KEY POINTS

- U.S. manufacturing has fallen from 21-25% of GDP in 1950s to about 10% today.

- The decline is worse than the average of first world developed countries. The result is an unbalanced economy excessively dominated by services and imports.

- Japan, Germany, and other developed countries have maintained strong manufacturing sectors at 15-25% of GDP.

- The U.S. should set a clear national goal of boosting manufacturing to at least 15% of GDP to re-establish a healthy balance of goods vs services and exports vs imports.

For decades, the United States has operated without a clearly defined industrial policy, relying instead on market forces and private sector innovation to guide domestic manufacturing. However, free trade has allowed imported goods to flood the U.S. market and undermine domestic producers, causing manufacturing’s long-decline in the United States. U.S. manufacturing currently accounts for around 10% of the U.S. GDP (1), a significant decline from the 1950s through the 1970s when it comprised 21-25% of GDP. (2)

Though manufacturing globally has been on the decline, the U.S. has been a particularly poor performer among the club of first world developed nations. This paper argues that lack of economic diversity, and the resulting concentration in services, and financial sector, makes the US and any country more fragile and less resilient in times of peace as well as in times of crisis. The recent re-emergence of tariffs and industrial policy has been a positive development, but there has not yet been a clear goal for the overall outcome.

We propose that the US should set a goal of increasing manufacturing to at least 15% of GDP, a number benchmarked to the mere average of first world economies. The objective need not decide the composition of industries, which is a related topic. Such a goal can help guide future policy debates and implementation beyond merely hoping a good result follows. It is a reasonable goal given the experience of peer nations. And it will rediversify our economy for resilience, growth, and national security.

U.S. Manufacturing Behind Peer Countries

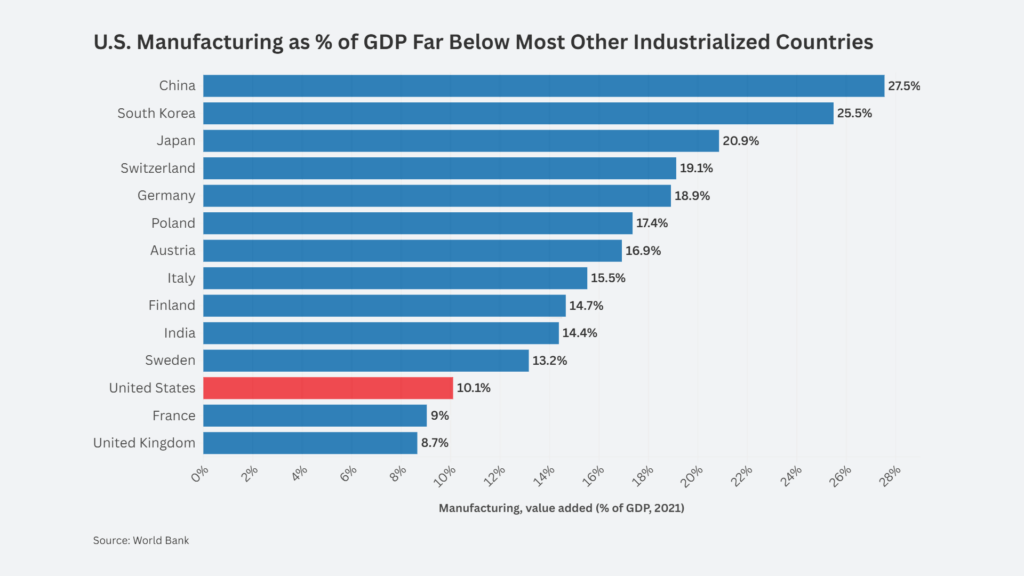

Even though the United States has lost a substantial portion of its manufacturing sector, this has not been the experience of all modern industrial economies. As shown in Figure 1, countries like Germany, South Korea, and Japan have maintained their manufacturing sectors at about 19-25% of GDP, a level the U.S. has not had since around 1980. In fact, the U.S. is substantially below average compared to other peer economies in terms of manufacturing’s share of total GDP. Even other high-cost countries like Switzerland, Finland, and Austria have managed to keep their manufacturing sectors at around 15% of GDP or higher.

FIGURE 1:

Japan is one of the best examples for how a thorough and long-term industrial policy can reap massive gains for a country’s industry. A U.S. Congressional study sums up Japan’s industrial policy, stating “Policies towards nurturing an internationally competitive automobile industry followed a pattern similar to those of the steel industry: heavy protection and subsidization, incentives for investment in technology, and increased concentration in the industry.”(3) These policies also allowed Japan to excel in industries such as electronics in future decades and maintain a strong manufacturing presence to this day.

