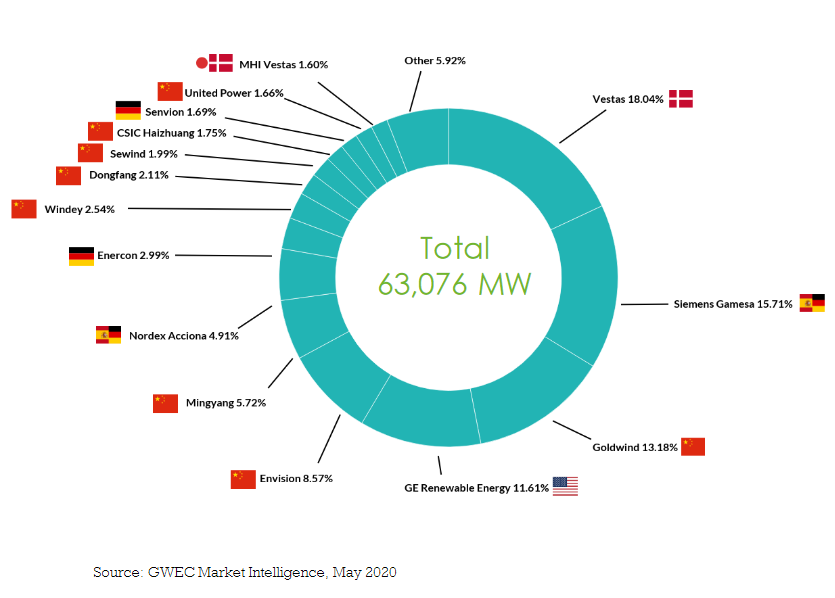

Ask a government official (or import lobbyist) whether a Buy American provision for solar and wind is a worthy cause and they’ll say “yes, but” – it’s more important to tackle climate change now and do it cheaply. That view instantly turns into sourcing bulk solar and EV battery materials from Asia. Wind turbines are next. Goldwind installed 48 wind turbines in the U.S. last year, versus 2 in 2019, according to the Global Wind Energy Council.

If you wonder why Beijing has jumped on the clean energy bandwagon, it’s not just because middle-class urbanites are sick of air pollution, though that is part of it. It is mostly driven by economics: China is a dominant force in every single clean energy supply chain in order to serve European and American climate change policies.

“We need to understand the real-person impact of these policies,” said Rep. Cathy Rodgers (R-WA-5) during a House Committee on Energy and Commerce hearing on May 3. “The drive to wind and solar…few are talking about how we are playing right into China’s strategic interests with these policies.”

Yet, the post-carbon world rages on. The Biden administration is following in the footsteps of our European allies in reducing the carbon footprint of the economy. It’s a worthy cause. And as President Biden says, “when I think of climate change, I think of jobs.”

“Dig, Baby, Dig”

Biden may be giving up on the old mantra of “drill, baby, drill” for hydrocarbons – as happened with fracking when he was vice president, but he will have to learn to embrace “dig, baby, dig” now.

The minerals going into EV motors, batteries, and wind turbines need to be mined. The U.S. clearly cannot mine what it does not have, but what it does have will require legislation to make sure it is happening domestically, at least in part, or risk going from fossil fuel energy security to clean energy dependence on raw materials sourced from elsewhere. Washington needs to think of the long game here. Developing mines can take 10 years or more.

“As the auto industry makes this shift, there is going to be risks and there are going to be opportunities,” said Rep. Debbie Dingell (D-MI-12) one of the lead sponsors of the CLEAN Future Act. “We have to get the policies right, or we leave this workforce behind.”

In a 287-page special report by the International Energy Agency (IEA) published this month, titled “The Role of Critical Minerals in Clean Energy Transitions”, the multilateral institution noted that a typical electric car requires six times the mineral inputs of a conventional car. A wind plant requires nine times more mineral resources than a gas-fired power plant.

Since 2010, the average amount of minerals needed for a new unit of power generation capacity has increased by 50% as the share of renewables has risen. Lithium, nickel, cobalt, manganese and graphite are crucial to battery performance, longevity, and energy density. Rare earth elements are essential for permanent magnets that are vital for wind turbines and EV motors, let alone navigational equipment on American fighter planes.

