Washington’s $70 Billion in Lost Protection: Liberation Day, One Year Later

Tracking Chinese Evasion and the Cost of U.S. Exemptions

One year after the most aggressive tariff escalation since 2018, the United States collected barely three-fifths of what its own policy prescribes. U.S. tariffs on Chinese imports carry a statutory rate that averages 62%, but the Treasury collected at an average rate of 38% during the thirteen-month period beginning in April 2025 [1]. The time period aligns with President Trump’s “Liberation Day” announcement of reciprocal tariffs against major trading partners.

This report estimates that gap cost the United States $70 billion in tariff protection ($66 billion from structural leakage created by Washington’s own policy choices, and $4 billion from Chinese evasion through third countries). The gap raises a question the tariff debate has largely ignored: whether the tariffs that have been enacted are actually being collected. If the U.S. is absorbing the political and economic costs of a 62% statutory regime, but collecting revenue as if the rate were 38%, the policy is delivering the disruption of a trade war without the corresponding competitive protection.

KEY FINDINGS

- One year after Liberation Day, the gap between what the U.S. tariff schedule prescribed on Chinese imports and what the Treasury collected reached an estimated $70 billion. Structural leakage from exclusions, bonded warehouse deferrals, and enforcement shortfalls accounts for $66 billion of that gap. Transshipment — the rerouting of Chinese goods through third countries to enter the United States at lower duty rates — accounts for another $4 billion.

- Nearly one in five dollars of Chinese trade diverted since Liberation Day suggests transshipment. Of the $75 billion redirected to the seventeen third-market partners covered by this analysis, an estimated $14 billion (19%) shows statistical patterns consistent with transshipment back into the American market. This diversion represents roughly 60% of the $122 billion annualized decline in direct Chinese exports to the United States during the analysis period.

- ASEAN is the dominant transshipment corridor, and electronics are the dominant product category. The Southeast Asian trading bloc absorbed $9 billion of the $14 billion in estimated transshipment, with 64% of Chinese trade diverted to the region showing signs of re-export to the United States. Computers, telecommunications equipment, and electrical machinery account for 41% of all transshipment and flow overwhelmingly through ASEAN assembly operations.

- The USMCA corridor is small, but carries the widest tariff gap of any corridor. Effective rates in both Canada and Mexico sit more than 30 percentage points below China’s, meaning every dollar rerouted through USMCA avoids more duty than through any other channel. That gap is directly at stake in the July 2026 renegotiation of the U.S.-Mexico-Canada Agreement (USMCA).

Background

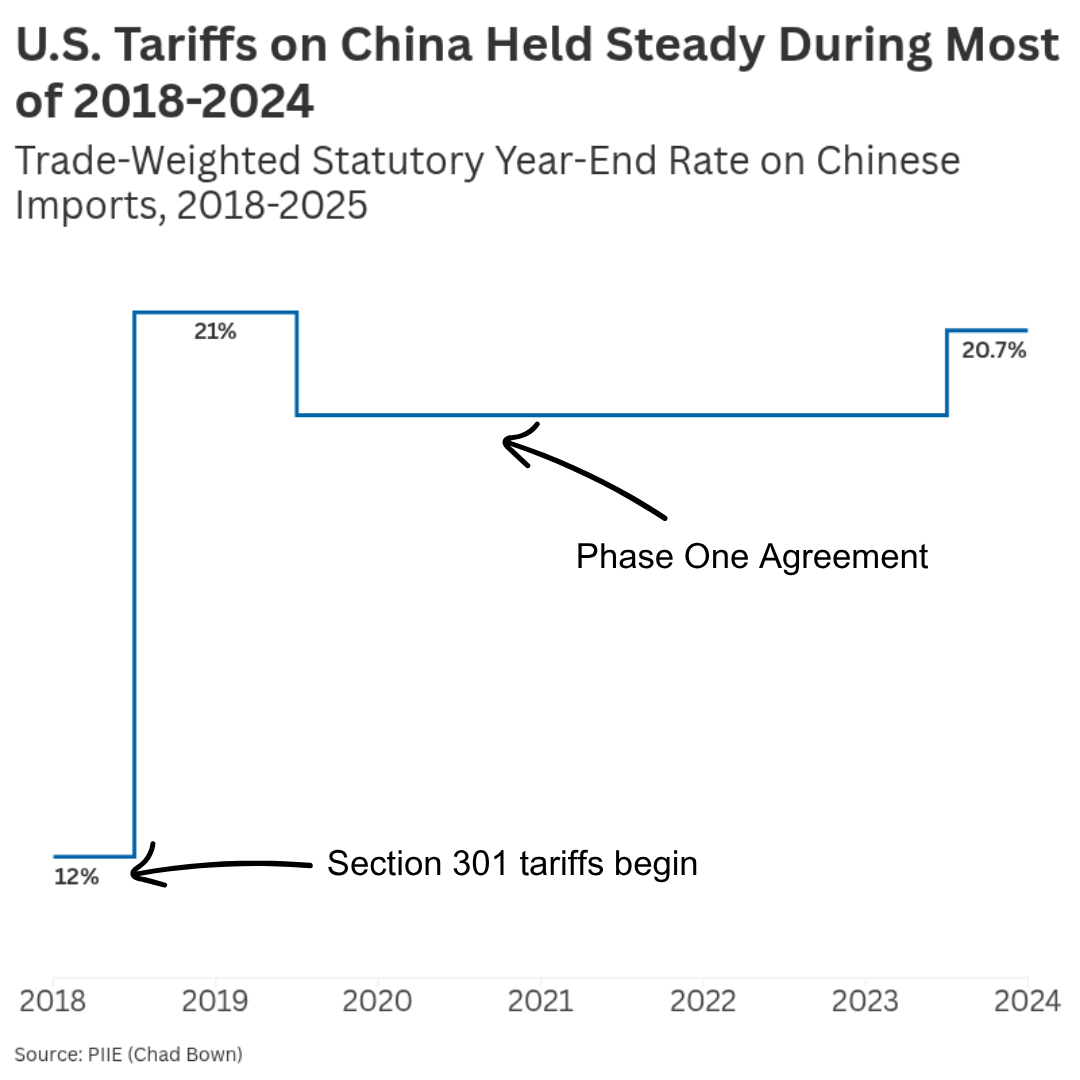

The United States has imposed tariffs on Chinese goods since 2018 to counter the structural cost advantages that Beijing’s industrial policies have given Chinese exporters: below-market financing, subsidized energy and land, forced technology transfer, and currency management. By one measure, the policy has worked. The bilateral trade deficit with China has fallen by roughly 50% since 2018, reaching $221 billion in 2025.

