Key Points

- We find that further decoupling from China would grow the U.S. economy and result in higher incomes and more jobs for Americans and the rebuilding of many critical manufacturing sectors.

- The removal of MFN (most favored nation) status for China would increase the tariff rate on imports from China from the current Column 1 rate, which is often zero or near-zero, to the Column 2 rate, equivalent to an average tariff rate of 39.9%.

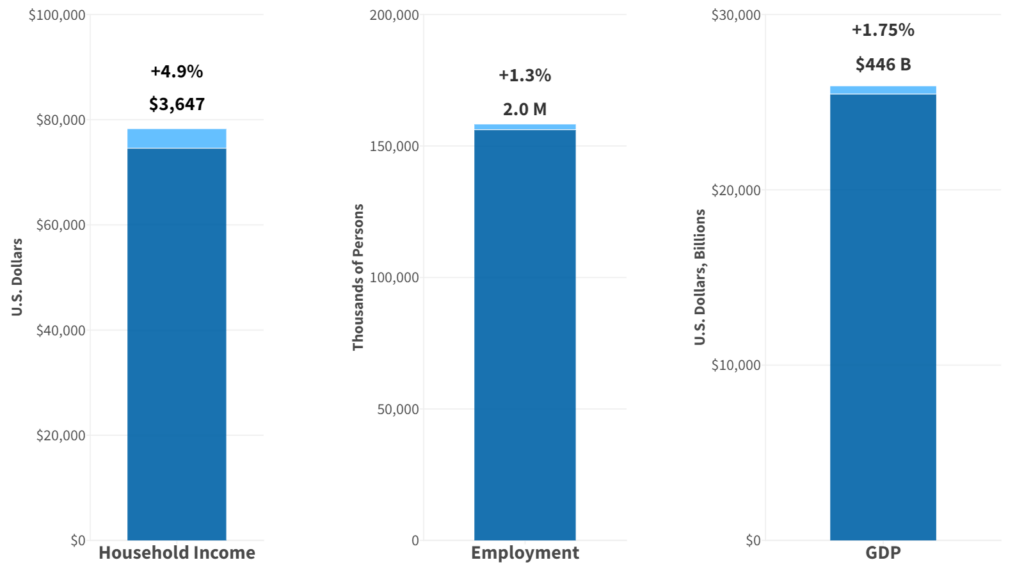

- The CPA Pro-Growth economic model finds that increasing tariffs on imports from China to Column 2 rates would result in 2 million new jobs and a $3,647 increase in real household incomes. Real GDP would grow by 1.75%.

- The CPA Pro-Growth model is based on real-world evidence of how tariffs expand economic output and allow firms to respond to the increase in domestic demand by increasing investment and creating new jobs.

Removing China’s MFN Status

In 2001, China was granted most favored nation status (MFN) which gave permanent preferential treatment to Chinese manufactured goods. This is also known as permanent normal trade relations (PNTR). Since 2001, the annual U.S. goods trade deficit with China has grown by $299.2 billion and amounts to a cumulative total of $6.1 trillion of goods deficits.

The trade deficit with China is by far the largest the U.S. runs with any country in the world. In 2022, the $382.9 billion trade deficit with China accounted for 32% of the $1.19 trillion total U.S. trade deficit. As our research shows, this has cost 3.4 million American manufacturing jobs since 2001. China has strategically undercut American firms with low-cost labor and government subsidy which has been the leading cause of the de-industrialization of the U.S. economy.

To analyze the impact the removal of China’s MFN status would have on the U.S. economy, we used our CPA Pro-Growth model to show the effects of imposing Column 2 tariffs on China, using the relevant Column 2 tariffs for each sector. Removing a country’s MFN status is not unprecedented as the U.S. removed Russia’s preferential trade status last year.

The Column 2 tariff rates that would apply to Chinese imports are listed in Table 1. Our model adjusts the tariff rate upward from the Column 1 rate which is often zero or a low single-digit rate. Of note, this simulation does not account for Section 301 tariffs or existing AD/CVD duties.