From the report:

“The shift to a clean energy system is set to drive a huge increase in the requirements for these minerals, meaning that the energy sector is emerging as a major force in mineral markets. Until the mid-2010s, the energy sector represented a small part of total demand for most minerals. However, as energy transitions gather pace, clean energy technologies are becoming the fastest-growing segment of demand.

In a scenario that meets the Paris Agreement goals, clean energy technologies’ share of total demand rises significantly over the next two decades to over 40% for copper and rare earth elements, 60-70% for nickel and cobalt, and almost 90% for lithium. EVs and battery storage have already displaced consumer electronics to become the largest consumer of lithium and are set to take over from stainless steel as the largest end user of nickel by 2040.”

Where Will These Minerals Come From?

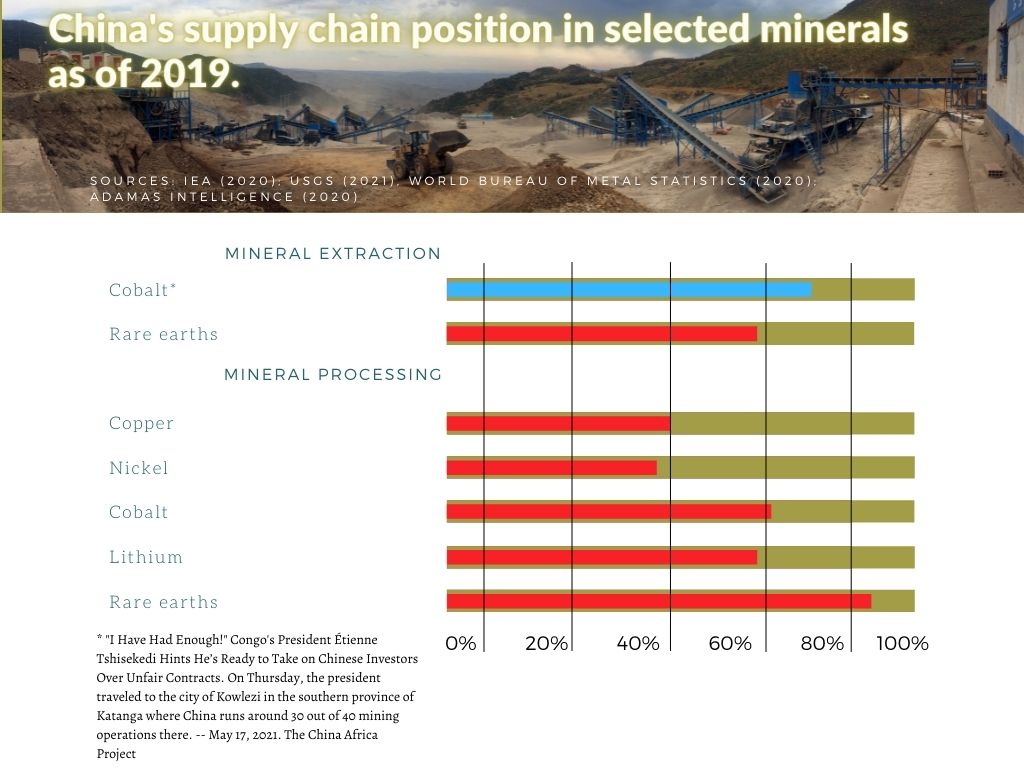

Production of many energy transition minerals is more concentrated than that of oil or natural gas. For lithium, cobalt, and rare earth elements, the world’s top three producing nations control well over three-quarters of global output. In some cases, a single country is responsible for around half of worldwide production.

The Democratic Republic of the Congo and China were responsible for some 70% and 60% of global production of cobalt and rare earth elements respectively in 2019. More than half of the Congo’s cobalt mines are being dug up by Chinese state-owned enterprises who ship the rocks to China to be processed.

In going green, it will be important to consider China’s footprint in this supply chain.

