America’s AI Build-Out Hinges on Chinese Electrical Parts.” Bloomberg, April 1, 2026. https://www.bloomberg.com/news/features/2026-04-01/us-ai-data-center-expansion-relies-on-chinese-electrical-equipment-imports.

Gallagher, Mary E., and Joyce Yang. “Does Chinese Investment in US Clean Energy Sectors Help or Hurt America?” Brookings Institution, March 12, 2026. https://www.brookings.edu/articles/does-chinese-investment-in-us-clean-energy-sectors-help-or-hurt-america/.

Goreichy, Esther, and Jacob Gunter. “China’s Overcapacity Threatens to Reshuffle Global Industrial Bases.” MERICS (Mercator Institute for China Studies), February 10, 2026. https://merics.org/en/comment/chinas-overcapacity-threatens-reshuffle-global-industrial-bases.

Hook, Leslie, and Tom Wilson. “DR Congo Stops Cobalt Exports in Attempt to Halt Sliding Prices.” Financial Times, February 24, 2025. https://www.ft.com/content/1d4f5517-545c-47cb-b9f4-f7c48607919a.

Irwin-Hunt, Alex. “Data Centres in 2025: Global Capacity Rush Hits Hurdles.” fDi Intelligence (Financial Times), December 22, 2025. https://www.fdiintelligence.com/content/13f1ece9-ae73-475b-a40e-2e91d5d3ed6c.

Irwin-Hunt, Alex. “The US AI Boom Drives Trade and Investment Surge.” fDi Intelligence (Financial Times), October 22, 2025. https://www.fdiintelligence.com/content/ab0303e8-c92d-421e-8663-b2598c147cec.

Kelly, Brendan. “Taiwan Firms Key to Nearshoring and Reshoring to Support AI Boom.” Federal Reserve Bank of Dallas, March 6, 2026. https://www.dallasfed.org/research/pubs/25trade/a4.

Kok, Erikhans, Johan Rauer, Pankaj Sachdeva, and Piotr Pikul. “Scaling Bigger, Faster, Cheaper Data Centers with Smarter Designs.” McKinsey & Company, August 1, 2025. https://www.mckinsey.com/industries/private-capital/our-insights/scaling-bigger-faster-cheaper-data-centers-with-smarter-designs.

Lee, Jinjoo. “As EV Market Stalls, Battery Makers Shift to Grids and Data Centers.” Wall Street Journal, March 19, 2026. https://www.wsj.com/business/autos/as-ev-market-stalls-battery-makers-shift-to-grids-and-data-centers-78cc2276.

Lombardo, Teo, Leonardo Paoli, Araceli Fernandez Pales, and Timur Gul. “The Battery Industry Has Entered a New Phase.” International Energy Agency, March 5, 2025. https://www.iea.org/commentaries/the-battery-industry-has-entered-a-new-phase.

Ma, Michelle. “AI Boom Drives US to Build Enough Battery Systems for Domestic Demand.” Bloomberg, March 18, 2026. https://www.bloomberg.com/news/articles/2026-03-18/ai-boom-drives-us-to-build-enough-battery-systems-for-domestic-demand.

McKinsey & Company. “The Cost of Compute: A $7 Trillion Race to Scale Data Centers.” 2025. https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/the-cost-of-compute-a-7-trillion-dollar-race-to-scale-data-centers.

Mitra Chem. “US Department of Energy Selects Mitra Chem for $100 Million Award for Domestic Battery Manufacturing.” Press release, September 2025. https://www.mitrachem.com/post/us-department-of-energy-selects-mitra-chem-for-100-million-award-for-domestic-battery-manufacturing.

O’Dea, Blathnaid. “How On-Site Batteries Are Fast-Tracking Data Center Grid Connections.” pv magazine USA, March 18, 2026. https://pv-magazine-usa.com/2026/03/18/how-on-site-batteries-are-fast-tracking-data-center-grid-connections/.

O’Kane, Sean, and Kirsten Korosec. “Ford Is Starting a Battery Storage Business to Power Data Centers and the Grid.” TechCrunch, December 15, 2025. https://finance.yahoo.com/news/ford-starting-battery-storage-business-211745514.html.

Otts, Christopher. “GM Will Import EV Batteries From China’s CATL Despite Tariffs.” Wall Street Journal, August 7, 2025. https://www.wsj.com/business/autos/gm-bolt-china-ev-batteries-1562e2f7.

Rosner-Uddin, Nian, Amanda Chu, and David Sheppard. “Data Centre Delays Threaten to Choke AI Expansion.” Financial Times, April 17, 2026. https://finance.yahoo.com/sectors/technology/articles/half-planned-us-data-center-150928890.html.

Samsung SDI. “Samsung SDI Wins KRW 1.5 Trillion ESS Prismatic Battery Supply Deal in the U.S.” Samsung SDI Newsroom, March 16, 2026. https://news.samsungsdi.com/global/articleView?seq=390.

Sandlund, William. “Investors Bet on Chinese Companies Powering Global AI Build-Out.” Financial Times, December 15, 2025. https://www.ft.com/content/ea276954-7dab-49be-a152-98caa95e8c9d.

Sandlund, William, and Edward White. “China Battery Trio Gain $70bn as Iran War Sparks ‘Paradigm Shift.'” Financial Times, March 23, 2026. https://www.ft.com/content/b122ca1f-fc99-4749-9764-f1998b84dd07.

Shirouzu, Norihiko, Nathan Gomes, and Akash Sriram. “Automakers Expand US Battery Storage Supply but China Still Key.” Reuters, April 13, 2026. https://www.reuters.com/business/energy/automakers-expand-us-battery-storage-supply-china-still-key–reeii-2026-04-13/.

Shivakumar, Sujai, Charles Wessner, and Thomas Howell. “Balancing the Ledger: Export Controls on U.S. Chip Technology to China.” Center for Strategic and International Studies, February 21, 2024. https://www.csis.org/analysis/balancing-ledger-export-controls-us-chip-technology-china.

St. John, Jeff. “Amid Tariff Uncertainty, US Grid Battery Industry Faces an Uphill Climb.” Canary Media, May 13, 2025. https://www.canarymedia.com/articles/energy-storage/tariffs-tax-credits-grid-battery-trump.

Stylianou, Nassos, et al. “How Mega Batteries Are Unlocking an Energy Revolution.” Financial Times, October 13, 2025. https://ig.ft.com/mega-batteries/.

Thomas, Devin, Benjamin Boucher, and Michael Mendrek-Laske. “Transformer Troubles: Manufacturing and Policy Constraints Hit US Transformer Supply.” Wood Mackenzie, August 13, 2025. https://www.woodmac.com/news/opinion/transformer-troubles-manufacturing-and-policy-constraints-hit-us-transformer-supply/.

U.S. Energy Information Administration. “U.S. Battery Capacity Increased 66% in 2024.” Today in Energy, 2025. https://www.eia.gov/todayinenergy/detail.php?id=64705.

Vasdev, Amar. “Battery Storage Costs Hit Record Lows as Costs of Other Clean Power Technologies Increased.” BloombergNEF, February 18, 2026. https://about.bnef.com/insights/clean-energy/battery-storage-costs-hit-record-lows-as-costs-of-other-clean-power-technologies-increased-bloombergnef/.

World Trade Organization. “Global Trade Outlook and Statistics, March 2026.” Geneva: WTO, 2026. https://www.wto.org/english/res_e/booksp_e/gtos0326_e.pdf.