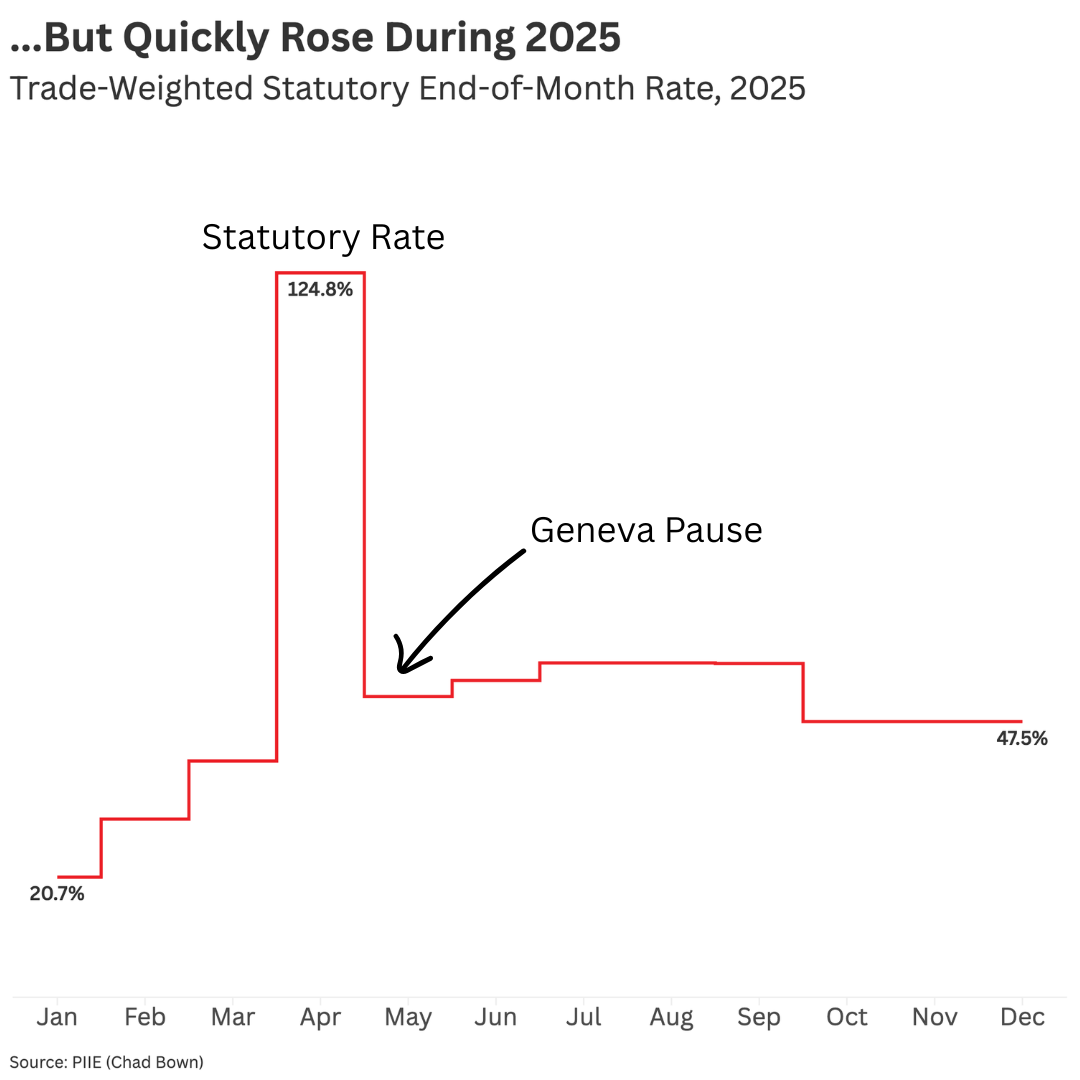

The tariff regime escalated sharply on April 2, 2025, when the second Trump Administration imposed reciprocal tariffs that pushed statutory rates above 100% (Figure 1). The Geneva pause in May reduced the combined rate to about 50%, but the effective tariff on Chinese imports remained at historically elevated levels through the end of 2025, sustaining the conditions for large-scale trade rerouting throughout this analysis period.

FIGURE 1

A shrinking bilateral deficit does not mean the underlying trade flows have disappeared. Beijing has a well-documented pattern of responding to U.S. trade enforcement by relocating production to jurisdictions with more favorable tariff treatment. From solar cells to kitchen cabinets, Chinese producers have responded to AD/CVD orders by shifting final assembly to the Association of Southeast Asian Nations (ASEAN), and the Department of Commerce confirmed the rerouting in both cases [2].

The rerouting incentive has grown with rising tariff rates. When Section 301 duties averaged 19–20%, the arbitrage for routing goods through a third country was meaningful but manageable. However, post-Liberation Day rates have raised the incentives to divert trade.

For example, a Chinese exporter facing a 50% tariff on direct shipment to the United States can cut the effective rate to 5–10% by routing through a USMCA partner or a low-tariff ASEAN economy. The savings on a single container of electronics can exceed $100,000. At that margin, a minimal-processing operation in Vietnam or Mexico pays for itself almost immediately.

Measuring the scale of this rerouting has proved difficult. Individual enforcement actions capture fragments of the problem, while aggregate trade statistics lack the product-level detail needed to identify specific evasion corridors.

