Key Points

- The CPA Pro-Growth Model provides superior analysis of the impact of changes in trade and industrial policies and their impact on the U.S. economy.

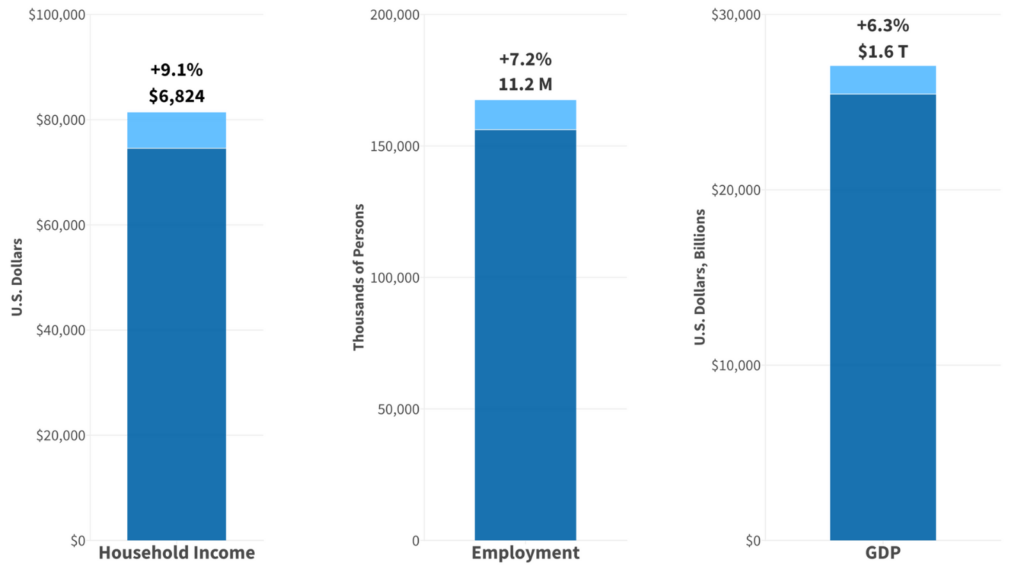

- Tax credits for all U.S. manufacturing sectors would stimulate the economy, create 11.2 million new jobs, and increase real household income by 9.1%. Real GDP would grow by 6.3%.

- The boost in economic activity would generate $226.1 billion in additional tax revenue for the federal government.

- The CPA Pro-Growth model modifies the standard GTAP model to allow firms to respond to changes in demand, increasing investment and employment.

Economic models of international trade and industrial policies have been unrealistic and biased towards free trade. The widely used GTAP model (Global Trade Analysis Project) makes assumptions that bias the model and its results in favor of free trade. Many of these assumptions do not account for how markets operate in the real world. GTAP has been used to forecast the impact of trade events from NAFTA to China’s winning Most Favored Nation status, to the Trump tariffs of 2018. In every case, its predictions of changes to U.S. exports and imports have been wrong, so much so that modeling economist Tim Kehoe of the University of Minnesota performed a postmortem analysis in which he concluded there was “zero predictive accuracy” in GTAP model forecasts for NAFTA.

At CPA, we are working to rectify these weaknesses by modifying the Global Trade Analysis Project (GTAP) model to include the stimulus to domestic demand and production that can result from import restriction. In this simulation we look at the effects of a direct stimulus to domestic manufacturing production.

In previous simulations, we looked at the positive effects tariffs can generate in the domestic economy (see here and here). Tariffs were the preferred trade policy of the Trump administration. The Biden administration has favored tax incentives (aka “industrial policy”) to support domestic production and investment in targeted industries.

The Biden administration’s industrial policies have generally aimed at providing support to specific domestic industries for climate or national security goals. In this simulation we look at the use of tax incentives targeted at the entire manufacturing sector for macroeconomic goals, i.e. increasing national income and providing more jobs and better-paying jobs.

Early signs from U.S. economic data suggest that the Inflation Reduction Act and the CHIPS Act are having a substantial effect on domestic manufacturing. Total construction spending in manufacturing has nearly tripled over the past two years. August 2023 saw manufacturing construction spending reach a record monthly high of $17 billion. At the same time, manufacturing employment is starting to tick up from recent all-time lows as a percentage of the total workforce. In September, it surpassed 13 million manufacturing jobs for the first time since the Great Recession. These indicators suggest substantial increases in manufacturing output should be expected next year.