Table 1: Column 2 Tariff Rates, Weighted Averages for Major Sectors

| Sector | Column 2 Tariff Rate |

| Apparel | 72.1% |

| Textiles | 62.7% |

| Rubber & Plastics | 60.0% |

| Misc. Manufacturing | 50.2% |

| Mineral Products | 47.0% |

| Metal Products | 39.6% |

| Electrical Products | 37.0% |

| Leather | 35.9% |

| Machinery | 35.8% |

| Beverages | 35.5% |

| Computer & Electronics | 35.3% |

| Chemicals | 33.9% |

| Wood Products | 33.8% |

| Iron & Steel | 30.2% |

| Pharmaceuticals | 29.5% |

| Motor Vehicles | 24.1% |

| Non-Ferrous Metals | 24.0% |

| Paper Products | 23.8% |

| Food Products | 17.5% |

| Agriculture | 7.6% |

| Petroleum & Coal | 6.7% |

Source: U.S. International Trade Commission; CPA Calculations

Note: Column 2 rates are weighted by 2022 import value with China

CPA Pro-Growth Model

The CPA Pro-Growth model is a modified version of the standard Global Trade Analysis Project (GTAP) model often used to evaluate the economic impact of trade policy proposals. Our modifications account for how tariffs impact domestic production using real-world evidence. These modifications improve on the standard GTAP model by including how tariffs can increase domestic output and employment.

We introduce productivity elasticities into the model, allowing domestic producers to increase output and leverage the opportunity that a tariff provides. We also introduce factor elasticities, allowing firms to respond to an increase in demand by increasing their capital investment and increasing employment. Firms respond to the increased economic activity by expanding capital investment and hiring more workers, which further amplifies the positive effect of the tariffs.

China MFN Removal Would Create 2 Million Jobs, Grow U.S. Economy by 1.75%

Our model finds that increasing tariffs on imports from China to the Column 2 rate would increase real household incomes by $3,647, or 4.9%, and create 2 million new jobs. We also find that real GDP would increase by 1.75%. Figure 1 summarizes these results. China’s MFN status would create jobs and grow the U.S. economy.

Figure 1: Results of CPA Pro-Growth Model Simulation of China MFN Removal

Source: U.S. Census Bureau, Bureau of Labor Statistics, Bureau of Economic Analysis; CPA Calculations

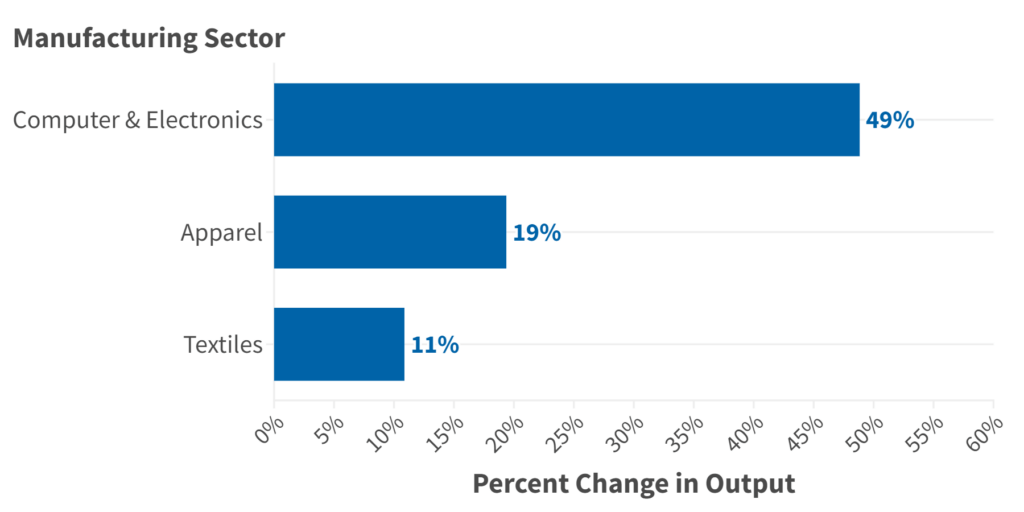

Increased tariffs on imports from China would also have a positive impact on U.S. manufacturing sectors. Our model finds China MFN removal would lead to reshoring, i.e. investment in manufacturing production that declined over the past two decades. Manufacturing output would increase by 6.1%.