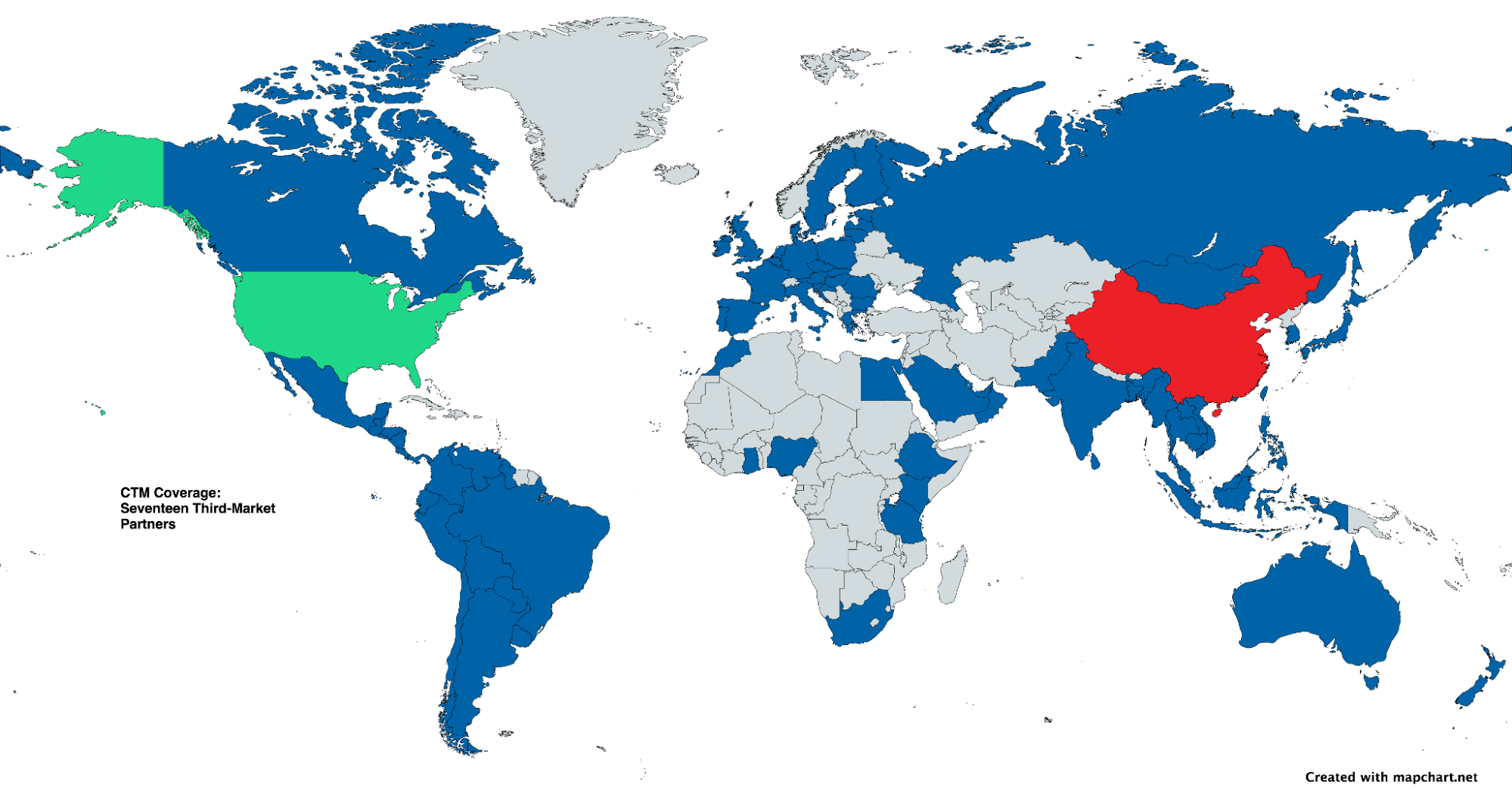

The CPA China Transshipment Monitor (CTM) introduced in this article is designed to fill that gap. It provides a product-level accounting of Chinese trade diversion and transshipment across seventeen third-country corridors, estimates the customs revenue lost through each channel, and compares the statutory tariff rate to what CBP actually collects [3].

Methodology

The CTM tracks three metrics at the HS6 product level for each of seventeen non-overlapping third-market partners: (1) declining Chinese exports to the United States relative to a 2022–24 annual baseline average; (2) rising Chinese exports of those same products to third markets (potential diversion); and (3) increased third-market exports of those products to the United States (potential transshipment [4]). The analysis uses customs data from Global Trade Tracker (GTT). When partner-level diversion matches exceed the China-to-U.S. decline for a given HS6 code, the CTM applies proportional allocation to prevent double-counting. Transshipment exposure is capped at the minimum of the allocated diversion and the U.S. import increase for each product-region combination.

Revenue loss is calculated on a partner-specific basis using the gap between the effective rate on Chinese imports (38%) and the effective rate on imports from each partner, both derived from USITC DataWeb calculated duties divided by customs value for the thirteen-month period. The seventeen partners are: ASEAN, the EU-27, India, Other Asia, South Korea, Mexico, Canada, Africa, the GCC, South America, Japan, Taiwan, Hong Kong, Russia, Central America, Australia and New Zealand, and the United Kingdom (Figure 2)[5].

FIGURE 2: The CTM Tracks 17 Trading Partners Across Six Continents

Third-market partners analyzed for trade diversion and transshipment, April 2025-2026.

These are upper-bound estimates. Further, matching rising Chinese exports to a region with rising U.S. imports from that region does not prove that specific goods were transshipped. Legitimate capacity expansion in third countries can coexist with transshipment.

To that end, the CTM is a screening tool designed to flag high-risk corridors for enforcement attention, not a causal estimate of evasion volumes. The revenue calculation uses partner-level average effective rates rather than product-specific rates; a product-level calculation would be more precise but the partner-level approach establishes the order of magnitude.

The $70 Billion Gap

The $70 billion gap reflects differences between the statutory rate (i.e. what Customs was supposed to collect) and the average effective rate (i.e. what Customs actually collected). In the year following Liberation Day tariffs, the 24-percentage-point gap between the two rates translated into an estimated $66 billion in structural leakage on the $277 billion in Chinese imports. Product exclusions granted on certain electronic components, industrial inputs, and medical products reduced the effective rate on qualifying goods to pre-tariff levels. Bonded warehouse entries and foreign trade zone deferrals also contribute by deferring duty assessment.

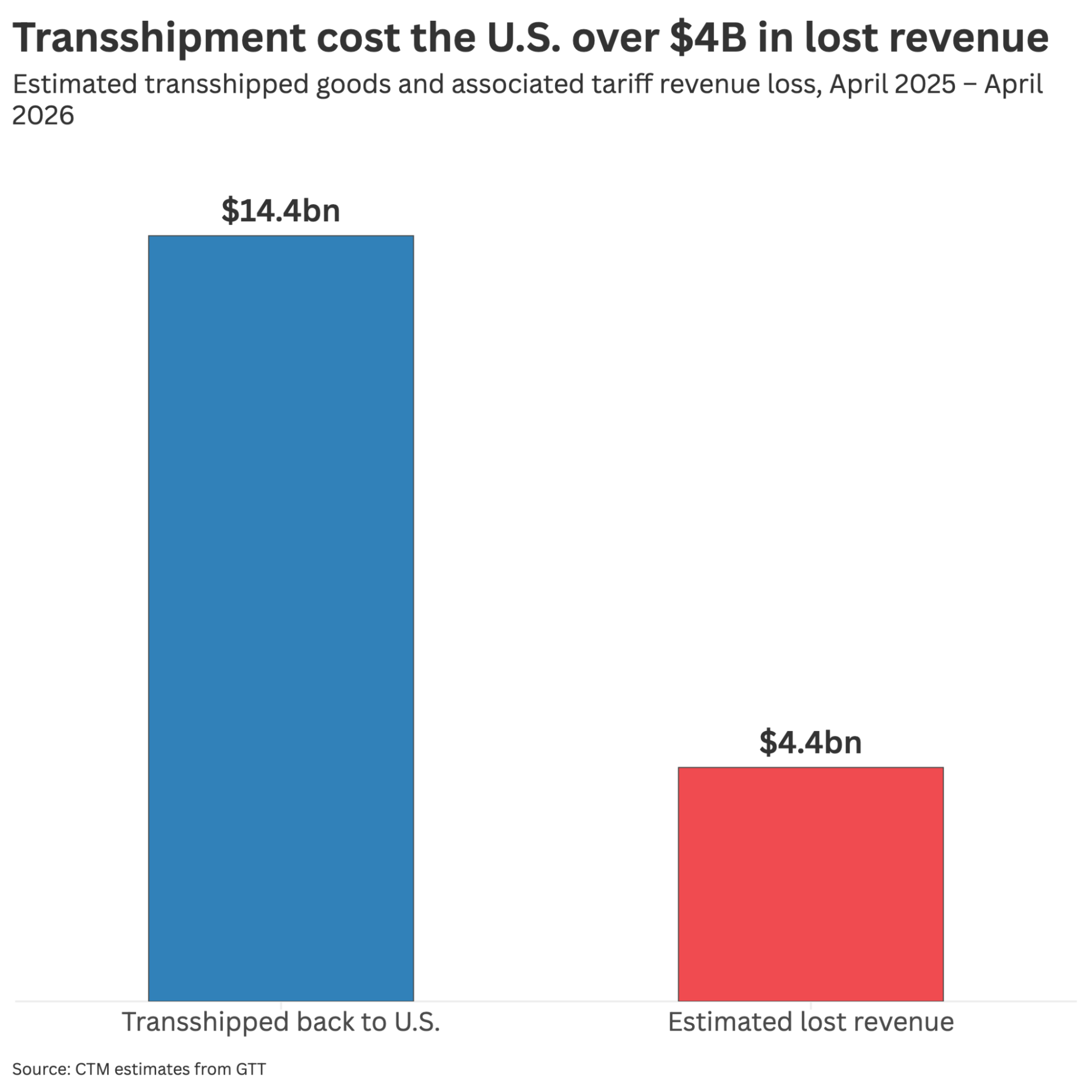

The remaining $4 billion resulted from estimated transshipment — the portion of diverted trade from China that was rerouted through third markets before arriving in the United States.

