Summary Points

- Higher import dependence makes countries more vulnerable to price shocks

- Countries that are more import dependent often experienced higher inflation during recent supply chain shocks than less import dependent countries. Comparing countries globally, every four percentage point increase in import dependence is associated with a one percentage point increase in inflation.

- The U.S. experienced some of the highest inflation rates globally during the pandemic. In 2022, the U.S. economy has the lowest manufacturing share of GDP in history so domestic production has been less able to mitigate supply shock problems. Among the many problematic results is the highest inflation seen in decades.

Introduction

The recent global crisis has led to the highest rates of inflation in forty years. Persistent global trade imbalances have given rise to differences in countries’ susceptibility to inflation during supply shock periods due to pandemic or geopolitical hostilities. That is because trade surplus countries are less import dependent and thus more resistant to supply problems abroad.

For the U.S., the long-running process of offshoring industry and jobs has effectively limited our economy’s ability to reduce supply chain shocks and subsequent higher inflation. Our lack of tariffs and other trade measures, as well as our overvalued dollar exchange rate, have made the U.S. much more vulnerable to global shocks, resulting in some of the highest inflation rates globally during the pandemic. Other countries such as Belarus, Hungary and Poland who have a high share of imports/GDP also saw a high inflation during the pandemic.

The U.S. Experience

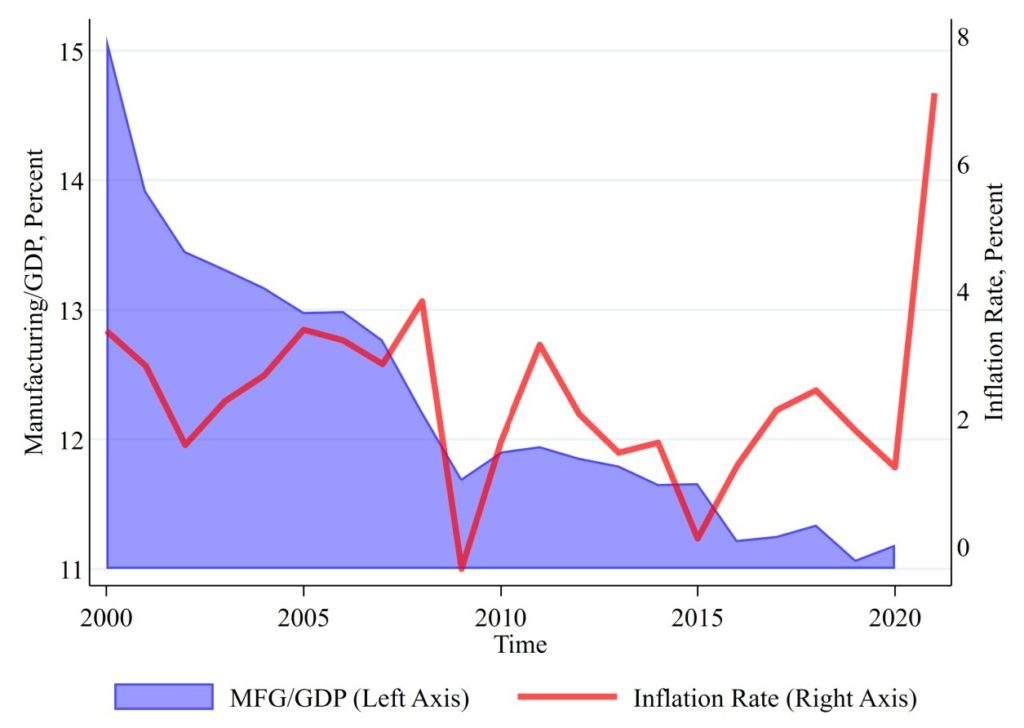

Figure 1 shows the relationship between the U.S.’s declining share of manufacturing to GDP and the average annual rate of consumer price inflation. Free trade and offshoring have resulted in lower prices as the overall trend in inflation has declined since the early 2000’s. The argument for importing from low wage, low regulation countries, with the resulting lower sticker prices, seems to work-until it doesn’t. Now facing the highest rate of inflation in decades, we have constrained our ability to mitigate supply shocks because of our decades-long process of offshoring U.S. jobs and industries.

Figure 1 shows the long-running decline of the U.S. manufacturing sector. Today, we have reached the lowest share of manufacturing to GDP while simultaneously experiencing the highest rate of inflation.