The level of concentration is even higher for processing operations, where China has a strong presence across the board. China’s share of refining is around 35% for nickel, 50-70% for lithium and cobalt, and nearly 90% for rare earth elements, the IEA report states.

Chinese companies have also made substantial investments in overseas assets in Australia, Chile, the Congo, and Indonesia. High levels of concentration, compounded by complex supply chains, increase the risks that could arise from physical disruption, trade restrictions, or geopolitical strife.

It also gives China an enormous amount of leverage. Imagine imposing sanctions on a Chinese company only to watch China hoard things like semiconductors, or reduce the export of rare earth materials needed to make an F16’s navigational equipment.

This also creates sources of concern for companies that produce solar panels, wind turbines, electric motors, and batteries using imported minerals. Their supply chains can quickly be affected by regulatory changes, trade restrictions, or political instability in a small number of countries. The Covid-19 pandemic already demonstrated the ripple effects that disruptions in one part of the supply chain can have on an industry.

The report highlighted the need for recycling battery waste, something CPA supports.

For bulk metals, recycling practices are already well established, but the IEA said that this is “not yet the case” for metals such as lithium and rare earth elements.

“Emerging waste streams from clean energy technologies can change this picture,” report authors wrote.

The number of spent EV batteries reaching the end of their first life is expected to surge after 2030, at a time when mineral demand is set to still be growing rapidly. IEA estimates that by 2040, recycled quantities of copper, lithium, nickel, and cobalt from spent batteries could reduce combined primary supply requirements for these minerals by around 10%.

Some members of Congress have addressed this issue of recycling.

IEA recommends funding R&D into new recycling technologies as a way to help companies that are devising ways to turn battery waste into materials that can be used to make new batteries.

In a May 6 article in The Korea Herald, American Manganese chief technology officer Zarko Meseldzija said battery manufacturing facilities are “producing maybe 10-20% of scraps from their process. That’s an opportunity to integrate a recycling process within that facility and recycle them directly back to high-quality materials that can be used for remanufacturing of batteries.”

Lithium-ion batteries, defective or not, contain cathodes that are made of expensive metals like nickel and cobalt and account for 25% of the cost of a whole battery.

“The scarcity narrative has led to a big push to get to these metals, as we are seeing in Nevada for lithium. There are over 13,000 claims for lithium there now,” said Dustin Mulvaney, a professor with the Department of Environmental Studies from San Jose State University. “Lithium-ion battery recycling will increase over time. For us to start moving in the direction of closing the loop on some of these metals, we have to start emphasizing more on waste. There needs to be more attention on that.”

Prices for certain minerals have risen strongly since the second half of 2020, with some reaching multi-year highs. This was due to expectations of strong future growth for alternative fuel sources, as well as China’s demand (and hoarding).

As a result of this price spike and demand outlook, the IEA said it sees “ample reasons to be vigilant about the ability of supply to meet demand – especially as many governments redouble efforts to accelerate energy transitions.”

Supply Chain Resilience is Economic Security

Analysis of historical episodes of tight mineral supply provides useful insight into the factors that could help to mitigate future risks from price spikes. Mitigating activity includes mineral substitution or innovation in supply and demand technologies.

From the 1960s until the late 1980s, the Mountain Pass mine in California was the largest source of rare earth oxides in the world. In 1992 China surpassed the United States as the world’s largest producer. Since then, China has dominated the global supply of rare earths and everything dug out of the ground at Mountain Pass gets shipped to China for processing.

From the report:

“After the Chinese export embargo in 2010, the US Department of Energy issued its first Critical Materials Strategy that year. The strategy identified 14 critical minerals, which were extended to 35 in later years. Since then, critical minerals have become a prominent feature in U.S. national security and defense strategies, highlighting the interdependence of economic security with national security.

The 2019 Federal Strategy to Ensure Secure and Reliable Supply of Critical Minerals highlighted that the country is reliant on imports for 31 of the 35 critical minerals, and has no domestic production for 14 of them.

