War in Ukraine Highlights Critical US Dependencies on Russia-China Axis

By Jeff Ferry and Amanda Mayoral

Summary Points

- The Russian invasion of Ukraine reveals the weakness of US industrial strategy and our over-reliance on imports in manufactured goods and raw materials.

- The US is import-dependent in many industries critical to US national security.

- A weak manufacturing base in critical industries leaves the U.S. vulnerable to shortages, price hikes, and market disruptions. It also weakens our negotiating position because adversaries are well aware of these dependencies.

- A strong manufacturing base strengthens our hand when confronting global threats because we are able to ramp up domestic production when necessary.

Industrial strategy is a critical component of national security policy. Despite this reality, US trade and industrial policies have overlooked industrial strategy in favor of globalization policies of free trade and widespread offshoring. This has hollowed out the U.S. manufacturing base over the past several decades. Now facing multiple global threats, the U.S. has a weak hand to play. Russia is challenging peace in Europe. China is increasing its influence in Asia and beyond. Both nations are coming together, as seen in the February 4th strategic agreement, to oppose the U.S., and what they called its “hegemony” and “standards of democracy.” Russia voiced support in that agreement for China’s claim to Taiwan.

Should the crisis intensify, the U.S. would be unable to mobilize resources in critical areas because it is overly dependent on foreign imports, especially from China. The Covid-19 crisis revealed painful shortages in the U.S. supply chain, particularly for drugs and medical equipment. Supply chain snafus over the past year have exposed shortages and over-dependence in a wide range of industrial goods. The current crisis leaves the U.S. with less freedom to maneuver than at any time since 1945.

Critical Manufacturing Industries for U.S. National Security

During the COVID-19 pandemic, the US government identified several industrial sectors critical to national security. The list of sectors is reported on the Cybersecurity and Infrastructure Security Agency (CISA) website. Four sectors—metals, machinery, electrical equipment, and transportation equipment— were identified as areas that are critical for our military and for the functioning of our day-to-day civilian economy. Other sectors that play an important role include computers/electronics, chemical production, the energy sector, and mining of minerals such as rare earths.

Metals include iron, steel, aluminum, copper, and others that are used to build vital U.S. infrastructure such as roads and the nation’s electric grid. Metals are also used in military equipment and thousands of consumer products.

Machinery includes machine tools, engines, pumps, and other equipment largely used in the manufacturing sector to produce finished products.

Electrical equipment includes batteries, electrical components, lighting equipment, household appliances and other parts with uses in consumer products and industrial applications.

Transportation equipment includes cars, trucks, airplanes, ships, and railway equipment which are all vital for the consumer economy and for military forces.

Computers/electronics include laptop computers, smartphones, the equipment that makes the Internet run, as well as the sophisticated defense electronics that power modern military equipment such as fighter jets, submarines, and tanks.

Chemical products are vital for many manufacturing production processes, including industrial gases, plastics, and other chemicals. Pharmaceuticals, vaccines, and other medicines are also included in the chemical sector.

Energy sector includes the infrastructure that generates and transmits electricity nationwide and the equipment used to create energy, such as oil and gas equipment and renewable energy equipment.

Mining sector includes the mining of metals like iron, copper, and rare earths as well as nonmetals such as gravel, used to make cement.

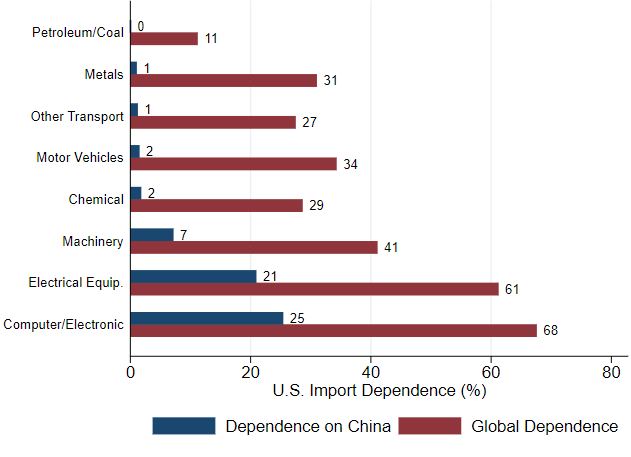

In all these sectors, the U.S. is largely dependent on imports. Figure 1 charts the level of import dependence with data from the CPA Reshoring Index. The red bars show the import dependence of each sector. It is highest for computers and electronics, where 68% of U.S. consumption of these products comes from imports. (This data is from government figures for 2019, to show normal U.S. pre-pandemic production and consumption.) In electrical equipment, we also rely on imports for a majority of our consumption of these vital products. In motor vehicles, chemicals, and machinery, we rely on imports for over a third of our normal consumption.

