Key Points

- Steel imports from Mexico have surged over the past several years. U.S. steel imports from Mexico have risen by 141% over historic levels, with some subcategories of imports tripling and quadrupling, despite a 2019 U.S.-Mexico agreement to maintain steel imports at past levels.

- The surge in steel imports in Mexican steel conduit, used in construction, led to the closure last year of a Long Beach, California steel factory with the loss of 145 union jobs.

- Excessive Mexican steel imports, in addition to the global oversupply of steel harms U.S. steel manufacturers by reducing revenue, investment and employment in the U.S. steel industry. The Biden administration should consult with the Mexican government per the 2019 agreement and if agreement cannot be reached, re-impose the Section 232 tariff of 25% on all Mexican steel imports.

In May 2019, a little over one year after the Trump administration ordered Section 232 tariffs of 25% tariffs on steel imports to the U.S., the U.S. and Mexico entered into an agreement that steel products could enter the U.S. duty free. The key terms of the agreement allowed for duty-free import of Mexican steel so long as Mexico maintained imports at historic levels. Despite such an agreement, Mexican steel imports have surged far beyond such levels over the past two years.

Steel Imports from Mexico Surge in Recent Years

Instead of maintaining imports at historic levels as agreed, Mexico has exceeded the agreed upon import levels. Over the past two years, Mexican steel imports have more than doubled in terms of value and increased in volume of metric tons by about half.

As shown in Table 1, U.S. steel imports from Mexico far exceed historical import volumes and values. The table shows steel imports according to the Harmonized Tariff Schedule (HTS) of iron and steel products (Chapter 72) as well as articles derived from iron and steel (Chapter 73). This analysis compares recent years of U.S. steel imports from Mexico to the average steel imports over the benchmarked period from 2015 to 2017.

TABLE 1: Value of Steel Imports to the U.S. from Mexico (Benchmark versus 2022)

| Benchmark Period (2015-2017) | 2021 Imports | 2022 Imports | 2022 Compared to Baseline | |

| Iron & Steel (Chapter 72) |

$1.5 B | $4.5 B | $5.5 B | 262% |

| Articles Made of Iron & Steel (Chapter 73) |

$4.2 B | $6.5 B | $8.2 B | 96% |

Source: U.S. Census Bureau (General Customs Value, HTS 72 & 73)

Note: Figures in billions of dollars; 2022 imports annualized from YTD totals through November 2022

The surge in U.S. imports from Mexico is even higher for various subcategories of steel imports. As shown in Table 2, imports of flat-rolled steel products have increased by 351% comparing annualized 2022 figures to the historical benchmark. For imports of steel conduit (included in HTS 7306.30.5028), the surge reached 417%. The surge in conduit imports into the western U.S. reached such a high level last year that Zekelman Industries was forced to close its Long Beach, California factory, with the loss of 145 jobs. Zekelman has asked the U.S. Trade Representative to take action to enforce the 2019 steel agreement with Mexico.

TABLE 2: Value of Selected Steel Import Subcategories to the U.S. from Mexico

(Benchmark versus 2022)

| Benchmark Period (2015-2017) | 2021 Imports | 2022 Imports | 2022 Compared to Baseline | |

| Other tubes, pipes, and hollow profiles, internally coated or lined (not exceeding 114.3 mm) (HTS 7306.30.5028) |

$14 M | $56 M | $71 M | 417% |

| Flat-rolled products (width of 600 mm or more, hot-rolled) (HTS 7208) |

$168 M | $436 M | $759 M | 351% |

| Wire of stainless steel (HTS 7223) |

$0.6 M | $0.3 M | $2.4 M | 273% |

| Other structures and parts of structures (HTS 7308) | $520 M | $1,303 M | $1,886 M | 263% |

| Semifinished products of iron (HTS 7207) |

$218 M | $745 M | $706 M | 223% |

| Other tubes, pipes and profiles (HTS 7306) |

$350 M | $489 M | $740 M | 111% |

Source: U.S. Census Bureau (General Customs Value)

Note: Figures in millions of dollars; 2022 imports annualized from YTD totals through November 2022

Overall, the value of Mexican steel imports has more than doubled compared to historic levels, up 141% in 2022. As shown in Table 2, some steel products have increased by as much as 4 times the previous imported values prior to the Section 232 tariffs. For example, flat-rolled steel products have quadrupled in value imported. Among the 53 four-digit HTS codes with imports of Mexican steel to the U.S., only nine are at or below the value of imports in the same classifications over the benchmark period while 43 classifications have increased by 25% or more.

When measured in volume of metric tons of steel imported, the same pattern of surging Mexican steel imports holds true as in the above figures in dollar value. In other words, the surge in imports is not a surge in price but a surge in volume of tons Mexico is sending across the border. According to the Department of Commerce, the U.S. imported 4.4 million metric tons of steel from Mexico in 2022 (through November), an annualized estimate of 4.8 million tons, and 4.3 million metric tons in 2021 compared to an average of 2.8 billion metric tons from 2015 to 2017. Mexico has exported a sustained increase of steel to the U.S. over the past two years by more than half as much compared to past volumes.