In this simulation, we use our CPA Pro-Growth Model to assess the impact of increasing production in all manufacturing sectors via corporate tax credits coupled with a requirement to invest in increasing domestic production. We model IRA-style tax credits in GTAP as a reduction of the tax burden for each manufacturing sector by 50%, which cuts manufacturing costs in the model and leads to increased investment. Our previous simulations model how increases in tariffs grow the U.S. economy and creates jobs. This simulation shows an alternative strategy to create economic growth by stimulating production by providing tax credits for U.S. manufacturers.

CPA Pro-Growth Model

The CPA Pro-Growth model is a modified version of the standard Global Trade Analysis Project (GTAP) model often used to evaluate the economic impact of trade policy proposals. Our model aggregates the default GTAP database into 26 sectors and three regions (the U.S., free trade agreement countries, and non-free trade agreement countries).

We introduce tariff productivity elasticities into the model, allowing domestic producers to increase output and leverage the opportunity that a tariff provides. That feature has no impact on this analysis as tariffs are not involved. However, we also introduce primary factor supply elasticities for labor and capital. These allow firms to respond to an increase in demand by increasing their capital investment and employment. Firms can increase output and employment, as can the national economy as a whole.

Given the tripling of manufacturing construction investment due to Biden administration industrial policies, it is fair to say that our model captures this dynamic that tax credits work to stimulate investment. While the boom in manufacturing production is yet to be seen, construction spending likely precedes the boost in output that will come over the next several years. Our model reflects these economic forces.

Results: Tax Credits for Manufacturing Grow the U.S. Economy

Model results show that stimulating production for domestic manufacturers would grow the U.S. economy and create jobs. Our model finds that providing U.S. manufacturers across all sectors with a 50% reduction in their tax burden would increase real household income by $6824, or 9.1%, and create 11 million new jobs. Firms across all manufacturing sectors create new jobs as they expand production. The economy would grow by $1.6 trillion, or 6.3%, in real GDP.

Figure 1: Tax Credits for U.S. Manufacturers Stimulates Household Incomes, Jobs, and GDP

Source: U.S. Census Bureau, Bureau of Labor Statistics, Bureau of Economic Analysis; CPA Calculations

Manufacturing output would increase by 31.9%. This includes powerful growth in some large manufacturing sectors. Figure 2 highlights key sectors with significant output increases. Machinery manufacturing gains most as it grows by 60%. Other sectors grow by about half in production output as Textiles (53%), Pharmaceuticals (48%), Apparel (45%), and Ferrous Metals (42%). All manufacturing sectors increase output and grow by double-digit increases (except for petroleum products, which grows by 7%).

Figure 2: Top Manufacturing Increase by Sector from 50% Reduction in Corporate Tax Rate by Sector

As a result of the increase in production and domestic supply of finished goods, consumer prices of manufactured goods fall substantially across all manufactured goods by a combined average of -14.9%. However, demand increases for intermediate goods due to the boost in manufacturing production. This puts an upward price pressure on primary products (6.1%) and prices for agricultural goods (3.8%).

The increase of household income leads to excess disposable income. This leads to a rise in prices in the service sector of 13.5%.

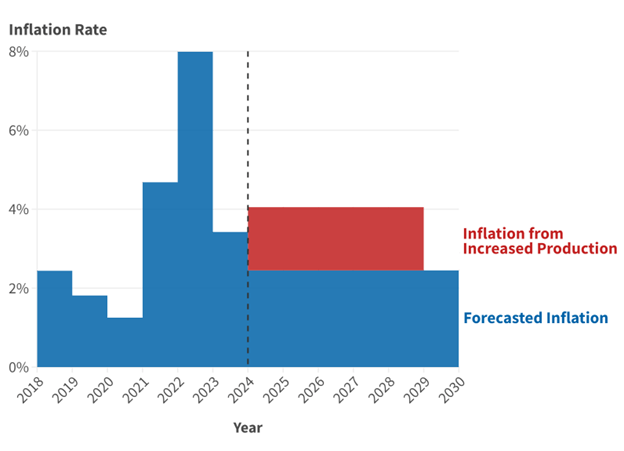

The model also shows a sharp increase in exports by 19% as U.S. produced goods become more competitive in the global market, which decreases total goods available for domestic consumption. Overall inflation of consumer prices is 8%. Since the model looks at a transition period which could take roughly four to eight years, we chart the impact over a six-year period. Figure 3 shows this adds roughly 1.3 percentage points to inflation over that period. Note that growth in household incomes and output are in real terms, i.e. after taking account of inflation.