This is a critical distinction. Transshipment captures what China does to circumvent U.S. tariffs, while structural leakage captures what U.S. policy does to undermine its own tariff regime. The scale of the structural gap suggests that exclusion reform and enforcement investment would yield substantially more revenue than transshipment enforcement alone.

Some exclusions reflect deliberate policy trade-offs to avoid disrupting domestic supply chains that depend on Chinese inputs. But the scale of the gap, and its persistence since 2019, shows that the effective tariff regime on Chinese imports is far less restrictive than the statutory rates suggest. The headline rate generates political and diplomatic friction; the effective rate determines how much competitive protection domestic producers actually receive.

Trade Diversion: Where Chinese Exports Went

FIGURE 3

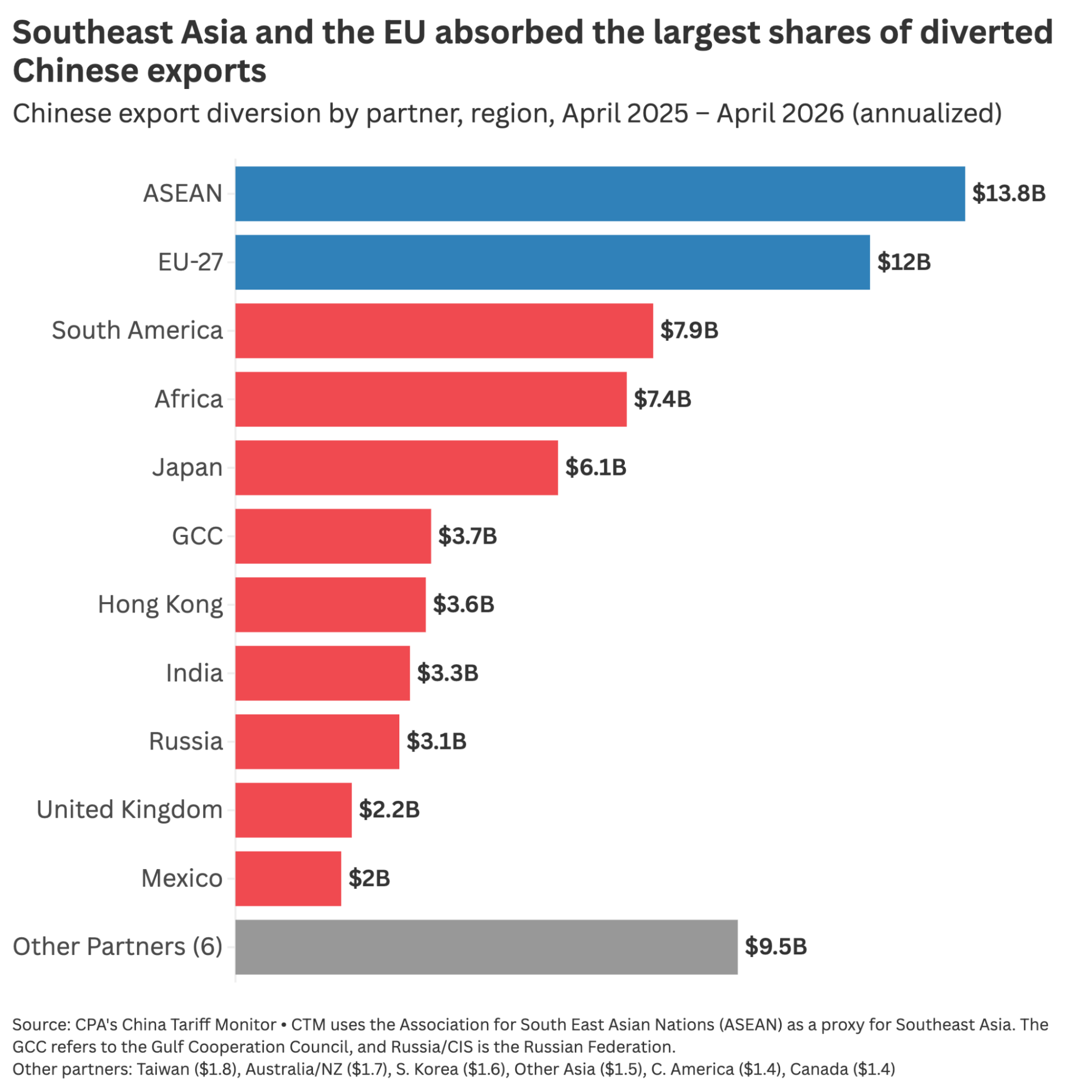

Chinese exports to the United States declined by an annualized $122 billion during the thirteen months after Liberation Day, measured against the 2022–24 annual baseline. After proportional allocation, about $75 billion of that decline, or 61%, was redirected to the seventeen third-country markets covered by the CTM. The remaining 39% is attributable to regions outside the CTM’s coverage, reduced demand, inventory drawdowns, and goods consumed in transit economies.

ASEAN and the EU absorbed the largest shares at $14 billion and $12 billion, followed by South America ($8 billion), Africa ($7 billion), and Japan ($6 billion) (Figure 3). ASEAN’s dominance reflects its existing role as a manufacturing hub with deep supply chain links to China.

India absorbed $3 billion in diverted Chinese exports. South America absorbed $8 billion, driven by Brazil, Chile, and other commodity exporters that have deepened trade ties with China. Africa absorbed $7 billion, an unexpectedly large figure that reflects Chinese infrastructure and manufacturing investments across the continent over the past decade.

Japan absorbed $6 billion, making it the fifth-largest diversion destination. At the HS6 code level, hundreds of individual product lines showed increases even as aggregate bilateral trade shifted modestly. Country-level trade balances can obscure significant product-level movements.

The largest absorption markets represent three distinct categories. ASEAN is primarily a production platform: Chinese firms use the region for final assembly and re-export. The EU and Africa are primarily absorption markets; most diverted goods are consumed domestically. South America sits in between, absorbing Chinese exports for domestic use while also, in selected product categories, providing assembly corridors for re-export. Understanding these distinctions matters for designing enforcement that targets transshipment without disrupting legitimate trade.

Transshipment: What Came Back

The more pressing question for U.S. enforcement is how much diverted trade is being rerouted back to the American market under third-country labels.

