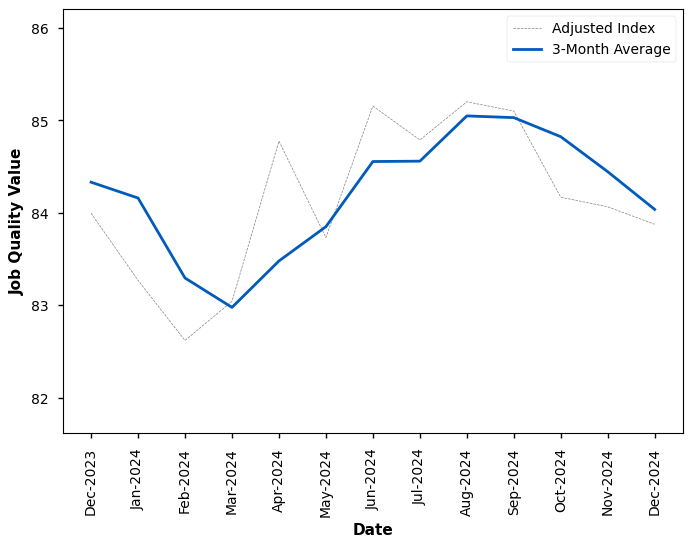

WASHINGTON — The Coalition for a Prosperous America (CPA) today announced that the U.S. Private Sector Job Quality Index (JQI) is now 84.04, down by 0.49% compared to last month. This continues the multi-month JQI decline trend. Meanwhile, the overall January 2025 Jobs Report from the government’s Bureau of Labor Statistics showed 143,000 jobs added in January. This figure is below expectations from most economists, who forecasted 170,000 job gains.

However, most other economic signals in the job report point positively. The jobs gains for the last two months were revised upward with December gains now at 307,000 and November gains now at 261,000. Furthermore, annual wage growth exceeded expectations hitting 4.1%, and monthly wage growth reached a substantial 0.5%, a jump from the 0.3% monthly growth from December. Unemployment also fell slightly to 4.0%.

The January JQI fell substantially again, decreasing by nearly 0.5%. One major reason for this decline is the higher proportion of job gains going into lower income job categories. Six of the top employing low-quality job categories all had December monthly job growth above 0.5%. These include Courier and messenger services (1.29%), Home health care services (0.88%), Traveler accommodation (0.79%), General merchandise retailers (0.64%), Individual and family services (0.56%), and Skilled nursing care facilities (0.51%). This widespread employment growth among many low-wage, low-quality job sectors is not matched by the high-quality jobs sectors.

Only three of the top employing high-quality job sectors had employment growth above 0.5% in December. These include Agencies, brokerages, and other insurance related activities (1.11%), Management, scientific, and technical consulting services (1.08%), and Architectural, engineering, and related services (0.50%). On average, high-quality job sectors saw job gains of only 0.03% while low-quality job sectors saw job gains of 0.28%. A higher proportion of job gains going to lower wage, lower quality sectors has been the primary driver of the falling U.S. Job Quality Index.

We also see echoes of this trend amid manufacturing job sectors. Both high- and low-quality manufacturing job categories saw employment losses in December. However, the losses for high-quality jobs were even greater than the losses for low-quality jobs. The high-quality manufacturing job losses with the most losses are Paper manufacturing (down 0.64%), Computer and electronic product manufacturing (down 0.45%), and Transportation equipment manufacturing (down 0.33%). Gains in other high-quality manufacturing sectors such as Fabricated metal product manufacturing (up 0.37%) and Chemical manufacturing (up 0.27%) were not enough to make up for the losses elsewhere.

Some low-quality manufacturing sectors did see some solid employment gains in December. These include Printing & related manufacturing (up 0.50%) and Textile product mill manufacturing (up 0.41%). However, again, losses elsewhere outweighed any gains. The largest low-quality manufacturing job losses were in Electrical equipment, appliance, and component manufacturing (down 0.95%) and Furniture and related product manufacturing (down 0.51%).

On the positive side, weekly income increased for both high- and low-quality job sectors in December, with wages increases even more for high-quality job sectors. The highest wage growth occurred for Chemical manufacturing (up 1.88%), Paper manufacturing (up 1.22%), and Transportation equipment manufacturing (0.87%). The only high-quality manufacturing job sector with a decline in wages was Nonmetallic mineral product manufacturing (down -0.18%).

Low-quality manufacturing jobs largely had positive weekly income growth in December as well. The largest wage growth occurred in Electrical equipment, appliance, and component manufacturing (up 1.76%) and Printing & related manufacturing (up 1.18%). Meanwhile, the only low-quality manufacturing sectors with wage losses were Textile product mill manufacturing (down 1.34%) and Furniture and related product manufacturing (down 0.17%).

Overall, total wage growth was also positive for both high- and low-quality job sectors. High-quality jobs saw top wage gains in Building equipment contractors (up 1.21%) and Agencies, brokerages, and other insurance related activities (up 1.05%). Meanwhile the wage losses were restricted to Computer systems design & related services (down 0.17%) and Management of companies & enterprises (down 0.15%).

The low-quality job sectors with the largest overall wage gains include Courier and messenger services (up 2.27%), General merchandise retailers (up 2.12%), and Warehousing and storage (up 1.38%). Monthly wage losses for low-quality jobs were restricted to Home health care services (down 1.11%) and Employment services (down 0.33%).

Figure 1. Job Quality Index 1990-2025