Figure 3: Forecasted Rate of Temporary Inflation from Corporate Tax Rate Reduction

Source: Federal Reserve Bank of St. Louis; CPA Calculations

Growing Economy Generates Additional Tax Revenue

The increase in production and economic activity throughout the economy spurred by the boost to the manufacturing sector would also generate additional revenue for the U.S. federal government. Assuming that federal revenue grows in proportion to the growth in GDP (while accounting for a reduction in the total corporate tax paid by manufacturers), the U.S. Treasury would receive about $226.1 billion in additional revenue.

In FY 2023, the federal government collected $4.441 trillion and corporate tax accounts for $419.6 billion, or about 9% of all federal receipts. Reducing the corporate taxes collected from manufacturers, which accounts for 37% of corporate tax receipts according to the Internal Revenue Service, would reduce corporate taxes receipts by $53.7 billion. Providing a tax credit only reduces corporate tax revenue by about 34% among manufacturers given their boost in output. Total federal receipts would increase by a net $226.1 billion from the additional economic activity from stimulating production in the manufacturing sector.

The increase in economic activity would provide policymakers with a revenue source to pursue an array of potential policies as they choose. Additional revenue could be used to further investment in key manufacturing sectors, social programs, or it could finance a substantial reduction in the individual taxes paid by millions of Americans.

Employment and Labor Force

Employment growth of 11 million jobs in a labor market that is already considered near full employment deserves additional context. Most of the employment growth is in the manufacturing sector, following the tax credits and production boost. 78% of the employment growth is in manufacturing and manufacturing employment as a share of total employment would grow by 4 percentage points. Manufacturing jobs pay above the average wage and offer benefits packages, which could attract new workers into the U.S. economy. The labor force participation rate remains 4.5 percentage points below its peak, suggesting strong economic growth would attract new workers into the workforce, particularly in the younger age cohorts.

Comparing Tax Credits with Tariffs

In comparison with our previous simulations of tariff increases, we find corporate tax credits provide a comparatively larger boost to manufacturing production and employment. This is because the direct impact on manufacturing investment is highly stimulative for the U.S. economy. Both of our tariff scenarios, the 35/15 (35% on manufacturing sector and 15% on other sectors, with all free trade agreement countries exempt from all tariffs) and the universal 10% tariff provide significant stimulus. But the model finds the stimulus relatively modest, based on historical evidence of tariffs in high-cost countries like the U.S., combined with the free trade agreement country exemption, which waters down the U.S. impact of the tariffs. Tariffs applied only to non-free trade agreement countries leads to trade diversion, i.e. increased imports from free trade agreement countries, which offsets some gains to domestic producers. In the case of a 10% universal tariff, the increase in tariffs is too small to generate the same output increases of a 50% tax credit of the magnitude modeled here.

As a whole, these various policy scenarios provide insight into how both tariffs and tax credits can be used to stimulate domestic production. Our results show us that tariffs should be set high enough and broad enough to effectively provide import restriction.

Tax credits come with their own policy lessons. When linked to production, corporate tax credits generate large increases in output and employment. Recent legislation, the IRA and CHIPS Act, shows how requiring domestic investment to claim the tax credit boosts total national investment and GDP. In contrast, unilateral unconditional corporate tax cuts such as the 2017 Tax Cut and Jobs Act (TCJA), which lowered the corporate tax rate from 35% to 21%, had no discernible impact on investment. Our model and years of experience in the U.S. and foreign economies suggests that unconditional tax cuts on their own do not stimulate production.

Conclusion

The CPA Pro-Growth Model shows that providing corporate tax credits to domestic manufacturers contingent on domestic investment to increase production in all manufacturing sectors delivers a powerful stimulus to the U.S. economy. The powerful growth in manufacturing stems from the reduced costs for U.S. manufacturers and the large opportunity for share gains in the U.S. market as U.S. manufacturers win share from imports. The export growth of 19% provides additional stimulus to U.S. production. The higher incomes and output in manufacturing feeds through to the service sector, providing more demand for services and more jobs in that sector. The result is broad-based economic growth throughout the U.S. economy.