Across all seventeen partners, the CTM identifies $14 billion in maximum transshipment exposure during April 2025 to April 2026 (Table 1). This represents 19% of the $75 billion in total allocated diversion: roughly one-fifth of Chinese goods diverted to the covered partners show signs of being funneled back to the United States.

Table 1: Trade diversion and transshipment by region, April 2025 — April 2026 (Annualized)

Region | Diverted ($B) | Transshipped ($B) | T/D Ratio | % of Total |

ASEAN | $13.8 | $8.8 | 64% | 61% |

EU-27 | $12.0 | $1.8 | 15% | 12% |

India | $3.3 | $0.8 | 25% | 6% |

Japan | $6.1 | $0.5 | 8% | 3% |

Mexico | $2.0 | $0.5 | 23% | 3% |

S. America | $7.8 | $0.4 | 5% | 3% |

Taiwan | $1.8 | $0.3 | 16% | 2% |

South Korea | $1.6 | $0.3 | 16% | 2% |

Canada | $1.4 | $0.2 | 17% | 2% |

Others (8) | $24.8 | $0.9 | 3% | 6% |

Total | $74.6 | $14.4 | 19% | 100% |

Source: Global Trade Tracker, USITC DataWeb, CPA analysis. HS6 code-level matching with proportional allocation. Baseline: 2022–24 annual average. Thirteen-month data annualized (×12/13). Sorted by transshipment exposure. “Other partners” includes Africa ($254M), GCC ($253M), United Kingdom ($173M), Central America ($63M), Australia & NZ ($48M), Other Asia ($37M), Hong Kong ($20M), and Russia ($2M).

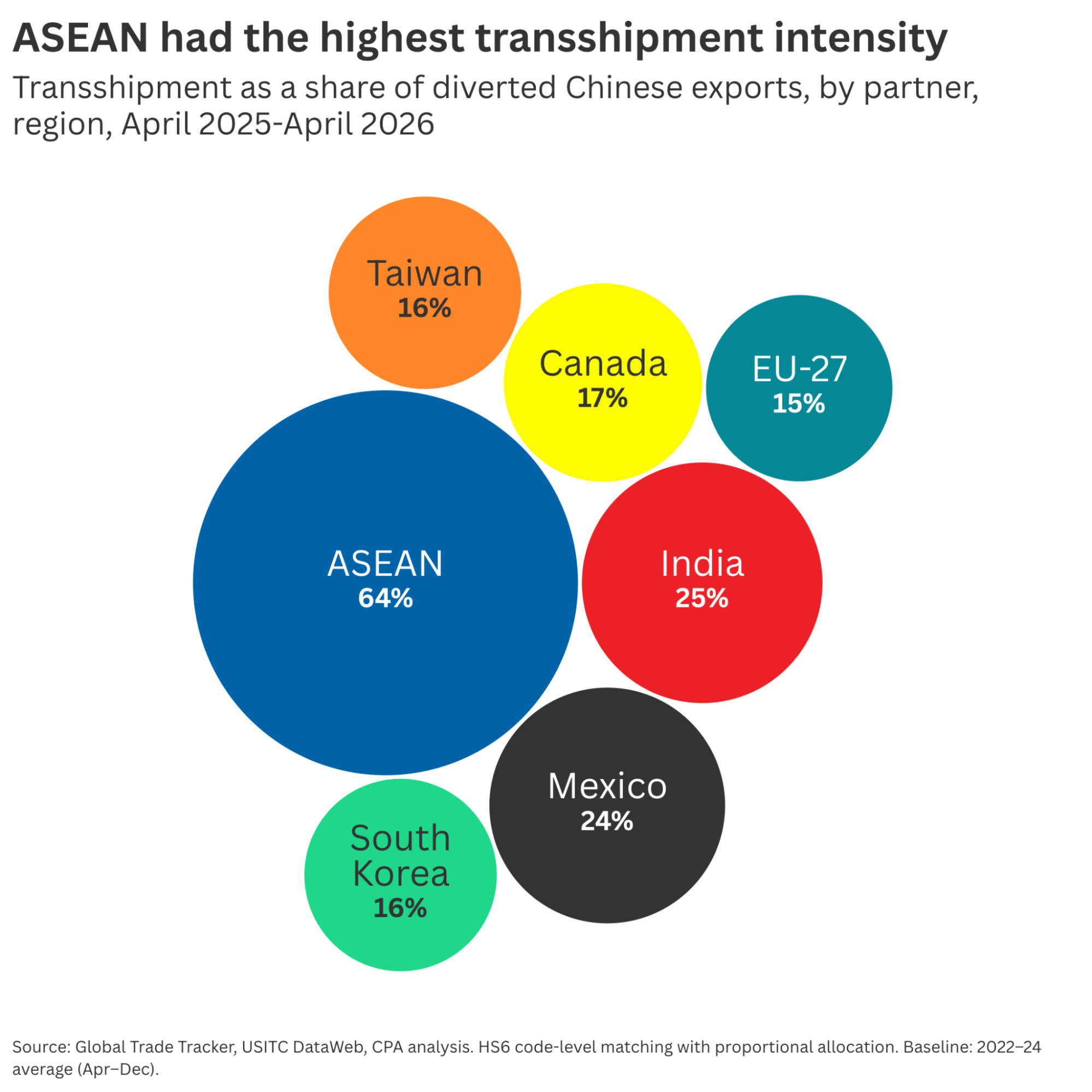

The Dominant Corridor: ASEAN

ASEAN accounts for $9 billion of the $14 billion transshipment total, more than half the global exposure concentrated in a single region. Sixty-four percent of Chinese trade diverted to ASEAN showed signs of being rerouted to the United States, the highest intensity of any partner grouping.

The pattern reflects two overlapping dynamics: the deep integration of Chinese and ASEAN electronics supply chains, where components cross borders multiple times before final assembly, and the rapid expansion of minimal-processing operations in Vietnam, Thailand, and Malaysia set up specifically to avoid U.S. tariffs on Chinese goods. Vietnamese electronics exports to the United States have grown by more than 400% since the initial Section 301 tariffs in 2018, a trajectory that far outpaces domestic capacity expansion.

The enforcement challenge is compounded by genuine economic development occurring alongside transshipment. Vietnam, Thailand, and Malaysia have all attracted real foreign direct investment in manufacturing since 2018, much of it from firms diversifying away from China. Distinguishing a factory that performs substantial transformation from one that performs only minimal processing to change the customs declaration requires product-level intelligence that CBP does not consistently possess.

The Highest-Intensity Corridors: India and Mexico

FIGURE 4

India exhibited the highest transshipment intensity of any individual country. The country’s $816 million in transshipment exposure, with a 25% intensity ratio, indicates India’s dual roles as both a market and a transshipment corridor.

India’s top transshipped products, including power converters, laptop computers, switching apparatus, and industrial valves, are consistent with the rapid expansion of Chinese-linked assembly operations in the country. India is also a target of the Section 301 overcapacity investigations launched in March 2026 (Figure 4).

Mexico showed the second-highest transshipment intensity. Although its diversion volume ($2 billion) is modest relative to ASEAN or the EU, 23% of that diverted trade shows signs of re-export to the United States.

