This article is an expanded version of testimony delivered by Ms. Mayoral to the U.S. International Trade Commission on July 22, 2022.

In his first State of the Union address, President Biden said “When I think about climate change, I think jobs”. I believe the president is correct about the potential opportunities that come with addressing climate change. However, if we are not strategic about our industrial policies, we will be creating foreign and not American jobs-as we have in many industries in the past. The solar industry is giving way to this trend as imports dominate the solar market and force solar firms to lay off workers or shutdown entirely. Removing tariffs will only exacerbate this situation and undermine our energy security needs. Facing issues like climate change, we need to diversify our energy needs and help build a strong renewable energy sector, which includes a resilient end-end solar industry.

In the past few years there has been a series of tariffs placed on solar imports, including Section 301 tariffs on modules from China. This article discusses the combined effect of these policies and the lessons we can learn from the solar experience apply also to other industries and other tariffs.

For reference, recent tariffs affecting solar imports include anti-dumping duties on Chinese solar panel imports, initiated in 2012; Section 201 duties on global imports of solar modules and cells, starting at 30%, levied in 2018; and Section 301 (List 2) tariffs of 25% on Chinese solar modules, initiated in 2018.

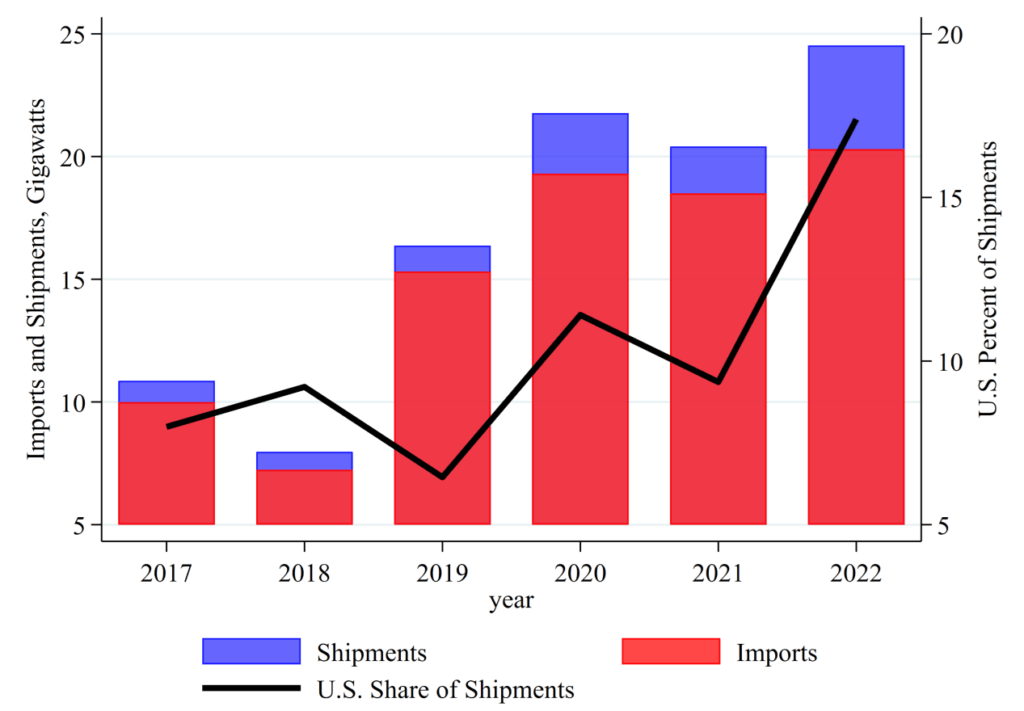

U.S. market share in the solar industry has increased since solar tariffs were enacted

In the past few years, solar tariffs have contributed to the United States’ rising share of the PV module market.[1] Figure 1 below shows the volume of total shipments (which includes imports and exports), a proxy measure of the size of the PV module market, based on federal data from the Department of Energy’s Energy Information Administration (EIA). Figure 1 shows two important facts: first that imports comprise most of the PV module shipments. Second, the U.S. share of these shipments has more than doubled since the Section 201 solar tariffs were put in place. The U.S. share has increased from 7.9% in 2017 to 17.3% in 2022.