The most powerfully impacted manufacturing sector is Computer & Electronics. Our model finds that tariffs at a Column 2 tariff rate of 35.3% would result in a 49% increase of production in this sector alone. Our Domestic Market Share Index (DMS) shows that in this sector, U.S. producers hold the second smallest market share of all 19 manufacturing sectors. The Computer & Electronics sector has lost about half of its domestic market share to foreign competitors over the past two decades, of which a substantial portion was gained by China.

The other top sectors with double-digit output gains are apparel (19%) and textiles (11%), both of which have been heavily offshored to China as well.

Figure 2: Top Manufacturing Increase by Sector from China MFN Removal

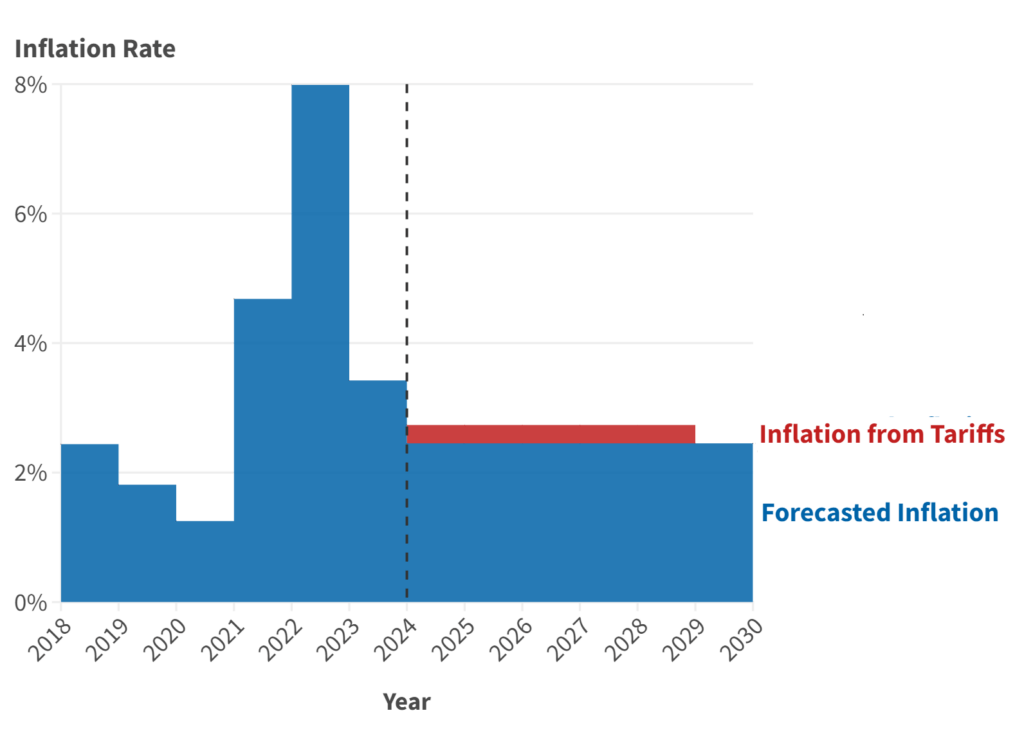

Increasing tariffs on imports from China at the Column 2 rates would result in a short-term increase in consumer prices. Our model finds consumer prices would rise by 1.7% over the entire transition period, or about 0.28% annually over an estimated six-year transition as Figure 3 shows. The graph also shows that the annual rate of inflation in 2019 after the imposition of Section 301 tariffs on many Chinese imports did not result in an increase on the prices of consumer goods.

Figure 3: Forecasted Rate of Temporary Inflation from China MFN Removal

Source: Federal Reserve Bank of St. Louis; CPA Calculations

The CPA Pro-Growth model shows that pursuing further decoupling from the Chinese economy by removing China’s MFN status would not harm the U.S. economy or American living standards. On the contrary, we find that further decoupling from China would grow the U.S. economy and result in higher incomes and more jobs for Americans and the rebuilding of many critical manufacturing sectors.