Figure 1: U.S. Manufacturing Share of GDP and Inflation, 2000-2021

Source: World Bank DataBank, U.S. Bureau of Economic Analysis, CPA Calculations

The recent spike in the inflation rate is due to a combination of events related to the COVID-19 crisis, namely supply chain shortages and a major stimulus of some $4 trillion dollars. Another contributor to the recent inflation is the ongoing Russian invasion of Ukraine, which has caused higher global oil prices.

International conflict is destabilizing for markets, should the Chinese invade Taiwan we would be directly affected because we trade a non-trivial amount with both. Under normal circumstances, the U.S. could respond to a global crisis by stimulating growth in domestic production where required. However, our reduced workforce and supply chains limit our ability to respond. Relying on imports, we are increasingly subject to global supply chain shocks, not to mention the anti-competitive price gouges that has quadrupled prices in the global shipping industry.

Import Dependence Is Correlated with Inflation

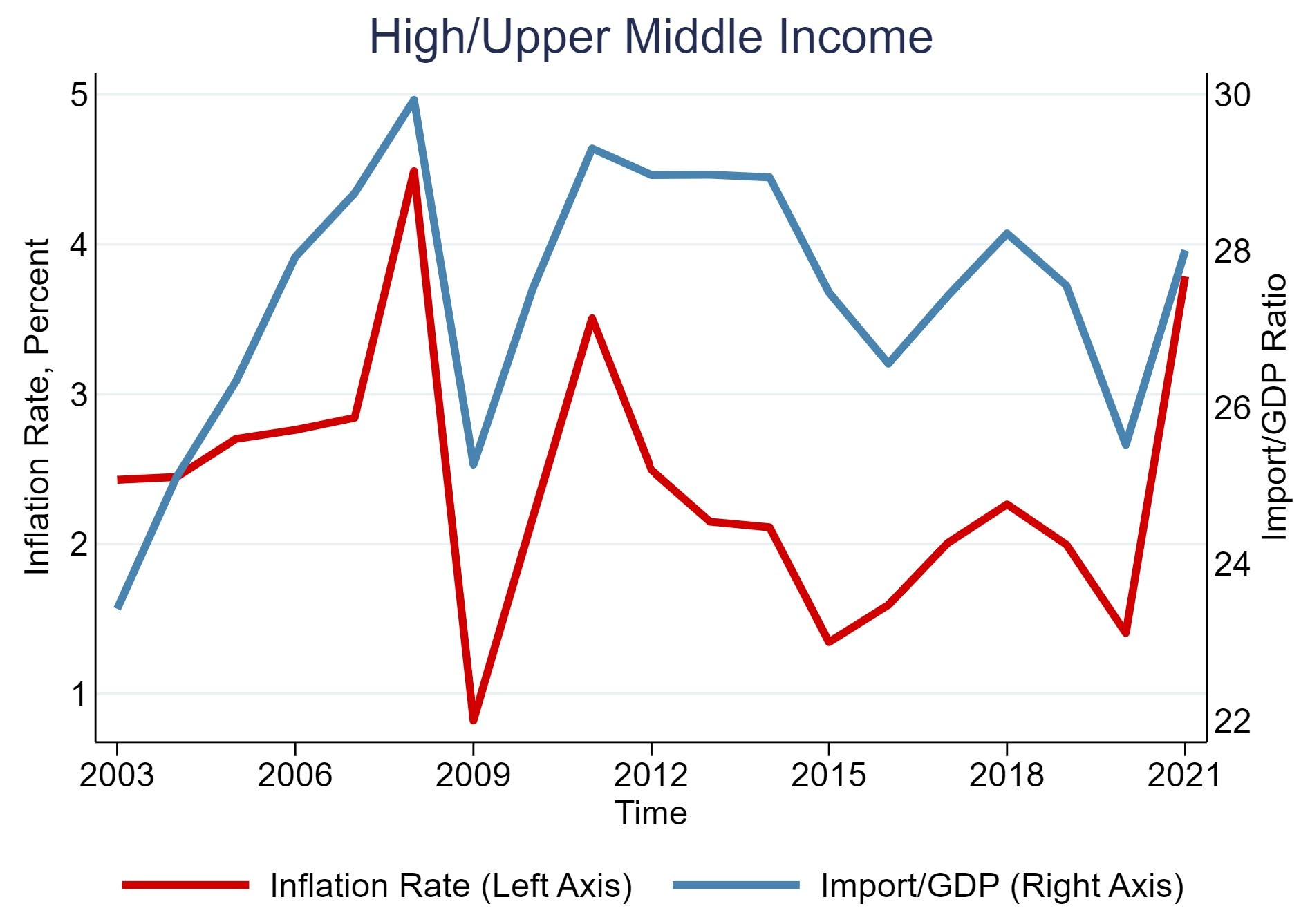

Figure 2 shows the relationship between import dependence and inflation. The figure is split between higher- and lower-income countries. This distinction is important because the average inflation rate among high- and upper-income countries tends to be lower than low/lower middle-income countries for any level of imports. The red line is the rate of inflation, and the range is displayed on the left axis. The blue line is the share of imports to GDP on the right axis. Note that the range for both series for higher and lower income countries is different.