Figure 1: Imports, Shipments, and U.S. Share of Shipments of PV Modules

Source: EIA Monthly and Annual Reports on the PV Module Shipments, CPA Calculations, Accessed July 2022

Increased import dependence makes us price dependent, a trend we are seeing during COVID

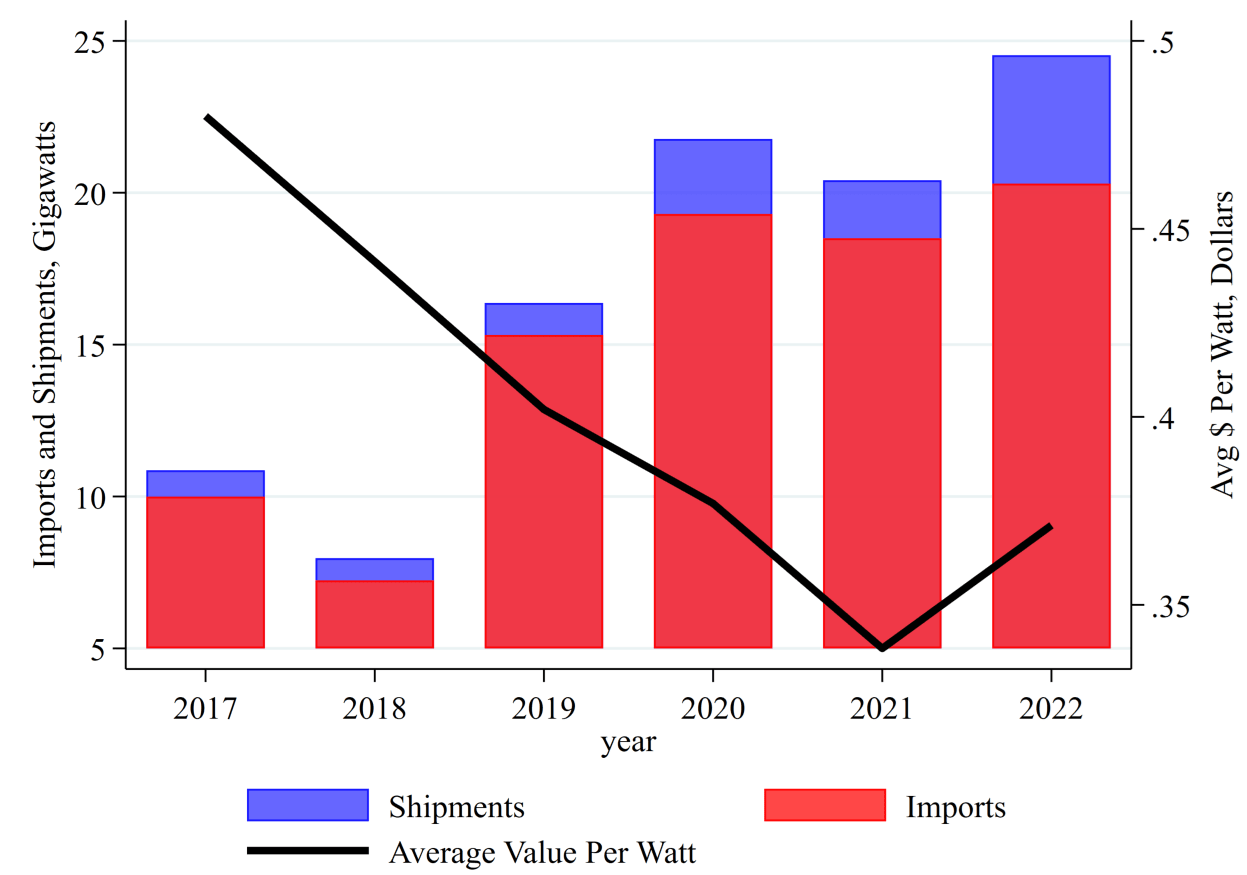

The price per watt of PV modules has declined dramatically over time, due to both increased productivity and increasing imports and production from U.S. firms. The import share of the PV market has increased dramatically from just 9% in 2000 to 87% in 2022. The dominance of foreign suppliers in the PV market leaves the U.S. vulnerable to the behavior of foreign actors. This is not a position the U.S. can afford to take in key markets such as renewable energies.