Electronics and computing equipment accounted for roughly a third of Mexico’s transshipment exposure, led by computers and data processing equipment. Automotive products — both parts and finished passenger vehicles — made up another 13%, a finding with direct implications for the USMCA renegotiation in 2026. Household appliances including washing machines and refrigerators, industrial floor coverings, and electrical control equipment round out the profile.

The diversity of transshipped goods through Mexico distinguishes it from the ASEAN corridor, where electronics dominate. Mexico’s transshipment pattern is consistent with the broader Chinese FDI surge into the country — nearly $4 billion in deals in 2023 alone — and the growth of assembly operations in sectors ranging from electronics to auto parts.

Strategic Corridors: South Korea and Taiwan

Both economies registered 16% transshipment intensity with modest absolute volumes ($254 million and $289 million). Their significance lies in composition. South Korea’s profile is concentrated in computer parts, monitor components, and auto parts, all semiconductor-adjacent categories with strategic sensitivity. Taiwan’s exposure is concentrated in electronics components, where its central role in the global chip supply chain creates pathways for Chinese goods to enter exports bound for the United States.

These corridors are small in dollar terms but significant given the strategic sensitivity of the products. If Chinese-origin components are entering the U.S. supply chain through South Korean or Taiwanese intermediaries in categories subject to export controls, the transshipment carries implications beyond revenue loss.

The EU-27 presents a distinctive pattern. Its $2 billion in transshipment is the second-largest absolute total, but its 15% intensity ratio is among the lowest of any major corridor. Most diverted goods are consumed domestically. The transshipment that does occur is concentrated in Germany, the Netherlands, and Ireland, countries with significant logistics infrastructure and re-export capacity. Ireland’s pharmaceutical and electronics sectors create opportunities for Chinese components to be incorporated into EU-origin exports shipped to the United States.

The GCC registered $253 million in transshipment exposure, largely concentrated in the UAE. Africa’s $254 million reflects new assembly corridors in countries like Ethiopia and Morocco, where Chinese manufacturers have set up production facilities with explicit export orientation. Together with the United Kingdom ($173 million) and Central America ($63 million), these corridors account for a combined $743 million in diffuse exposure that is difficult to target through corridor-specific enforcement.

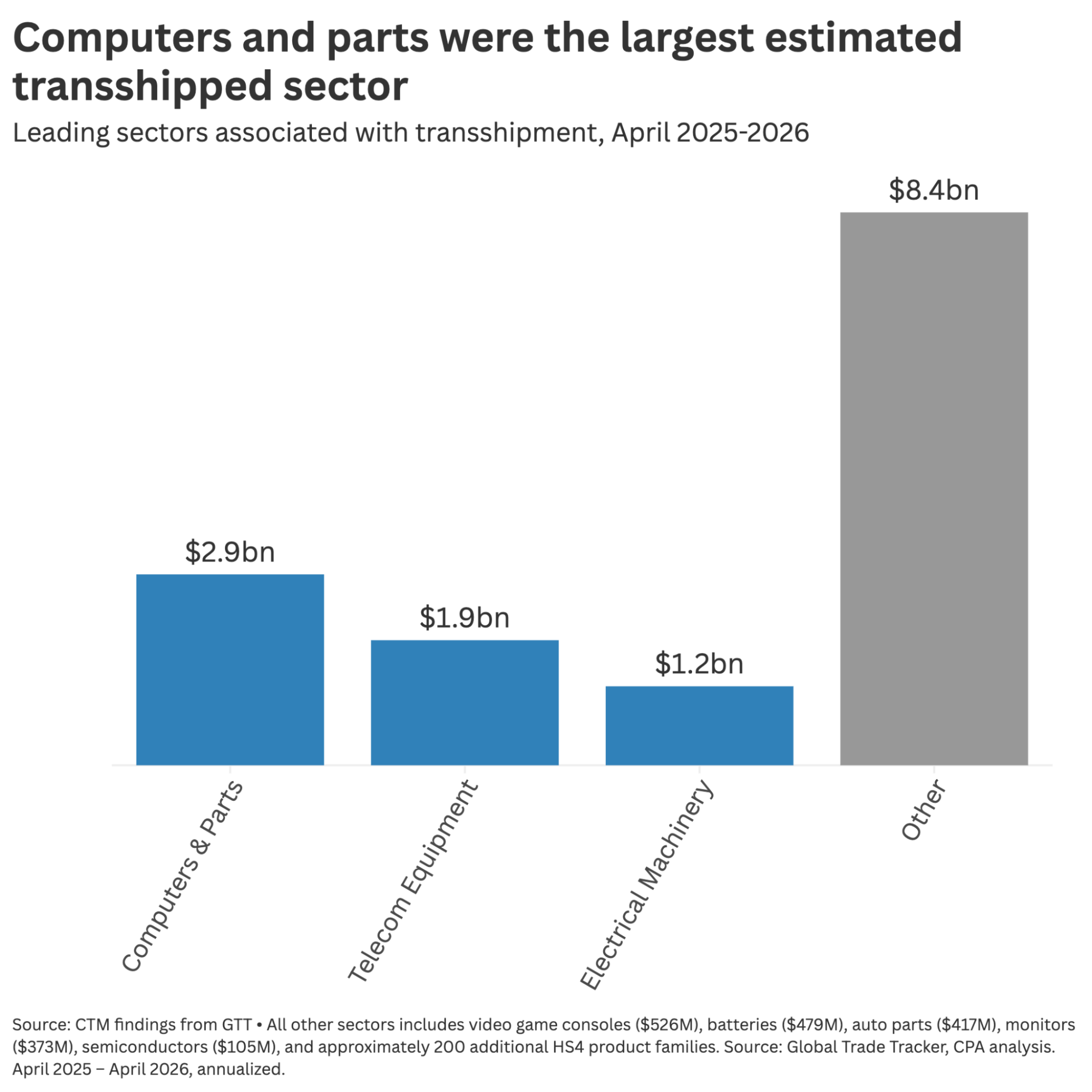

Sectors Most Exposed to Transshipment

FIGURE 5

Electronics leads by a wide margin. Computers and computing parts account for $3 billion in transshipment exposure, telecommunications equipment for $2 billion, and electrical machinery for $1 billion (Figure 5). Together, these three categories represent 41% of the total and flow overwhelmingly through ASEAN.

The concentration is consistent with economic logic. These product categories have the highest unit values, the most complex multi-country supply chains, and the greatest opportunity to exploit the gap between Chinese and ASEAN tariff rates. A laptop assembled in Vietnam from Chinese components enters the United States at a 10% effective rate rather than 38%. On a $3 billion trade flow, that gap translates directly into foregone customs revenue.

Further down the list, the profile shifts from electronics toward strategic industrial goods. Batteries registered $479 million, relevant to the parallel debate over Chinese EV battery supply chains and the 45X production tax credit. Auto parts through Mexico alone added $45 million, reinforcing the case for tightening rules of origin in the July 2026 USMCA renegotiation.

Semiconductors and integrated circuits registered $105 million, a modest figure but one that warrants attention given the strategic sensitivity of the product category and the public investment committed through the CHIPS Act. If Chinese-origin chips are entering U.S. supply chains through third-country relabeling, the transshipment undermines the objectives of both the tariff regime and the industrial policy program.

