Key Points

- With 86 Gigawatts of planned solar module capacity and some 30 Gigawatts of imports, the U.S. market faces huge oversupply of solar modules.

- This will force many U.S. producers out of business, leaving the Chinese-owned U.S. facilities as the last man standing.

- Today, with optimism at its height, Chinese-owned facilities are building more U.S. capacity than U.S. producers. The Chinese lead will only grow as U.S. producers bow out.

- The solution is to reinforce the Inflation Reduction Act tax credits with import quotas and prohibitive tariffs to guarantee rational pricing and a U.S. market dominated by U.S. producers.

The U.S. solar module manufacturing industry is heading for disaster. Although demand and installations are rising steadily, imports are rising much more quickly. And under the stimulus of the Inflation Reduction Act, domestic production is surging to unprecedented levels. The result will be a solar power apocalypse, in which dozens of companies go bankrupt and/or sell off their businesses. The lucky ones will be the ones that scale down their plans quickly and avoid taking on too much debt.

The cutbacks and bankruptcies have already begun. After reporting a $36 million loss on just $29 million of quarterly revenue, California solar installer Sunworks filed for bankruptcy and is now being liquidated. SunPower, an installer and one of the early developers of solar cells announced an eye-watering loss of $247 million for 2023, raised an emergency $175 million loan from its French parent TotalEnergy, and brought back its previous chairman Tom Werner to help save the company. Finally, Cubic PV announced last month that it was abandoning plans to produce solar wafers in the U.S. and instead would concentrate on solar modules. Trailblazing innovator Cubic was America’s best hope to break the Chinese stranglehold on solar wafers, but catastrophic price declines throughout the solar supply chain led Cubic’s investors to cancel the wafer project.

The likely outcome of all this upheaval could well be an increased Chinese stranglehold on a global market that China already dominates.

For several years we have argued that U.S. self-sufficiency in solar energy can only be achieved if the U.S. has access to every step of the supply chain from suppliers inside the U.S. or at least outside of China. Independent evidence shows that in recent years, China has steadily increased its dominance in each step in the supply chain from its already-high levels a decade ago. In a recent report, the International Energy Agency, a body normally given to cautious consensus statements, said bluntly:

“Global solar PV manufacturing capacity has increasingly moved from Europe, Japan and the United States to China over the last decade. China has invested over USD 50 billion in new PV supply capacity – ten times more than Europe – and created as many as 300 000 manufacturing jobs across the solar PV value chain since 2011.”[1]

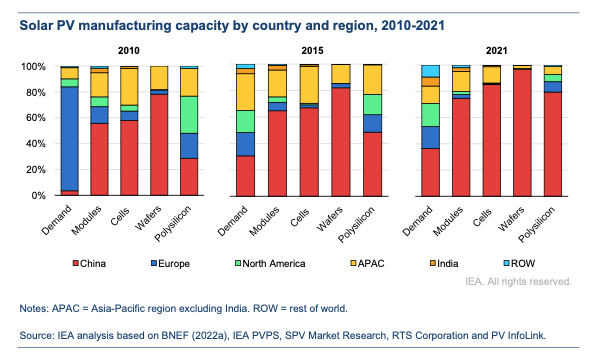

Figure 1 below, taken from the IEA report, shows China’s rising dominance in the supply chain. Its dominance in the crucial segment of solar wafer manufacturing is near-total. Meanwhile, China’s domestic economic problems have led the Chinese Communist Party (CCP) to redouble its focus on exports. Today most solar modules imported into the U.S. start off as solar cells manufactured in China from solar wafers made in China. The cells are then shipped to Southeast Asia where they are assembled into modules and then shipped to the U.S.

Table 1 shows the rise in imports of solar modules. Last year, module imports doubled to $18 billion. The Trump tariffs of 2018 depressed imports, but they skyrocketed in 2022 and 2023. Last year, imported solar modules paid an effective tariff rate of just 0.4%. The bifacial exclusion, which made two-sided solar modules exempt from tariffs, followed by President Biden’s two-year “pause” on certain solar tariffs announced in June 2022, has led to a surge in imports.

Table 1. Solar module imports almost doubled last year to record level of $18.6 billion.