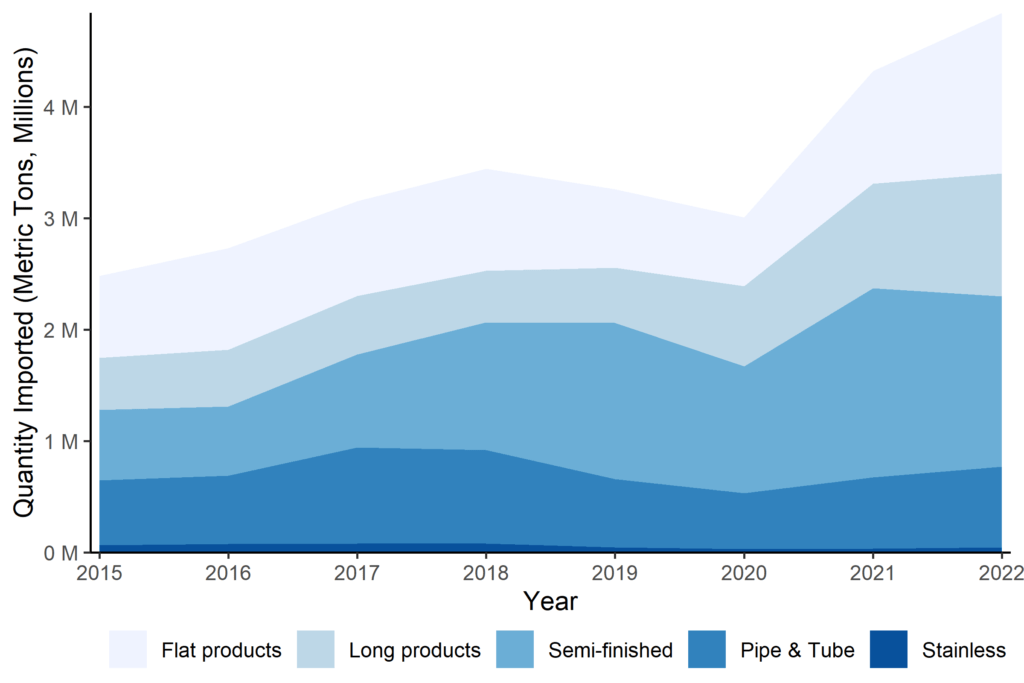

The three largest product categories of Mexican steel imports have all seen significant and sustained increases over the past two years. Comparing annualized 2022 totals to the benchmark period flat steel products are up 73%, semi-finished steel up 120%, and long products steel up 120%. Pipe and tube steel products and stainless steel imports have remained roughly equal in quantity to the benchmark period.

Mexico has clearly not held their end of the agreement to limit steel imports to the U.S. at historical levels. Instead, steel imports from Mexico to the U.S. have surged over that time period both in terms of value and quantity.

FIGURE 1: Volume of Steel Imports from Mexico to the U.S.

Source: Global Steel Trade Monitor, U.S. Department of Commerce, Enforcement and Compliance

Note: Total 2022 import quantity is annualized from YTD totals through November 2022

Lack of Increase in Demand to Justify Increased Steel Imports

An increase of consumption of steel or steel products might hypothetically explain why Mexican steel imports have surged in recent years despite the previous agreement. However, there are no significant shifts in demand that would justify such increases.

Construction accounts for about half of global steel demand. Yet, trends in construction do not track the same increase in imported steel from Mexico. Construction spending increased over the past two years before leveling off in recent months due to less investment because of the cooling economy.

Furthermore, total global imports of steel to the U.S. have decreased in recent years. Therefore, as Mexican imports have increased, this means the share of Mexican steel entering the U.S. market has increased as a proportion of the global share.

There is no evidence of a shift on the demand side to justify the increase of supply of Mexican steel imported to the U.S. The increase of imports from Mexico indicates that it is not adding industrial capacity to meet its own needs nor an increase in demand for steel in the U.S. market.

The agreement stated that “In the event that imports of aluminum or steel products surge meaningfully beyond historic volumes of trade over a period of time, with consideration of market share, the importing country may request consultations with the exporting country. After such consultations, the importing party may impose duties of 25 percent for steel and 10 percent for aluminum.” In our view, the U.S. government should proceed immediately to consultations and if action is not taken to reduce Mexican imports back to historic levels, the U.S. government should re-impose 25% duties on all Mexican steel imports.

Duty-free access to the U.S. domestic market has made steel production in Mexico an attractive transshipment point. For example, after the U.S. imposed Section 232 tariffs on steel imports from China, some Chinese companies relocated production to Mexico to avoid tariffs on the finished products. China has a huge overcapacity in steel production that has flooded global markets and forced steel plants in the U.S. and elsewhere to shut down, laying off thousands of workers. The global market for steel is about 1.5 billion metric tons annually, but global capacity equates to 2.3 billion tons annually. China accounts for 75% of new steel capacity over the past two decades.

The Biden administration needs to take a firmer stance toward steel imports from Mexico to ensure fairness for U.S. steel manufacturers and workers employees. The U.S. government should consider re-imposing tariffs on Mexican imports. Another possible course of action is to impose quotas similar to those placed on South Korea. Such a system would allow Mexico to export steel duty-free to the U.S. only up to an agreed historic level.

Thousands of Tons of Steel From Mexico Originated Elsewhere

The 2019 agreement specifically calls for steel products not melted and poured in North America to be treated differently from steel that originates in North America. As of November 2022, according to the Department of Commerce’s SIMA database, approximately 16% of steel imports from Mexico were melted and poured outside of North America. Brazil is the largest source of melted and poured steel that is imported from Mexico to the U.S. accounting for about 502,000 metric tons of flat-rolled steel, or 11% of imported steel from Mexico. Direct action should be taken to ensure that these imports are treated differently than North American melted and poured steel in any new agreement with Mexico.