The strategy included 24 policy goals under the six major “calls to action” categories, alongside over 60 recommendations aiming to revitalize production and processing operations in the country and alleviate vulnerability against supply disruption. In addition to rebuilding domestic production, the strategy acknowledged the important role of strategic partnerships with other regions such as Canada, the European Union, Australia and Japan.”

This week, the Senate will discuss the Strategic Competition Act in order to outlast China in the new post-carbon economy. China has moved in that direction not because it cares about the planet, but because it wants to dominate the supply chains of the future. For years, China has been told that its two biggest trading partners, the U.S. and European Union, were turning off the lights on fossil fuels. Cars were going electric. Coal was getting replaced by wind and solar. And in that timeframe, China began test-driving its nascent EV market, led by BYD. Now they are the biggest consumer market for EVs. Tesla wants to be there. Their biggest car battery facility outside of the U.S. is in Shanghai.

Also in the last 10 years, China has taken its cue from Washington and Brussels and now has 8 of the top 10 solar manufacturers after dumping solar on the world and killing the European solar industry. It has roughly 7 of the top 10 wind turbine manufacturers now. The U.S. has zero.

GE Renewable Energy is based in Paris, not the U.S. It is a division of General Electric.

The reality is that China is very good at building industries because its state-owned companies can dig for raw materials and sell them to processors at a loss. The government will always keep them funded.

When China wanted to build its EV market, it turned its public bus lines into EVs and became the biggest lithium buyer in the world. They only sourced from Chinese companies. And where they didn’t have the supply in China, they invested in Africa, and elsewhere, to make it there.

Speaking to the House Manufacturing Caucus on the critical minerals supply chain earlier this month, Austin Devaney, a senior executive with Piedmont Lithium in North Carolina, said the U.S. needs a cleantech supply chain from “top to bottom”.

For solar that includes polysilicon, much of which comes from China. And solar cells, nearly all of which come from Asia.

For EVs, it means lithium and recyclables, and rare earth mines. It means battery cell manufacturers, not just battery pack assemblers.

And for wind, the U.S. is dependent on GE Renewable Energy of France and other multinationals who sometimes source large parts here at home. GE manufactures wind blades in North Dakota, but that depends on the turbine model. The Block Island offshore wind project paid for by the state of Rhode Island is a GE import.

“When you look at China and Europe, you will see that they have long-term policies around electric vehicles and climate change,” said Devaney. “Their emission standards are set for the next 15 years. That policy implementation is really critical for all the other things to follow up on.”

In Climate Push, ‘Drill, Baby, Drill’ Becomes ‘Dig, Baby, Dig.’ But China’s Doing Most of the Digging.

Ask a government official (or import lobbyist) whether a Buy American provision for solar and wind is a worthy cause and they’ll say “yes, but” – it’s more important to tackle climate change now and do it cheaply. That view instantly turns into sourcing bulk solar and EV battery materials from Asia. Wind turbines are next. Goldwind installed 48 wind turbines in the U.S. last year, versus 2 in 2019, according to the Global Wind Energy Council.

If you wonder why Beijing has jumped on the clean energy bandwagon, it’s not just because middle-class urbanites are sick of air pollution, though that is part of it. It is mostly driven by economics: China is a dominant force in every single clean energy supply chain in order to serve European and American climate change policies.

“We need to understand the real-person impact of these policies,” said Rep. Cathy Rodgers (R-WA-5) during a House Committee on Energy and Commerce hearing on May 3. “The drive to wind and solar…few are talking about how we are playing right into China’s strategic interests with these policies.”

Yet, the post-carbon world rages on. The Biden administration is following in the footsteps of our European allies in reducing the carbon footprint of the economy. It’s a worthy cause. And as President Biden says, “when I think of climate change, I think of jobs.”

“Dig, Baby, Dig”

Biden may be giving up on the old mantra of “drill, baby, drill” for hydrocarbons – as happened with fracking when he was vice president, but he will have to learn to embrace “dig, baby, dig” now.