| Annual solar module imports | ||||

| Year | Imports $B) | YoY % change | Duties Paid ($M) | Effective Duty Rate |

| 2009 | $ 1.242 | 0 | ||

| 2010 | $ 2.315 | 86.3% | 0 | |

| 2011 | $ 4.489 | 93.9% | 0 | |

| 2012 | $ 4.846 | 8.0% | 0 | |

| 2013 | $ 3.578 | -26.2% | 0 | |

| 2014 | $ 4.108 | 14.8% | 0 | |

| 2015 | $ 5.938 | 44.6% | 0 | |

| 2016 | $ 8.169 | 37.6% | 0 | |

| 2017 | $ 5.087 | -37.7% | 0 | |

| 2018 | $ 2.872 | -43.5% | $ 256.2 | 8.9% |

| 2019 | $ 5.727 | 99.4% | $ 670.4 | 11.7% |

| 2020 | $ 7.855 | 37.2% | $ 683.2 | 8.7% |

| 2021 | $ 6.308 | -19.7% | $ 602.9 | 9.6% |

| 2022 | $ 9.552 | 51.4% | $ 120.8 | 1.3% |

| 2023 | $ 18.608 | 94.8% | $ 77.4 | 0.4% |

| Source: US Census | ||||

In August 2022, the Inflation Reduction Act was signed into law. The solar power sections of the Act provided for tax credits to manufacturers building out each segment of the solar supply chain, a very positive move. The tax credits unleashed a huge wave of investment in new solar manufacturing facilities. We counted some 40 companies announcing investment plans for solar module production, either greenfield sites or expansion of existing sites. The output when all these plants come onstream in two years or so will be some 86 Gigawatts (GW) of modules.

Last year’s imports of $18 billion are likely to represent some 30 GW of solar modules. Imports are likely to continue to rise, but if we assume for the moment they stay flat, then total U.S. annual supply would be 116 GW.

On the demand side, data from Wood Mackenzie and the solar trade association SEIA show that last year, the U.S. installed 33 GW of solar modules. This year, they project a rise of 10% to installations of 36 GW. WoodMac and the SEIA tend to be perennial optimists, driven by their convictions that they are saving the planet, while also making good money for their solar installer members and persuading bankers to finance solar installations, since the industry is heavily dependent on credit.

But even if we allow ourselves to be still more optimistic than those commentators, and assume as much as 40GW of installations this year, followed by 10%-15% increases each year thereafter, we still confront a situation in which total supply will be more than double total demand for several years to come.

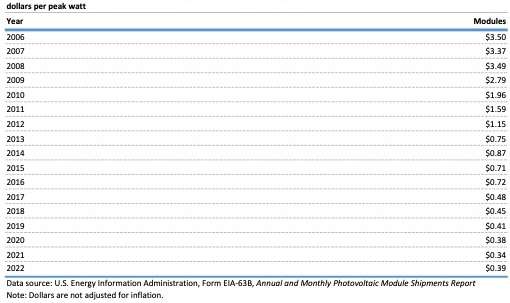

With such huge oversupply, and given China’s continuing investment in production and export well beyond its own domestic needs, the market price per watt for modules must continue to fall. Table 2 shows that module prices have fallen by more than 50% since 2016, to 39 cents a watt as of 2022, the last year for which the Department of Energy’s Energy Information Agency has published data. Reports from manufacturers suggest modules are today attracting prices in the 30 cents per watt range. At that price, it is very hard for a U.S.-based solar module producer to make a profit.

Figure 1. China’s share of global supply has increased steadily in modules, cells, wafers, and polysilicon. Its dominance in solar wafers is almost total.

Our analysis of planned solar module manufacturing facilities found that Chinese-owned companies are planning to build more U.S. facilities, in terms of Gigawatts of capacity, than U.S.-owned companies. On announced plans, Chinese-owned companies will account for 31 GW or 35.9% of the total planned U.S. production capacity of 86 GW, as compared to 29 GW or 33.8% for U.S.-owned companies. Chinese solar module leaders like Longi and Trina are building larger, multi-gigawatt facilities, while U.S.-owned companies like Mission Solar or Canadian companies like Heliene are building facilities with capacity of 1 GW or less.

In most cases, construction of the new or expanded facilities has already begun. If the price paid for solar modules continues to fall this year and next, U.S. companies will either cancel their plans or try to exit the business by selling their completed money-losing facilities. In many cases, the buyer is likely to be a Chinese producer, further increasing China’s dominance of the U.S. solar manufacturing industry. U.S. investors demand a competitive return on investment. Chinese manufacturers on the other hand are backed by Chinese banks, and behind them the CCP, which enables them to stay in business through years of losses. Global solar energy dominance is an objective of the CCP, enshrined in the Made in China 2025 plan and other five-year plans.

Today, the only multi-gigawatt producers on U.S. soil are First Solar and Hanwha Q Cells. On current trends, in a. couple of years the list will include Chinese majors Trina, Longi, Jinko and Canadian Solar.

Table 2. The U.S. price per watt for solar modules has fallen 46% since 2016.

Table 3. Announced expansion plans show China leading

in solar module production facilities on U.S. soil.

| Ownership | Capacity (GW) | As percent of total planned capacity |

| USA | 29.09 | 33.8% |

| China | 30.95 | 35.9% |

| India | 8.5 | 9.9% |

| Canada | 2 | 2.3% |

| Korea | 5.1 | 5.9% |

| Europe | 9 | 10.4% |

| Cambodia | 1.5 | 1.7% |

| Total | 86.14 | 100.0% |

| Source: Company press releases | ||

Accelerate Investment and Competition with Import Quotas

The present system is not working. Every solar module producer we speak to is worried stiff about declining prices and doubtful future profitability. The IRA has stimulated investment but even billions of dollars of tax credits are not sufficient on their own to build a healthy industry. A number of reforms can transform the current environment into one that can build a healthy, profitable, U.S.-owned solar manufacturing industry.