Conversely, some industrialized countries have experienced even worse manufacturing declines than the United States. The United Kingdom’s manufacturing sector now only comprises less than 9% of GDP and the UK’s GDP per capita has actually started to fall, going from $50,398 in 2007 to $48,867 today (4). British economist Walter Eltis attributes the UK’s long-term stagnating wages directly to the decline in manufacturing, stating “few can doubt that the UK would have achieved a higher GDP and a lower natural rate of unemployment if manufacturing industry had been able to win a higher share of world markets and the UK home market.” (5)

Need for a Dual Approach with Tariffs and Industrial Policy

The manufacturing decline in the U.S. and other western countries stems from several factors, including the offshoring of production to lower-cost countries and lacking policy support to retain and grow domestic manufacturing. This shift has left the U.S. more dependent on foreign suppliers for essential goods, impacting everything from consumer electronics to critical materials needed for national defense.

This lack of economic diversity has left the United States much more fragile during crises. For example, an NIH study outlined how during the COVID crisis, “With heavy reliance on global suppliers, America struggled to secure the necessary equipment and protective gear when the health crisis hit and disrupted nearly every link in the global supply chain.” (6) The U.S. was over-reliant on foreign manufacturers, with insufficient industrial base to meet demand during a crisis. The study continues, “Throughout the three waves of infection, there were glaring deficiencies in the domestic manufacturing ability to provide necessary supplies.” (7)

The U.S.’s overreliance on imports has also contributed to price volatility in recent years. According to a study by the Federal Reserve, during the COVID crisis, “The shift in demand toward durable goods consumption and the heavy reliance on foreign suppliers to produce these goods has created a mismatch between supply and demand resulting in price increases. Sectors that rely more heavily on foreign inputs from countries that faced stronger disruptions experienced larger increases in PPI inflation.” (8) Reshoring manufacturing to 15% or more of GDP will help reduce inflation risks caused by global supply chain disturbances.

To address these issues, the U.S. needs a more robust industrial policy focused on expanding domestic manufacturing. The Trump and Biden Administrations have started to implement elements of such a strategy, including the Trump tariffs and Biden’s Inflation Reduction Act, but the U.S. needs more. The United States should adopt a dual approach of tariffs and targeted industrial policies aimed clearly at increasing manufacturing’s share of GDP to at least 15%. Wide-ranging tariffs on key industrial sectors would provide a substantial boost for domestic producers and encourage companies and investors to build a robust domestic supply chain.

A clear industrial policy is also needed sufficiently build domestic industries, especially in high investment cost industries and other key economic sectors. This could include subsidies, tax incentives, or grants for domestic manufacturers in high-tech and strategic sectors, such as semiconductors, electric vehicles, and advanced materials. Investment in workforce development would be equally important, ensuring that U.S. workers have the skills needed for these modern manufacturing roles. Additionally, aligning federal funding for R&D with private sector needs would support innovation and efficiency gains across industries. Together, tariffs and industrial policies would help rebuild the U.S. manufacturing base, enhancing resilience, reducing dependency on foreign imports, and creating well-paying jobs in a reinvigorated sector. The economic rebalancing would greatly contribute to the long-term health of the U.S. economy, boosting both our economic resilience and prosperity.

Conclusion

Revitalizing U.S. manufacturing is both an achievable and essential goal for strengthening the economy and safeguarding national security. By setting an ambitious target to raise manufacturing’s share of GDP to 15%, the U.S. can more clearly measure the success of its industrial policy to rebalance the economy. As the experience of countries like Japan and Germany has shown, robust industrial policies—featuring targeted tariffs, strategic investments, and workforce development—can drive sustained manufacturing growth in a high-cost economy.

(1) Value added by industry: Manufacturing as a percentage of GDP. (2024, September 26). https://fred.stlouisfed.org/series/VAPGDPMA

(2) Yuskavage, R., & Fahim-Nader, M. (2005b, December). Gross Domestic Product by Industry for 1947–86. U.S. Bureau of Economic Analysis. https://apps.bea.gov/scb/pdf/2005/12December/1205_GDP-NAICS.pdf

(3) U.S. Congress, Office of Technology Assessment, Competing Economies: America, Europe, and the Pacific Rim, OTA-ITE-498 (Washington, DC: U.S. Government Printing Office, October 1991).

(4) World Bank Open Data. (n.d.). World Bank Open Data. https://data.worldbank.org/indicator/NY.GDP.PCAP.CD?locations=GB

(5) Eltis, Walter, and David Higham. “Closing The UK Competitiveness Gap.” National Institute Economic Review 154 (1995): 71–84. https://doi.org/10.1177/002795019515400105.

(6) Ngo, C. N., & Dang, H. (2022). Covid‐19 in America: Global supply chain reconsidered. World Economy, 46(1), 256–275. https://doi.org/10.1111/twec.13317

(7) Id.

(8) Santacreu, A. M., & LaBelle, J. (2022, April 21). Global Supply Chain Disruptions and Inflation During the COVID-19 Pandemic. Federal Reserve Bank of St. Louis. https://www.stlouisfed.org/publications/review/2022/02/07/global-supply-chain-disruptions-and-inflation-during-the-covid-19-pandemic