By Steven L. Byers, PhD, and Jeff Ferry

Last year the US registered its largest trade deficit in 12 years and its largest-ever deficit in goods trade. In this article, we review the main trends in US international trade in 2020.

- The US trade deficit continued to deteriorate in 2020 as it rose to a 12-year high $679 billion, a 17 percent increase over 2019.

- The goods deficit was the highest on record, $915.8 billion.

- The COVID pandemic suppressed both exports and imports in 2020, but exports fell by more, contributing to the larger trade deficit.

- Our goods deficit with China fell for the 2nd consecutive year, demonstrating the effectiveness of the Section 301 China tariffs.

- Our goods deficit with Vietnam rose by 24.9%, making it our third largest deficit country.

-

The strength of the dollar continued to exacerbate our trade deficit. Although the dollar declined in the second half of 2020, it is still 10% higher than it was 15 years ago.

As a result of COVID-19 related government lockdowns worldwide economic growth and associated global merchandise trade were severely disrupted in 2020. The United Nations Conference on Trade and Development (UNCTAD) recently estimated that global merchandise trade fell 5.6% in 2020, the largest decrease since 2009, when merchandise trade fell 22%. Services trade, which includes tourism, fell by a larger amount, an estimated 15.4%.

U.S. Economic Trends: GDP and Trade

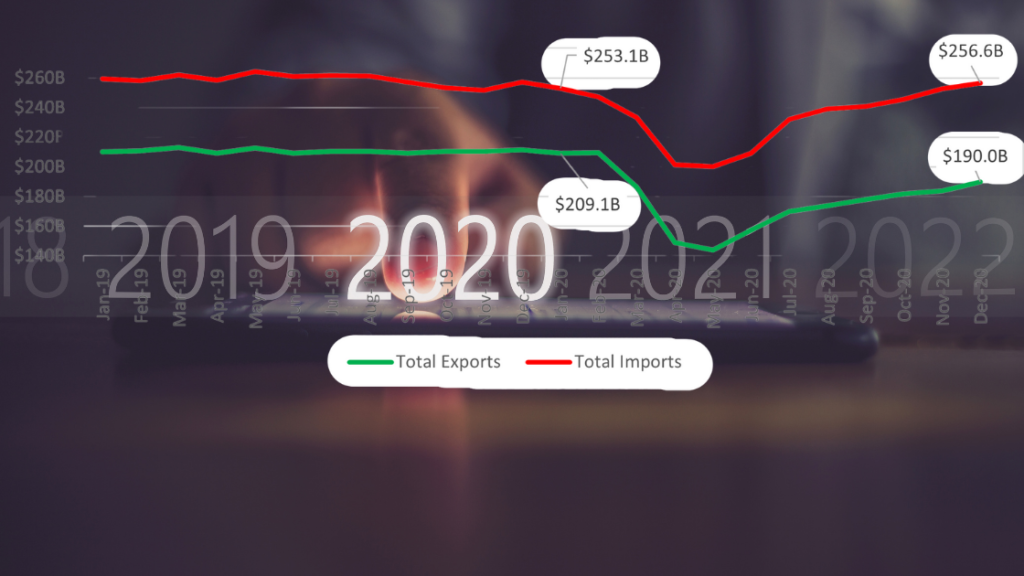

Last year US real Gross Domestic Product (GDP) shrank by 3.5 percent, the first economic contraction since the Great Recession in 2009. As a result of the Covid-19 pandemic, businesses were shuttered, and millions of workers became unemployed. Total US exports declined 15.7% and imports fell 9.5%, resulting in a widening of the trade deficit of $101.9 billion, 17.7% higher than in 2019. Exports of goods and services ($2.1 trillion) was the lowest since 2010 ($1.9 trillion). Similarly, imports of goods and services ($2.8 trillion) was the lowest since 2016 ($2.7 trillion).

Imports declined less than exports primarily because emergency federal spending programs helped moderate the decline in US consumption. The US government sent two stimulus payments to consumers in the first half of 2020, along with direct support to businesses. Simultaneously, the US Federal Reserve pursued a massive program of monetary stimulus and quantitative easing which lowered the cost of borrowing resulting in a wave of mortgage refinancing and corporate bond issuance. As a result, both exports and imports rebounded beginning in June, but imports rebounded close to pre-pandemic levels, while exports remained lower by approximately 9%, as shown in Figure 1 below.

US imports were led by pharmaceuticals ($162.8 billion), followed by passenger cars ($141.7 billion), cell phones and other household goods ($98.5 billion). Pharmaceutical imports increased by 9.2% from 2019, a smaller increase than in 2019 (12.1%) or 2018 (20.4%). Pharmaceutical imports increased by 9.2% from 2019, a smaller increase than in 2019 (12.1%) or 2018 (20.4%).

US exports were dominated by aircraft (including parts and equipment) with $71.6 billion, followed by pharmaceuticals ($59.4 billion), industrial machines ($57.3 billion), and semiconductors ($55.3 billion). Aircraft related exports plunged following the grounding of the Boeing 737 Max over safety issues. Semiconductor exports rose as pandemic shutdowns led to increased consumption of computers, video games, and other Internet-related equipment.