- Modify the IRA so Chinese-owned companies cannot claim tax credits.

Today, the U.S. taxpayer is paying Chinese companies to build facilities in the U.S. and extend and reinforce China’s global monopoly. In China, no U.S. company is permitted to build and operate solar module facilities, let alone getting Chinese government money to do so. This is an absurd situation. Congress should rectify this immediately by modifying the IRA to exclude all Chinese companies from eligibility for the tax credits. On the other hand, other foreign companies should not be excluded. Korean, European, and Japanese companies bring more competition, valuable capital dollars, and in some cases technological innovation which can make the U.S. industry stronger and more innovative.

- Implement import quotas to manage imports to a sensible level.

Last year’s imports could have supplied close to 100% of the U.S. market. With the vast oversupply produced in China and Southeast Asia, and Chinese companies’ ability to drive prices down, there is little scope to build a sustainable U.S. industry. Chinese companies could easily drive prices down to half the 50 cents to 60 cents level which U.S. companies tell us is needed for a profitable U.S. industry.

Given global oversupply and the control Chinese majors exert over global module prices, neither tariffs nor tax credits at any reasonable level can rebuild a healthy U.S. market. But import quotas, with hard volume limits on imports, can. Here is an illustration of how quotas could work: our estimate, based on SEIA data, is that of this year’s likely 36GW of solar installation, some 10GW will come from U.S. sources and 26GW will be imported. To avoid disruption of the market, this year’s quota could start at 26GW. It would fall by 5GW each year thereafter, until reaching a desired final state. Imports worth 10% to 20% of the market might be reasonable as a final state. But growth in U.S. production of 5GW per year will enable the industry to invest and grow in sustainable fashion. The annual decline in the quota should be set after consultation with the U.S. industry, to gain assurance that the industry can and will step up production at a rate sufficient to meet market demand as the quota falls.

- Set a price floor for solar modules.

The pressure of global oversupply should not be underestimated. Chinese companies will begin planning ways to circumvent import quotas from the moment they catch wind of the idea. The U.S. can use the IRA to enforce a price floor, in other words companies found to be selling below the floor lose access to the tax credits in that year. The minimum price could be 50 to 60 cents a watt, although it should be set after consultation with the major U.S.-based producers and buyers of solar modules.

An interesting idea would be to build an annual price reduction into the price floor. The reduction could be 5% per annum. Given U.S. inflation of 2%, this amounts to an annual 7% reduction in the cost of modules in real (inflation-adjusted) terms. This is a reasonable reduction in price and cost and manufacturers could build it into their plans and continue to invest, make a profit, and expand their businesses.

It should be borne in mind that modules are only about a quarter of the total cost of a solar installation. Solar installs are in the range of $2 a watt for utilities to $3-$3.50 a watt (or more) for residential home installs. So the price of the module is actually a relatively minor factor in the overall cost, and stable module prices will have little effect on the speed with which a utility can build its solar capacity. They may even simplify a solar investment plan by allowing utilities to build a more rational multi-year planning process.

- Public institutions should be required to buy U.S. solar modules

Schools, military bases, VA hospitals, government offices, and other public buildings should be required to buy only U.S.-produced solar modules and if they buy power from power producers, it should be produced from U.S. solar modules. Creating a stable, rational solar power industry is so important that the public sector should do its part to support the U.S. industry.

This plan can be put into place using Section 232 tariffs, which the president can implement by executive proclamation. The quota would be effected through a tariff rate quota (TRQ). The TRQ would specify that in Year One, the first 26GW of imports would come in with a small tariff (say 25%) and any modules above that level would attract a 400% tariff—effectively a quota. In Year Two, the first tranche of low-tariff imports would fall to a limit of 21GW, with all imports above that attracting the 400%. And so on.

This plan would not only restore order to the solar module market. It would also create profitable customers for the upstream manufacturers, including solar wafers, solar cells, and polysilicon. I would expect that investors would quickly emerge in those businesses once they became confident that their downstream module-making customers had viable businesses.

Critics will say this is not a free market. But the choice is not between a free market and an un-free market. The choice is between a market controlled by the Chinese government and a rational, U.S.-based industry that has some degree of insulation from China’s domination of the solar manufacturing industry. For those who doubt the seriousness of China’s intentions, the size of China’s 2023 trade surplus, $823 billion, the second year running with surpluses over $800 billion, should convince them of China’s determination to dominate world markets in all goods it considers strategic.

The steady growth in demand for solar modules over the next several years and predictable costs in the bill of materials will make such a plan more viable than in commodity-oriented industries. The benefits of the plan are first, a guarantee of U.S. autonomy for an industry and a resource—solar power– that everybody agrees will play a large and increasing role in U.S. energy generation over the next several decades. The plan will also create thousands of good jobs in solar power manufacturing. It will reinvigorate U.S. technological innovation in this industry, which has been in a prolonged slump since China first set out to wipe out the U.S. and European industries.

[1] International Energy Agency, Special Report on Solar PV Global Supply Chains, August 2022, pg. 7.