In World War II, the U.S. mounted a huge, rapid escalation of production of all military equipment, led largely by executives from the U.S. auto industry. Today we would be unable to execute such an operation, because production of today’s military (and civilian) equipment depends on electronics and machinery, so much of which is imported. The Russia-China alliance makes matters worse. The blue bars in Figure 1 show U.S. dependence on Chinese imports. In key sectors like computers, electrical, and machinery, our imports from China make up a large share of our total consumption. In any confrontation with China (for example, over a Chinese attack on Taiwan), U.S. imports would become unreliable and might stop altogether.

U.S. dependence is in reality far worse than depicted in Figure 1, which shows complete industrial sectors as classified by the U.S. Bureau of Economic Analysis. Within each sector, there are individual products, components, or materials, where our dependence is far greater. For example, rare earth metals are used in vital electrical components that go into computers, fighter jets, and hundreds of other products. China produces 60% of the world’s rare earths and refines even more of them. U.S. mining of rare earths has restarted in Mountain Pass, California, but the mineral compounds are sent to China for refining. So our ability to become once again the “arsenal of democracy” is hamstrung by dependence on the very nations likely to become our opponents.

This lack of broad-based domestic production also hampers our sanctions efforts against Russia, which are pretty weak to begin with. For example, the Biden administration is imposing a ban on the export of microchips to Russia. But Russia imports a tiny amount of chips. Chips are only of use inside electronic devices. As the world’s largest manufacturing nation, China plays an outsize role in the production and export of most electronic devices, including computers, engines, pumps, etc. Like the U.S., Russia gets most of its computers from China. Despite any Russia sanctions, the U.S. designed chips that are the brains of those computers are still going to China and with the new closer Russia-China relationship, China will make sure Putin does not lack for computers and related electronics.

Figure 1: U.S. Import Dependence in Critical Industries

Source: CPA Reshoring Index, 2021

Russia’s Influence in The World Economy

As the U.S. considers sanctions against Russia, it’s important to understand the scale of Russia’s influence in the world economy and how we can impose penalties on Putin’s Russia while managing the damage to the U.S. and rest of the world. As a $1.7 trillion economy, Russia’s global role is significant, but confined to a handful of strategic sectors. Russia’s efforts to modernize and industrialize since the collapse of the Soviet Union have mostly been unsuccessful. Instead, Russia remains a key producer and exporter of primary products.

Oil & Gas

Oil and gas are Russia’s best-known and most important exports. According to data from NSEnergyBusiness.com, in 2019 Russia was the world’s third-largest producer of oil, pumping 11.5 million barrels a day or 12% of global oil production. According to the BP Statistical Review of World Energy 2020, Russia was the world’s largest oil exporter, exporting 9.2 million barrels/day, slightly more than Saudi Arabia or the U.S. Russia’s economic clout stems from the fact that many nations are dependent on either Russian oil, or the global price of oil, both of which are heavily influenced by Russia’s production and exports. As the world’s leading oil exporter, oil prices are sensitive to changes in Russia’s production levels.

In natural gas, the story is similar. The U.S. is the world’s largest producer of natural gas, thanks to the fracking revolution of the last 20 years. But Russia is number two, producing 679 billion cubic meters, equivalent to 17% of global production. Russia has the world’s largest reserves of natural gas. In terms of exports of liquefied natural gas (LNG), which travels by ship, Russia ranked fourth in 2019, after Qatar, Australia, and the U.S. But Russia exports far more natural gas through pipelines, nearly all of it to Europe. In 2019, some 217.2 billion cubic meters of Russian gas was exported through pipelines. Russia’s political clout comes from the fact that some 37% of Europe’s natural gas comes from Russia. For Germany, Russian dependence is even higher. Europe has become increasingly dependent on natural gas, following European efforts to reduce emissions, such as Germany’s decision to restrict coal production and step away from nuclear power. This has made Europe more dependent on Russian natural gas.

