Ask someone walking down Main Street USA if they think a strong dollar is important and they will say yes. They think a strong dollar allows them to buy more things. They are right, of course. It means American companies can buy more things overseas and sell it to consumers cheaply.

Ask someone on Wall Street the same question and they will undoubtedly say yes. A strong dollar means more demand for dollar assets, meaning a bigger market for the financial products and services that they sell.

But if you ask retired World Bank economist John R. Hansen, he will tell you that the strong dollar has inflicted huge damage on U.S. businesses, farmers, and workers, by making U.S. goods uncompetitive in world markets and making imports from China, Japan, Germany, and elsewhere too competitive here at home.

According to CPA economists, the overvalued dollar has cost the U.S. on the order of five million jobs. The damage gets worse as the dollar continues to climb in the tense atmosphere following Russia’s war in Ukraine.

To Wall Street, however, a strong dollar also means foreigners have high demand for Treasury bonds, which keeps interest rates low and allows big investment banks to buy stocks and bonds on margin. Margin is debt, and some firms borrow up to five times the amount of what they are purchasing. In other words, take out a loan for $5,000, but put in only $1,000 of your own money to buy Tesla stocks. That’s five times margin.

In February, FINRA reported that clients in their members’ investment firms had over $835 billion in open margin accounts ready to be deployed or already deployed.

That number does not include proprietary trading accounts held by big banks like Goldman Sachs, nor does it count hedge funds. This number, which is equal to the entirety of the Saudi Arabian GDP for 2020, is made possible thanks to the low-interest rates that come with a strong dollar. These accounts also accumulate interest and serve as a good example of why Wall Street backs strong dollar policies.

Washington, too, likes a strong dollar, but for different reasons.

For some, a strong currency is a symbol of economic strength. A weak currency is something banana republics suffer.

Others, with a more sophisticated view of markets, understand that a strong dollar makes it easier to maintain low-interest rates. Low-interest rates mostly benefit large borrowers. If low-interest rates lead to higher housing costs, many people end up being priced out of the market altogether.

Worth noting here is that many of these people – from Wall Street to Washington — will say the Chinese yuan is too weak. It trades at around six to one against the dollar.

Yet, despite dollars going farther in China than here – making it cheaper for U.S. multinational companies in terms of every imaginable overhead cost, from labor to taxes – China continues to gain on the U.S. economy.

Is the Chinese economy a powerhouse or is it being left behind, making nothing but Happy Meal toys and cheap Christmas ornaments? Most people will unanimously agree that China is an economic powerhouse. Your kids are on TikTok. Not the European equivalent, if there even is one. The new Fast & Furious film opened in China first, not Mexico, not France, and definitely not here.

“If you talk to members of congress, and the general public, they seem to be relatively unaware of the severity of the overvalued currency that we have. It is really eating our lunch,” said Hansen. “There seems to be a love of the strong dollar, and the idea that it makes America strong. We know that China is strong in terms of all the dollars it accumulates from our economy, yet China has a weak currency. So how can a weak currency make China strong, and a strong dollar makes us weak?”

Hansen presented at last week’s annual CPA conference in Washington D.C.

Hansen has been beating the drum on this issue since at least 2015 and is widely published on the subject.

The U.S. has been living with “the fat dollar monster” – as he referred to it last week at the conference — for about 50 years. It got really beefy in the late 1970s with the petrodollar.

The U.S. has been living with “the fat dollar monster” – as he referred to it last week at the conference — for about 50 years. It got really beefy in the late 1970s with the petrodollar.

Manufacturing went south – and east – ever since. And American standards of living largely flatlined, with wages barely able to keep up with inflation.

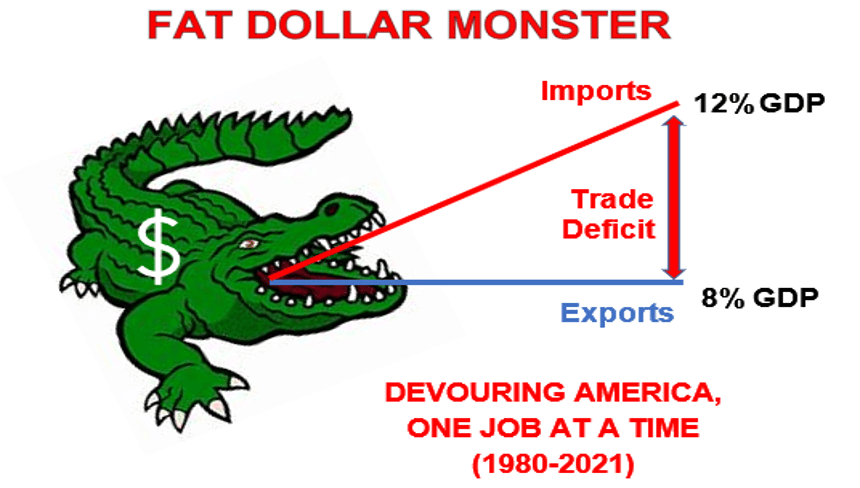

Exports between 1980 and 2021 have remained at around 8% of U.S. GDP, with no noticeable upside despite investments and improved productivity due to new technology. Imports went from 8% of GDP in 1980 to 12% over the same period.