The minerals going into EV motors, batteries, and wind turbines need to be mined. The U.S. clearly cannot mine what it does not have, but what it does have will require legislation to make sure it is happening domestically, at least in part, or risk going from fossil fuel energy security to clean energy dependence on raw materials sourced from elsewhere. Washington needs to think of the long game here. Developing mines can take 10 years or more.

“As the auto industry makes this shift, there is going to be risks and there are going to be opportunities,” said Rep. Debbie Dingell (D-MI-12) one of the lead sponsors of the CLEAN Future Act. “We have to get the policies right, or we leave this workforce behind.”

In a 287-page special report by the International Energy Agency (IEA) published this month, titled “The Role of Critical Minerals in Clean Energy Transitions”, the multilateral institution noted that a typical electric car requires six times the mineral inputs of a conventional car. A wind plant requires nine times more mineral resources than a gas-fired power plant.

Since 2010, the average amount of minerals needed for a new unit of power generation capacity has increased by 50% as the share of renewables has risen. Lithium, nickel, cobalt, manganese and graphite are crucial to battery performance, longevity, and energy density. Rare earth elements are essential for permanent magnets that are vital for wind turbines and EV motors, let alone navigational equipment on American fighter planes.

From the report:

Where Will These Minerals Come From?

Production of many energy transition minerals is more concentrated than that of oil or natural gas. For lithium, cobalt, and rare earth elements, the world’s top three producing nations control well over three-quarters of global output. In some cases, a single country is responsible for around half of worldwide production.

The Democratic Republic of the Congo and China were responsible for some 70% and 60% of global production of cobalt and rare earth elements respectively in 2019. More than half of the Congo’s cobalt mines are being dug up by Chinese state-owned enterprises who ship the rocks to China to be processed.

In going green, it will be important to consider China’s footprint in this supply chain.

The level of concentration is even higher for processing operations, where China has a strong presence across the board. China’s share of refining is around 35% for nickel, 50-70% for lithium and cobalt, and nearly 90% for rare earth elements, the IEA report states.

Chinese companies have also made substantial investments in overseas assets in Australia, Chile, the Congo, and Indonesia. High levels of concentration, compounded by complex supply chains, increase the risks that could arise from physical disruption, trade restrictions, or geopolitical strife.

It also gives China an enormous amount of leverage. Imagine imposing sanctions on a Chinese company only to watch China hoard things like semiconductors, or reduce the export of rare earth materials needed to make an F16’s navigational equipment.

This also creates sources of concern for companies that produce solar panels, wind turbines, electric motors, and batteries using imported minerals. Their supply chains can quickly be affected by regulatory changes, trade restrictions, or political instability in a small number of countries. The Covid-19 pandemic already demonstrated the ripple effects that disruptions in one part of the supply chain can have on an industry.

The report highlighted the need for recycling battery waste, something CPA supports.

For bulk metals, recycling practices are already well established, but the IEA said that this is “not yet the case” for metals such as lithium and rare earth elements.

“Emerging waste streams from clean energy technologies can change this picture,” report authors wrote.

The number of spent EV batteries reaching the end of their first life is expected to surge after 2030, at a time when mineral demand is set to still be growing rapidly. IEA estimates that by 2040, recycled quantities of copper, lithium, nickel, and cobalt from spent batteries could reduce combined primary supply requirements for these minerals by around 10%.

Some members of Congress have addressed this issue of recycling.

IEA recommends funding R&D into new recycling technologies as a way to help companies that are devising ways to turn battery waste into materials that can be used to make new batteries.

In a May 6 article in The Korea Herald, American Manganese chief technology officer Zarko Meseldzija said battery manufacturing facilities are “producing maybe 10-20% of scraps from their process. That’s an opportunity to integrate a recycling process within that facility and recycle them directly back to high-quality materials that can be used for remanufacturing of batteries.”

Lithium-ion batteries, defective or not, contain cathodes that are made of expensive metals like nickel and cobalt and account for 25% of the cost of a whole battery.

“The scarcity narrative has led to a big push to get to these metals, as we are seeing in Nevada for lithium. There are over 13,000 claims for lithium there now,” said Dustin Mulvaney, a professor with the Department of Environmental Studies from San Jose State University. “Lithium-ion battery recycling will increase over time. For us to start moving in the direction of closing the loop on some of these metals, we have to start emphasizing more on waste. There needs to be more attention on that.”