Bilateral Goods Trade Balances

China continued to be the largest US deficit country, measured by goods trade. The US goods trade deficit with China fell 10 percent last year to $311 billion. The decline in our China deficit, down 26% since it peaked in 2018 at $419 Billion, shows that the Trump Section 301 tariffs were effective in reducing US dependence on China imports. However, the news is not all good. The largest part of the reduction imports from China was replaced by imports from other nations, which helps to explain why our total goods deficit ($916 billion) was the highest ever. Still, in today’s world, with US agricultural exporters struggling to gain access to container ships to ship product sitting on west coast docks, any reduction in dependence on China is welcome.

As part of his negotiations with China, President Trump agreed a “Phase One” deal at the start of 2020. One year, later, it is clear from Peterson Institute analysis PIIE US China – Phase One that China failed to meet the targets it agreed to. In any case, that deal does little to address the huge imbalance in US manufacturing trade with China. President Biden, who has said that his administration will not change the China tariffs in the short term, has yet to reveal his administration’s policy stance towards China.

The US goods deficit with the European Union edged up by 2% to $182.2 billion, the highest figure on record. Our deficit with Germany, the EU’s largest national economy, actually improved by $10 billion, down to $57.3 billion for the year. While US manufacturing production largely emerged from Covid-19 shutdowns by late summer, European factories have experienced repeated shutdowns due to successive waves of Covid-19 and highly restrictive policies in many countries.

Our goods deficit with Mexico also hit a new record, at $112.7 billion. The deficit with Mexico increased as companies moved their supply chains out of Asia and closer to home. Passenger cars and trucks, vehicle parts, and computers were the largest categories of imports from Mexico.

The US deficit with Vietnam surged almost 25% to $69.7 billion, making it our third largest deficit country, ahead of Germany and Japan. This is a stunningly bad result for the US since Vietnam is a relatively small and poor nation with a GDP of under $300 billion. Vietnam’s goods exports to the US last year of $79.6 billion were worth more than a quarter of its GDP. By contrast, Germanys $115 billion of exports to the US were less than 3% of its $3.9 trillion GDP. Vietnam benefitted from multinationals moving production out of China, including electronics, household goods, apparel, and furniture. Vietnam also benefited from an undervalued currency, which is now the subject of a USTR investigation. Vietnam is the latest example of a nation with an economic strategy that targets the US consumer for its growth at home. It adds to the pressure of many other Asian nations that have pursued that strategy for decades.

US imports from Switzerland were led by a 14% increase in pharmaceuticals, and a huge increase in imports of nonmonetary gold, related to traders’ financial transactions involving the spot and futures market for gold. Those transactions are related to the Covid pandemic and are unlikely to continue. However, the growth in pharmaceutical imports is a persistent trend. Switzerland uses tax breaks and research grants to lure pharmaceutical companies to establish manufacturing there.

The US had the largest bilateral surpluses with the Netherlands $18.1B, led by exports of pharmaceuticals, crude oil, and medicinal equipment. Our second largest surplus was with Hong Kong $16.1B, led by exports of semiconductors, cell phones and household goods, aircraft (including engines, parts, and equipment), and gem diamonds. The top ten countries with which the US has a trade surplus all experienced declines in the level of the surplus compared with 2019. This is primarily due to production shutdowns to address the spread of Covid-19.

The US had the largest bilateral surpluses with the Netherlands $18.1B, led by exports of pharmaceuticals, crude oil, and medicinal equipment. Our second largest surplus was with Hong Kong $16.1B, led by exports of semiconductors, cell phones and household goods, aircraft (including engines, parts, and equipment), and gem diamonds. The top ten countries with which the US has a trade surplus all experienced declines in the level of the surplus compared with 2019. This is primarily due to production shutdowns to address the spread of Covid-19.

Currency and Exchange Rates

CPA estimates that the dollar is 27 percent higher than its current account balancing level. Persistently large misalignment of the dollar presents a strong headwind for US manufacturers trying to remain competitive with foreign producers.

Figure 2 shows that the trade-weighted US dollar exchange rate rose in the first three months of 2020 and fell thereafter. By year-end, despite being 3.1 percent below its January 2020 level, the dollar was still 10.1 percent higher than it was 15 years ago in January 2006. The full effect of the exchange rate on imports and exports is typically felt after a two-year lag. Indications are that the dollar is now on a slow, multi-year decline but the boost to US production may not be felt until 2023.

Currency misalignment is the larger problem for US producers because it affects our trade with all other nations. However, currency manipulation has recently reemerged as a political issue. In December, the US Treasury said Vietnam and Switzerland met the three conditions in US law to be named currency manipulators. On November 24, 2020, the Department of Commerce preliminarily determined that China’s undervaluation of the renminbi constitutes a countervailable subsidy. It is unclear what action, if any, the Biden administration will take on these issues.

Most economic forecasters see the US economy moving back to strong growth in the second half of 2021, as the nation finally emerges from Covid-19 lockdowns and service sector businesses including tourism and travel get back to normal. The abnormally high savings rates among US households (13% in Q4 2020) suggest that as the economy returns to normal, consumers will go on a spending spree, leading to accelerating imports and an even worse trade deficit. On the other hand, the Biden administration has proposed several policies that could promote reduced imports and higher US manufacturing production, including a Buy American Executive Order, a potential public infrastructure plan, and (to quote national security advisor Jake Sullivan) a “foreign policy for the middle class.” This will be an interesting year.