The long tail matters as much as the headline sectors. The “Other” category accounts for $6 billion, or 44% of the total, spread across hundreds of HS4 families. CBP can target the top three sectors and cover 41% of the problem. Covering the rest requires product-level screening at scale.

Two emerging patterns deserve monitoring. The rapid growth in battery transshipment coincides with the expiration debate over the 45X credit. If Congress allows it to lapse, the incentive for Chinese battery manufacturers to route production through ASEAN and Mexico will increase. The product-level overlap between transshipment exposure and USMCA origin rules creates a rare alignment between enforcement priorities and the negotiating calendar.

The Cost of Transshipment

FIGURE 6

Volume alone does not determine which corridors are most costly. The tariff differential matters as much. Effective rates in Mexico and Canada sit more than 30 percentage points below China’s, the widest gap of any corridor. Their combined exposure is a relatively modest $724 million, but every dollar rerouted through USMCA avoids more duty than through nearly any other channel.

India’s revenue loss is moderate relative to its transshipment volume because its own effective rate (12%) narrows the arbitrage window. EU member states, with a collective effective rate of 5%, present a wider gap and account for a disproportionate share of per-dollar revenue loss despite lower transshipment intensity.

This finding is directly relevant to the July 2026 USMCA renegotiation. If Chinese goods are entering the U.S. market through Mexican intermediaries under USMCA preferences with minimal transformation, the rules of origin need tightening. The CTM’s product-level data can identify which HS6 codes are driving the exposure.

The $4 billion is a conservative estimate for two reasons. First, the revenue calculation applies partner-level average effective rates rather than product-specific rates; for corridors where transshipment is concentrated in high-tariff categories, the actual per-dollar loss likely exceeds the average. Second, the analysis does not capture revenue lost through direct customs fraud, including undervaluation, misclassification, and shell company schemes. In 2025, the gap between what China reported exporting to the United States and what U.S. Customs recorded as arriving reached a record $112 billion, suggesting that direct fraud losses may rival or exceed transshipment losses.

Policy Recommendations

The CTM’s findings point to five areas where targeted action would narrow the $70 billion gap. Three address transshipment enforcement; two address the structural leakage that accounts for the vast majority of foregone revenue.

1. Narrow product exclusions and sunset bonded warehouse deferrals

The $66 billion structural leakage is the largest source of foregone revenue and the most actionable. Product exclusions on electronic components, industrial inputs, and medical products account for a substantial share of the gap between the statutory and observed effective rate. Each exclusion was granted for a reason, typically to avoid disrupting domestic supply chains, but the cumulative effect has been to reduce the effective tariff rate by more than a third.

Congress and USTR should conduct a systematic review of all active exclusions, sunset those where domestic or allied-country alternatives now exist, and require annual reauthorization for those that remain. The review should prioritize exclusions in product categories where the CTM identifies significant transshipment exposure, as these categories represent both direct revenue loss (through the exclusion) and indirect revenue loss (through the transshipment corridor the exclusion helps sustain).

Bonded warehouse and foreign trade zone deferrals present a separate challenge. These provisions allow importers to defer duty assessment until goods are withdrawn for consumption, and a share of goods are re-exported without duties ever being paid. Requiring periodic reconciliation of bonded warehouse entries for Chinese-origin goods would close this gap without eliminating the programs’ trade facilitation benefits.

2. Tighten USMCA rules of origin ahead of the July 2026 renegotiation

The CTM identifies $724 million in transshipment exposure through Mexico and Canada, with the widest tariff gap of any corridor. If Chinese goods are entering the U.S. market under USMCA preferences after minimal transformation, the rules of origin need strengthening. Auto parts, electrical machinery, and computing components should be subject to enhanced origin verification in the renegotiated agreement.

3. Expand CBP enforcement in Southeast Asian corridors

ASEAN accounts for 61% of all transshipment exposure, concentrated in electronics flowing through Vietnam, Thailand, and Malaysia. CBP should increase targeting of high-risk HS6 codes, particularly in computers and parts ($2.9 billion), telecom equipment ($1.9 billion), and electrical machinery ($1.2 billion). Product-specific enforcement is more efficient than blanket measures and avoids disrupting legitimate trade.

4. Require quarterly reporting on the statutory-observed rate gap

The CTM reveals that the U.S. collected barely three-fifths of its prescribed tariff revenue on Chinese imports in the year after Liberation Day — a gap that has widened as statutory rates have risen while exclusions and deferrals hold the effective rate down. This gap has received far less policy attention than transshipment, despite being fifteen times larger.

USITC or CBP should publish quarterly data on the effective vs. statutory rate, broken down by product category and exclusion type, so that policymakers can track whether the gap is widening or narrowing.

The reporting framework should also track the bilateral customs data discrepancy between Chinese export declarations and U.S. import records, which reached $112 billion in 2025. Publishing this figure alongside the rate gap would give policymakers a more complete picture, distinguishing between revenue lost through policy design (exclusions) and revenue lost through enforcement failure (fraud and transshipment).

5. Investigate transshipment in strategically sensitive product categories

South Korea and Taiwan registered transshipment exposure concentrated in semiconductor-adjacent products: computer parts, monitor components, and electronics assemblies. These volumes are small in dollar terms but significant given the strategic sensitivity of the products. The Department of Commerce should assess whether transshipment in these categories undermines existing export controls and the CHIPS Act investment program.

Conclusion

The CTM identifies statistical relationships between trade flows, suggesting instances of transshipment. When Chinese exports to a partner surge in the same HS6 codes where that partner’s exports to the United States also surge, the pattern is consistent with rerouting. It does not, by itself, prove that specific goods were relabeled or minimally processed. Legitimate capacity shifts, inventory restocking, and changing sourcing decisions can produce similar signatures in the data.

That distinction is the point. The CTM is a screening tool designed to direct enforcement attention; it is not a forensic audit. Policymakers should read its findings the way an epidemiologist reads a cluster map: the data identifies where to investigate, not what the investigation will find. The $14.4 billion in transshipment exposure marks the corridors and product categories where CBP’s limited enforcement resources are most likely to yield results. The $66 billion in structural leakage identifies the policy design choices that are eroding the effective rate from within.

Used this way, the CTM offers a quarterly diagnostic. By tracking whether the statutory-observed rate gap widens or narrows, and whether transshipment intensity shifts across corridors as enforcement tightens, policymakers can assess whether collection is keeping pace with the incentives the tariff regime creates. The $70 billion gap is the product of specific, reversible policy choices. Closing it requires collecting the tariffs already on the books.

The tariff regime is aggressive on paper and permissive in practice. The CTM will track whether that changes.

FOOTNOTES

The statutory rate is the tariff the schedule prescribes — the combined rate a Chinese import would face if every layer of duties applied in full. The effective rate is what the Treasury actually collects, calculated as total duties collected divided by the customs value of imports. The gap between the two reflects exclusions, bonded warehouse deferrals, foreign trade zone provisions, and other policy carve-outs that reduce the rate on qualifying goods.