With oil prices now topping $100 a barrel for the first time in years, Russia’s growing clout in this market is clear. As in any market, the solution in economic and geopolitical terms, is to have alternatives. Those alternative include U.S. fossil fuels as well as renewable sources of energy. China’s growing domination in renewable energy equipment (solar and wind) is another flashing red light for the coming geopolitical confrontations of the 21st century. It’s also clear that there is little wisdom in banning some forms of energy before alternatives are fully capable of fulfilling the gap. Or as one wag on Twitter said, Germany should stop allowing its energy policies to be dictated by a Swedish 18-year-old in braids.

Russia has used this dependence to increase Russia’s influence in Europe, for example by bringing former German chancellor Gerhard Schroeder onto the board of Russian gas giant Gazprom. The U.S. is increasing its shipments of LNG gas to Europe, with the potential to reduce European dependence on Russia and (perhaps) enable European leaders to show a little more backbone in standing up to Putin. But all such moves are mired in domestic political debates about fossil fuels. Putin has cleverly exploited such confusion to make Russia’s supplies a more powerful weapon in global geo-politics. The alliance with China further increases Russia’s and China’s influence in the critical global energy market.

Minerals

Russia is also a key producer of several strategic minerals. Russia and South Africa are the two leading sources for palladium, each producing about one third of the global total. Palladium is used in automotive catalytic converters and in some widely used electronic components like capacitors. The price of palladium, now around $2300 an ounce, has tripled since 2017, largely due to increased use in the automotive sector. According to the USGS, there are domestic resources of palladium (USGS, 2020). However, ramping up U.S. mining capability is always challenging, due to long and uncertain U.S. approval processes.

China and Russia together account for 80% of the world’s supply of vanadium, another little-known metal that is crucial in several industrial products. Vanadium is used as an alloy in turbine blades in jet engines and power transmission equipment. It also has uses in electronics and chemical refining.

Antimony is another metal where China and Russia are the world’s leading suppliers. Antimony is used in ammunition, flame retardants, and ceramics. The U.S. has little domestic capability to mine antimony and is highly dependent on China for current supplies. According to the USGS, China accounts for some 77% of global production, with Russia in second at 6.9%.

Another little-known resource is neon, an inert gas widely used in semiconductor manufacturing. According to technology market analyst firm TrendForce, Ukraine supplies 70% of the world’s consumption of neon. The current war threatens supplies of neon, and if Ukraine ends up as a puppet state of Russia, this further strengthens the hold of the Russia-China axis over vital supplies in the technology supply chain.

China is already the leading global supplier of many minerals, such as the rare earths cited above. The China-Russia alliance will strengthen China’s hand in the rising global confrontation between the U.S. and China. In addition to the domestic mineral resources within the vast land mass that stretches from eastern Europe to the Pacific coast, Russian companies like Norilsk Nickel and China’s large number of mining companies control other mineral resources elsewhere, such as the critical cobalt supplies in the Congo, largely mined by Chinese companies.

Conclusion

Russia is inflicting war not just on the Ukraine, but also on European peace, and on global democracy. This war, combined with the emerging China-Russia axis, has serious implications for the U.S. The decline of the U.S. industrial base puts us at a huge disadvantage in protecting our own country and providing global leadership at times of crisis. Following Russia’s invasion of the Ukraine and the Russia-China alliance, the need to reshore critical industries is more imperative than ever.

References

Andrew Fawthrop, The top ten largest oil-producing countries in the world, NS Energy, 2020.

Andrew Fawthrop, Profiling the top six natural gas producing countries in the world, NS Energy, 2021.

Statistical Review of World Energy, BP, 2020.

Trendforce, Ukrainian-Russian Conflict Affects Semiconductor Gas Supply and May Cause Rise in Chip Production Costs, Says TrendForce, Feb. 15, 2022.

U.S. Geological Survey, Mineral Commodity Summaries 2022.