Our dependence on imports and global supply chains contributed to higher PV module prices in the last twelve months, shown in figure 2 below. Import dependence is a double-edged sword-we accept lower prices, but we also have to accept that we give up some ability to influence our own prices. While we enjoy cheaper prices from higher imports, we also inherently give up control over our ability to increase supply in a crisis.

Figure 2: PV Imports and Prices

Source: EIA Monthly and Annual Reports on the PV Module Shipments, CPA Calculations, Accessed July 2022

While tariffs were beneficial to U.S. firms, they did not inhibit imports, a fact that shows the U.S. has considerable buying power in the solar market

Despite the solar tariffs, imports of PV modules increased but have also comprised a lower share of total shipments as U.S. firms have also increased production. While imports still increased over this period, they likely would have been higher without the tariffs. The solar tariffs did not stop foreign supply, they merely reduced it somewhat.

Tariffs also showed us that the U.S. has considerable buying power in the solar market globally. According to a 2021 USITC report, both domestic and import prices of solar products fell between January 2018 and June 2021.[2] While the USITC report figures were confidential, estimates of the PV module import price indicate a 40 percent decline from 39 cents in Q2 2018 to 28 cents per watt in Q4 2020.[3] The drop in the import price signals that the U.S. has monopsony -like market power with a tariff. In other words, falling import prices implies that the U.S. has the ability to benefit from a tariff in the solar market.

The reliance of U.S. companies on upstream Chinese solar components limits the benefit of tariffs

Developing a U.S. end-to-end supply chain can mitigate supply chain shortages. However U.S. solar companies rely heavily on China and its subsidiaries for the manufacture of solar components. As of 2021, China dominates the global market for these components: polysilicon (72%), ingots (98%), and wafers (97%).[4] China also produces 81% of the world’s supply of solar cells and 77% of solar modules. China’s dominance in the upstream solar industry is a result of the labor and energy intensive requirements of making these components coupled with China’s willingness to mass subsidize/wrongfully source these needs. China relies on slave labor from the Xinjiang province to source about half of its polysilicon needs. [5] Further, estimates show that the Chinese government has invested nearly $50 billion into building its solar industry.[6] Altogether, these advantages make PV manufacturing roughly 30%-40% cheaper in China than the U.S., driven mostly by differences in labor costs.

The reliance of U.S. companies on upstream Chinese solar components limits the benefit of tariffs. The U.S. must develop its own end-to-end supply chain independence by increasing its capacity to produce solar module components or move towards the production of other technologies such as cadmium telluride (CdTe). Currently, most solar energy panels produced globally are crystalline silicon PV modules, which make up 84% of the U.S. market. The remaining production (16%) is the manufacture of CdTe panels.

Conclusions

The issue of tariffs and import dependence is larger than the solar industry. Economic security is national security. And economic security means the U.S. should not be import dependent and by extension price dependent on foreign actors in critical industries, such as renewable energy.

Individual U.S. firms cannot compete against the collective resources of countries like China who provides free land, cheap or slave labor, subsidized loans, major tax breaks and major subsidies. These conditions make U.S. workers compete with slave labor, such as the slave labor camps in the Chinese Xinjiang province. Eliminating tariffs would undermine the current market. Instead, we must use a variety of industrial policies to limit imports and reduce dumping in the U.S.

Facing issues like climate change, we need to build a strong renewable energy sector, which includes a resilient solar industry and supply chain. Tariffs are a necessary but insufficient measure to achieving this. Tariffs should be part of a broader industrial strategy that targets the entire supply chain and focuses on quality rather than just the quantity of jobs.

[1] Jeff Ferry, Reclaiming the U.S. Solar Supply Chain from China, Coalition for a Prosperous America, March 2021

[2] “Crystalline Silicon Photovoltaic Cells, Whether or Not Partially or Fully Assembled Into Other Products”, U.S. International Trade Commission, Publication 5266, December 2021

[3] David Feldman and Robert Margolis, “H2 2020 Solar Industry Update”, National Renewable Energy Laboratory, PR-7A40-79758, April 6, 2021

[4] Solar Energy Technologies Office, “Solar Photovoltaics Supply Chain Review Report”, U.S. Department of Energy, February 24, 2022

[5] “Uyghurs for sale,” Australian Strategic Policy Institute, 2020.

[6] “Solar PV Global Supply Chains”, International Energy Agency, 2022