Last year, the U.S. recorded a massive, record-breaking, $1.09 trillion goods deficit. For the first two months of this year, the goods deficit was over $80 billion, breaking record after record, in spite of tariffs on Chinese goods and quotas on European and Japanese steel. That is because for the companies who make and sell these goods, it is cheaper to do so overseas thanks to the strong purchasing power of the U.S. dollar. Twenty-five percent tariffs are not enough, especially when compared to currencies like the Mexican peso, and the Vietnamese dong.

The dollar is overvalued by an estimated 20%, Hansen said, citing research from both CPA and the Peterson Institute for International Economics.

The Chinese yuan is undervalued by about the same amount. That acts as a tax on every U.S. product sold overseas – something members of Congress continue to speak about during hearings in relation to export markets they are all trying to open up to American-made goods. The problem is that importers are going to have to pay 20% more for those goods.

The Chinese yuan is undervalued by about the same amount. That acts as a tax on every U.S. product sold overseas – something members of Congress continue to speak about during hearings in relation to export markets they are all trying to open up to American-made goods. The problem is that importers are going to have to pay 20% more for those goods.

“The overvalued dollar makes things manufactured abroad artificially cheap. Is that what we want? I don’t think so,” Hansen said.

Why is the dollar overvalued?

In layman’s terms, it is because the U.S. is the world’s largest and most liquid securities market. Portfolio investments from around the world are parked in U.S. mutual funds, private accounts, and hedge funds.

The dollar is used by the world. If China is buying Brazilian soybeans, they are transacting in dollars.

Emerging markets like China and Brazil all have foreign currency reserves that they maintain, most of them in dollars. China has over $2.5 trillion in its reserves in U.S. securities – either in money market accounts, U.S. Treasury bills, and bonds.

Are cheap imports great?

They allow us to consume more, but a better job market, one not dependent on employment in the gig economy or at the Dollar store, would make up for higher-priced goods.

Hansen said Washington policymakers need to look at the costs that lie behind the imports, including the economic and social costs of lost blue-collar jobs.

“If imports are underpriced, guess what happens? Unless the price difference is small, then people will buy foreign goods instead of American goods. And when you don’t buy American goods, companies have no interest in producing in America and our economy suffers,” Hansen said.

“The money Americans earn from their jobs ends up getting transferred – spent – abroad and then capacity utilization drops off. You’ve seen that in the steel industry,” he said.

What does that look like? If a company is built to make 100 pounds of widgets a month, but only makes 60 pounds because it’s too expensive to make 100 pounds, then the money that the company spent on machinery and labor to make 100 pounds is going to waste. Layoffs occur. Worse yet, companies fold.

“Who is going to invest if someone can undersell you all the time? The strong dollar is a trap,” Hansen said.

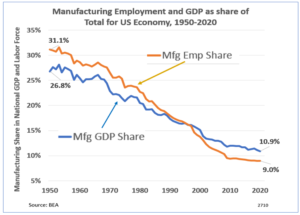

U.S. manufacturing employment and share of GDP have both plunged from being about a third of GDP to 10% currently. Nearly all of those manufacturing gains were sent to Mexico and China, with some going to Europe. The manufacturing jobs were replaced by service jobs or nothing at all.

“My wife and I lived in North Carolina for 15 years before moving back to DC. Driving through the state you will see these communities that have been decimated. It’s grinding poverty,” he said. “We shouldn’t have that here in the U.S., but we do. We are very poor, internationally speaking, in terms of intergenerational mobility and now you are seeing that within entire communities, like in North Carolina, where textile and furniture manufacturers left. You sometimes have a community with two or three manufacturing jobs in town and when one of them is offshored, it’s a disaster. That is why income inequality has exploded in the U.S.”

Back in the early 1900s, we had the robber barons, famous for building mansions in New York, and summer home villas in Newport, RI.

Back in the early 1900s, we had the robber barons, famous for building mansions in New York, and summer home villas in Newport, RI.

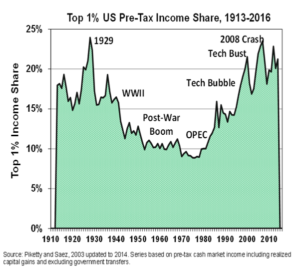

By World War II, income inequality declined as women entered the workforce. For about 20 years, up until the 1970s, the U.S. had its highest level of income. Wages rose. That changed with the petrodollar, leading to a stronger currency, and then rose again with the tech bubble in the 90s which led to fast-rising income inequality. Today, income inequality is approaching robber baron levels again.

Thanks to all the capital flowing into the U.S., not to build Toyota factories per se, but primarily to buy stocks and bonds, the U.S. now owes more to the world than the world owes the U.S. in terms of debt. That was not always the case. A strong dollar makes it so.

“We need to move to the dollar towards a competitive exchange rate,” Hansen said. “Two options are on the table, with one being a small tax on the money that comes in via investing into the securities market. That will slow the inflow. This way you are charging investors who are making the dollar unreasonably strong,” he said about a market access charge.

In March, the International Monetary Fund said that such access charges were okay so long as the market knew in advance and such moves were not done in the middle of an economic crisis, thus spooking markets.

“We have to fix this fat overpriced dollar,” Hansen said. “If we do, then we will have a balanced, slim, and trim currency that works for America.”