Figure 2: Inflation and Import Dependence by Income Group

Source: World Bank DataBank, U.S. Bureau of Economic Analysis, CPA Calculations

Figure 2 shows a few important points. First, regardless of high or low income, the rate of inflation and the import/GDP ratio tend to move together over time. The correlation between inflation and the import/GDP ratio is 0.5 for higher income and 0.7 for lower. A simple regression between these two variables shows every four percentage point increases in import dependence is associated with a one percentage point increase in inflation. The relationship is even stronger among low-income countries where every four percentage point increases in import dependence is associated with a 2.7 percentage point increase in inflation.

Second, the global supply chain shocks from COVID-19 resulted in a relative increase in inflation among high income countries and relative decrease among low-income countries. The average rate of inflation for higher income countries increased from 1.4% to 3.8 % between 2020 and 2021, whereas the average rate of inflation among lower income countries dropped from 8.5% to 7.9% between 2020 and 2021.

A key driver of inflation among higher income countries were the global supply chain shocks that occurred during COVID-19. These shocks will have a higher impact on countries that import more–which tend to be higher income countries. Inflation is also driven by fiscal stimulus which tended to also be higher among high income countries during COVID.

The decline in inflation among low-income countries was driven by a few factors. While global food prices spiked amid supply shortages, many countries experienced a higher yield in their domestic market than anticipated. Further, covid supply limitations and restrictions limited exports and increased supply in domestic markets.[1] Overall, countries that have a lower import/GDP ratio experienced both a smaller price shock during COVID and a decline in prices rather than increase.

Country Level Comparison

Higher income countries such as Estonia, Belarus, and Lithuania saw the largest increases in inflation between 2020 and 2021 and they also have a large (more than 65%) share of imports/GDP. In 2021, the U.S. experienced the second highest rate of inflation among high income countries (7.1%), while China, the U.S.’s largest source of imports and with positive net exports, saw an inflation rate of less than 1%.

Countries with a high share of imports/GDP such as Hungary (81%), Kyrgyz republic (69%), and Belarus (66%) saw high rates of inflation in 2021, reaching 5%, 11%, and 9% respectively. Similarly, countries with a low share of imports/GDP such as China (17%), Australia (17%), and Indonesia (18%) saw low rates of inflation during 2021, reaching 0.9%, 2.8%, and 1.5% respectively.

While the U.S. experienced one of the largest increases in inflation during COVID, it has a relatively low import/GDP ratio (~15%). While the ratio of imports/GDP is informative, the absolute level of imports also contributes to domestic inflation. So, while the U.S. has a relatively small share of imports/GDP, it is highly dependent on imports in certain sectors, which led to shortages and price increases. The shortage of semiconductors for automobiles and its impact on prices of new and used autos is an example.

Conclusions

Proponents of free trade tend to focus on the price-reducing effect of lower tariffs and other trade barriers. A critical weakness in this argument however is that our increasing dependence on imports is a double-edged sword-we also become more vulnerable to inflationary spikes at the will of foreign actors or international markets.

The data shows that import dependence has been correlated with inflation across time and countries. Many countries that were import dependent were more vulnerable to global supply shocks and as a result saw higher inflation during 2021. Many countries experienced painful inflation during COVID because they could not produce what they needed. The U.S. also experienced this problem because we chose to offshore many jobs and productive capacity.

U.S. policy has focused on the importance of price rather than jobs and capacity and we are paying higher prices for it now. Since the U.S. joined the WTO and lowered its trade barriers, the share of U.S. manufacturing has declined. While we have enjoyed lower prices, we have lost millions of jobs and the fabric for a strong supply chain that could have mitigated the higher prices were paying today.

The free trade policies adopted by the U.S. are not the only cause of high U.S. import levels. The flood of imports has been made possible by the anti-competitive subsidization of capital, land, and labor by foreign countries, particularly China. Free trade policies are a disadvantage for U.S. firms in an anti-competitive global trade market. The U.S. must adopt a range of industrial policies, including but not limited to tariffs, to neutralize these anti-competitive practices and create greater opportunities for U.S. firms at home and abroad.

[1] “Rwanda”, IMF Country Report, No. 22/200, June 2022