In August 2023, Commerce found that solar cell imports from Cambodia, Malaysia, Thailand, and Vietnam were circumventing AD/CVD orders on Chinese solar products. In July 2024, Commerce ruled that wooden cabinets completed in Malaysia or Vietnam using Chinese components fall within the scope of AD/CVD orders on Chinese cabinets. See 88 Fed. Reg. 57,412; 89 Fed. Reg. 57,845.

Transshipment through third countries, which the CTM estimates at $14.4 billion during April 2025 – April 2026, is one source of revenue leakage. Direct customs fraud at the port of entry — including undervaluation, misclassification, and shell company schemes — represents another. In 2025, the gap between what China reported exporting to the United States and what U.S. Customs recorded as arriving reached a record $112 billion.

As used in this report, transshipment refers to goods that are manufactured in China but enter the United States under a third-country origin label, typically after undergoing minimal or superficial processing abroad sufficient to change their customs classification. This is distinct from logistics transshipment, where Chinese-origin goods transit a port hub like Singapore but retain their Chinese-origin declaration upon entry into the United States — a common practice that is already captured correctly in U.S. trade data.

Africa coverage includes South Africa, Nigeria, Egypt, Kenya, Ethiopia, Ghana, Tanzania, and Morocco. The GCC includes Saudi Arabia, the UAE, Kuwait, Qatar, Bahrain, and Oman. South America includes Argentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Guyana, Paraguay, Peru, Uruguay, and Venezuela. “Other Asia” includes Bangladesh, Pakistan, Sri Lanka, and Mongolia. Central America includes Belize, Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua, and Panama.

REFERENCES

ASEAN-Japan Centre, “Global Value Chains in ASEAN: Electronics,” Paper 13, March 2021. https://www.asean.or.jp/main-site/wp-content/uploads/2024/03/GVCs_Electronics_Paper-13_full_web.pdf

Barata da Rocha, Madalena, Nicolas Boivin, and Niclas Poitiers, “The Economic Impact of Trump’s Tariffs on Europe: An Initial Assessment,” Bruegel Analysis 16/2025, April 17, 2025. https://www.bruegel.org/sites/default/files/2026-04/the-economic-impact-of-trump%E2%80%99s-tariffs-on-europe%3A-an-initial-assessment-10843.pdf

Bloomberg, “China’s $112 Billion Cargo Gap Shows Record US Tariff Evasion,” February 24, 2026. https://www.bloomberg.com/news/features/2026-02-24/china-s-112-billion-cargo-gap-shows-record-us-tariff-evasion

Flach, Lisandra, Hannah Hildenbrand, and Feodora Teti, “The Regional Comprehensive Economic Partnership Agreement and Its Expected Effects on World Trade,” Intereconomics, Vol. 56, No. 2, pp. 92-98, 2021. https://www.intereconomics.eu/contents/year/2021/number/2/article/the-regional-comprehensive-economic-partnership-agreement-and-its-expected-effects-on-world-trade.html

Hiratuka, Celio, “Why Brazil Sought Chinese Investments to Diversify Its Manufacturing Economy,” Carnegie Endowment for International Peace, October 18, 2022. https://carnegieendowment.org/research/2022/10/why-brazil-sought-chinese-investments-to-diversify-its-manufacturing-economy

MERICS, “Mapping and Recalibrating: Europe’s Economic Interdependence with China,” China Monitor, November 2020. https://blog.merics.org/sites/default/files/2020-11/Merics%20ChinaMonitor_Mapping%20and%20recalibrating%20%281%29.pdf

Meltzer, Joshua P., “Is China Circumventing US Tariffs via Mexico and Canada?” Brookings Institution, September 23, 2025. https://www.brookings.edu/articles/is-china-circumventing-us-tariffs-via-mexico-and-canada/

Meyer, Armand, and Agatha Kratz, “China’s Manufacturing FDI in ASEAN Grew Rapidly, But Faces Tariff Headwinds,” Rhodium Group, April 24, 2025. https://rhg.com/research/chinas-manufacturing-fdi-in-asean-grew-rapidly-but-faces-tariff-headwinds/

Meyer, Armand, Danielle Goh, and Thilo Hanemann, “A Closing Back Door? China’s Evolving FDI Presence in Mexico,” Rhodium Group China Cross-Border Monitor, October 10, 2024. https://cbm.rhg.com/sites/default/files/2025-04/china-s-evolving-fdi-presence-in-mexico.pdf

New York Times, “Tariffs, Southeast Asia, and Transshipments,” August 7, 2025. https://www.nytimes.com/2025/08/07/business/economy/tariffs-southeast-asia-transshipments.html

Ports of Rotterdam and Antwerp-Bruges, “Value Creation for Europe,” February 2025. https://www.portofrotterdam.com/sites/default/files/2025-02/Value%20creation%20for%20Europe%20%28Ports%20of%20Rotterdam%20and%20Antwerp-Bruges%29.pdf

Spital, Tajda, “Global Trade Redirection: Tracking the Role of Trade Diversion from US Tariffs in Chinese Export Developments,” European Central Bank Economic Bulletin, Issue 1/2026, February 18, 2026. https://www.ecb.europa.eu/press/economic-bulletin/focus/2026/html/ecb.ebbox202601_01~fde39c8d00.en.html

U.S. Department of Commerce, “Antidumping and Countervailing Duty Orders on Crystalline Silicon Photovoltaic Cells, Whether or Not Assembled Into Modules, From the People’s Republic of China: Final Affirmative Determinations of Circumvention,” 88 Fed. Reg. 57,412, August 23, 2023. https://www.federalregister.gov/documents/2023/08/23/2023-18161/antidumping-and-countervailing-duty-orders-on-crystalline-silicon-photovoltaic-cells-whether-or-not

U.S. Department of Commerce, “Wooden Cabinets and Vanities and Components Thereof From the People’s Republic of China: Final Scope Determination,” 89 Fed. Reg. 57,845, July 17, 2024. https://www.federalregister.gov/documents/2024/07/17/2024-15681/wooden-cabinets-and-vanities-and-components-thereof-from-the-peoples-republic-of-china-final-scope

U.S.-China Economic and Security Review Commission, 2025 Annual Report to Congress, November 2025. https://www.uscc.gov/sites/default/files/2025-11/2025_Annual_Report_to_Congress.pdf

U.S. Government Accountability Office, “Antidumping and Countervailing Duties: Management Enhancements Needed to Improve Efforts to Detect and Deter Duty Evasion,” GAO-12-551, May 17, 2012. https://www.gao.gov/products/gao-12-551

Vietnam Briefing, “Vietnam’s Electronics Industry 2026: A Guide to Emerging Opportunities,” April 30, 2026. https://www.vietnam-briefing.com/news/vietnams-electronics-industry-guide-emerging-opportunties.html/

Wall Street Journal, “China, Africa, and Tariffs,” 2025. https://www.wsj.com/world/africa/china-africa-tariffs-664f62eb

Womble Bond Dickinson, “Buying American: Country of Origin Requirements in US Government Contracts,” April 2020. https://www.womblebonddickinson.com/sites/default/files/2020-04/Buying_American_Country_of_Origin_Requirements_in_US_Government_Contracts.pdf