Prices for certain minerals have risen strongly since the second half of 2020, with some reaching multi-year highs. This was due to expectations of strong future growth for alternative fuel sources, as well as China’s demand (and hoarding).

As a result of this price spike and demand outlook, the IEA said it sees “ample reasons to be vigilant about the ability of supply to meet demand – especially as many governments redouble efforts to accelerate energy transitions.”

Supply Chain Resilience is Economic Security

Analysis of historical episodes of tight mineral supply provides useful insight into the factors that could help to mitigate future risks from price spikes. Mitigating activity includes mineral substitution or innovation in supply and demand technologies.

From the 1960s until the late 1980s, the Mountain Pass mine in California was the largest source of rare earth oxides in the world. In 1992 China surpassed the United States as the world’s largest producer. Since then, China has dominated the global supply of rare earths and everything dug out of the ground at Mountain Pass gets shipped to China for processing.

From the report:

This week, the Senate will discuss the Strategic Competition Act in order to outlast China in the new post-carbon economy. China has moved in that direction not because it cares about the planet, but because it wants to dominate the supply chains of the future. For years, China has been told that its two biggest trading partners, the U.S. and European Union, were turning off the lights on fossil fuels. Cars were going electric. Coal was getting replaced by wind and solar. And in that timeframe, China began test-driving its nascent EV market, led by BYD. Now they are the biggest consumer market for EVs. Tesla wants to be there. Their biggest car battery facility outside of the U.S. is in Shanghai.

Also in the last 10 years, China has taken its cue from Washington and Brussels and now has 8 of the top 10 solar manufacturers after dumping solar on the world and killing the European solar industry. It has roughly 7 of the top 10 wind turbine manufacturers now. The U.S. has zero.

GE Renewable Energy is based in Paris, not the U.S. It is a division of General Electric.

The reality is that China is very good at building industries because its state-owned companies can dig for raw materials and sell them to processors at a loss. The government will always keep them funded.

When China wanted to build its EV market, it turned its public bus lines into EVs and became the biggest lithium buyer in the world. They only sourced from Chinese companies. And where they didn’t have the supply in China, they invested in Africa, and elsewhere, to make it there.

Speaking to the House Manufacturing Caucus on the critical minerals supply chain earlier this month, Austin Devaney, a senior executive with Piedmont Lithium in North Carolina, said the U.S. needs a cleantech supply chain from “top to bottom”.

For solar that includes polysilicon, much of which comes from China. And solar cells, nearly all of which come from Asia.

For EVs, it means lithium and recyclables, and rare earth mines. It means battery cell manufacturers, not just battery pack assemblers.

And for wind, the U.S. is dependent on GE Renewable Energy of France and other multinationals who sometimes source large parts here at home. GE manufactures wind blades in North Dakota, but that depends on the turbine model. The Block Island offshore wind project paid for by the state of Rhode Island is a GE import.

“When you look at China and Europe, you will see that they have long-term policies around electric vehicles and climate change,” said Devaney. “Their emission standards are set for the next 15 years. That policy implementation is really critical for all the other things to follow up on.”

MADE IN AMERICA.

CPA is the leading national, bipartisan organization exclusively representing domestic producers and workers across many industries and sectors of the U.S. economy.

TRENDING

CPA Issues Statement of Support for New Labor Tariff Action

Trump Tells War Department to Gain Better Visibility of Critical Minerals Used by Defense Contractors

The Trade Bargain Behind America’s Cost-of-Living Crisis

CPA Welcomes FDA Proposal to Expose Hidden Foreign Suppliers in America’s Drug Supply Chain

CPA and Aluminum Extruders Council Urge Treasury to Close Solar “Domestic Content” Loophole

The latest CPA news and updates, delivered every Friday.

WATCH: WORTH FIGHTING FOR

Get the latest in CPA news, industry analysis, opinion, and updates from Team CPA.

CHECK OUT THE NEWSROOM ➔