- We are moving to a quarterly cadence for our Currency Misalignment Monitor.

- The Monitor tracks currency misalignment based on latest monthly exchange rates

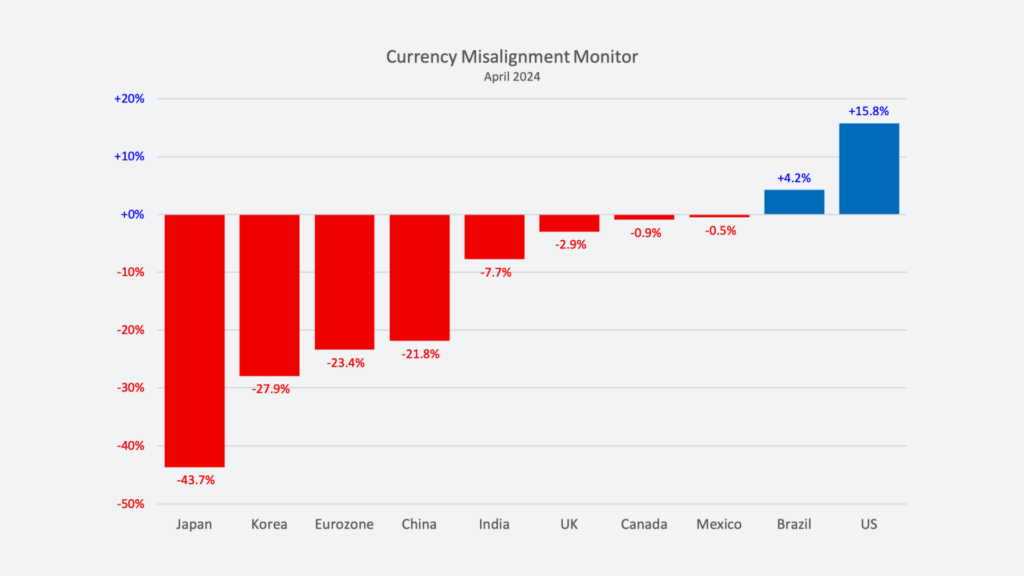

- Dollar overvaluation has moderated slightly since last December, but the greenback remains the most overvalued major currency, at 15.8% above equilibrium value.

- Japanese yen continues hugely undervalued, at 43.7%.

- Chinese yuan undervaluation reaches 21.8%, as China’s central bank allows the yuan to slide to counteract weakening Chinese economy.

The April Currency Misalignment Monitor shows that the dollar continues to be heavily overvalued and major Asian currencies remain undervalued. Standard economic theory requires exchange rates to be close or at least tending towards the values that put their current accounts into balance. That allows for fair international competition and maximization of global output. The overvalued dollar makes imports less expensive in the U.S. and our exports more expensive on world markets. Our overvalued currency is the biggest single contributor to our large trade and current account deficits. Last year, the U.S. trade deficit was $779.8 billion, while the current account deficit was even larger, at $818.8 billion (equivalent to 2.99% of U.S. gross domestic product).

In recent months, the dollar has edged down as financial markets grew more convinced that sometime this year, and perhaps as soon as June, the Federal Reserve will begin reducing interest rates. Lower U.S. interest rates reduce the yield on dollar assets, including Treasury debt, money market funds, and other dollar-denominated assets. Lower yields prompt international investors to reduce dollar holdings and shift into other currencies. However, the U.S. is enjoying stronger economic growth than other major economies, which tends to attract investment into dollar-denominated assets, somewhat offsetting the effect of declining dollar yields.

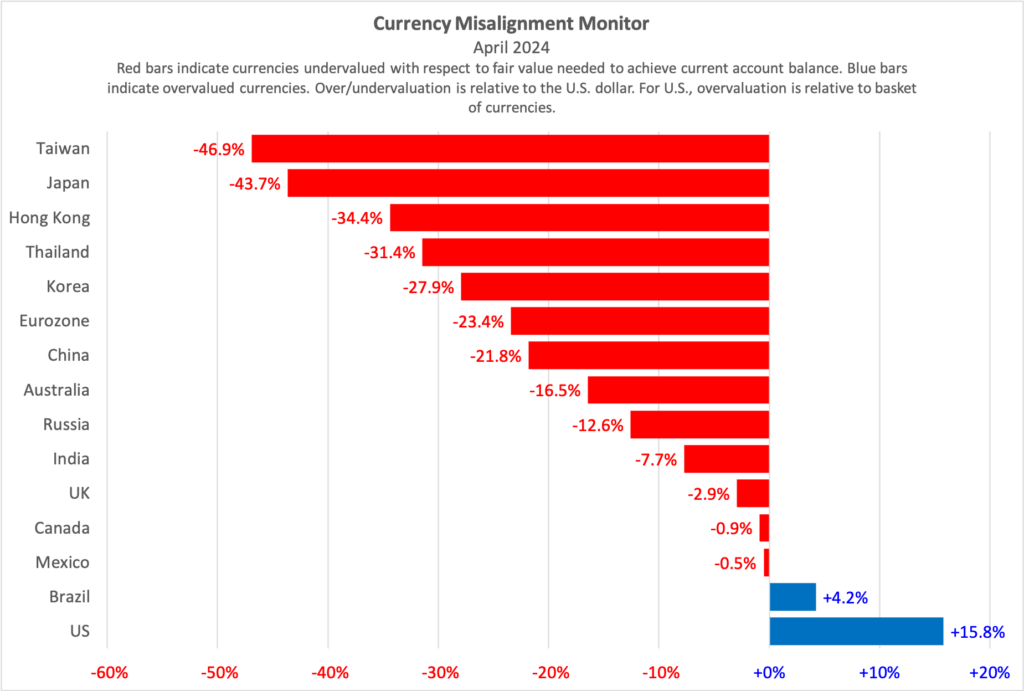

The major Asian currencies are substantially undervalued, reflecting the fact that they are running persistently large current account surpluses. Our model estimates equilibrium or fair value for a currency by adjusting all currencies to lead to balanced current accounts (i.e. reducing both surpluses and deficits to as close to zero as possible) five years out, i.e. by 2028. Japan’s undervaluation, at 43.7%, is huge because the model indicates Japan’s currency would have to rise by 43.7% against the dollar to generate a balanced current account in 2028, based on the IMF forecasts of the world economy in 2028.

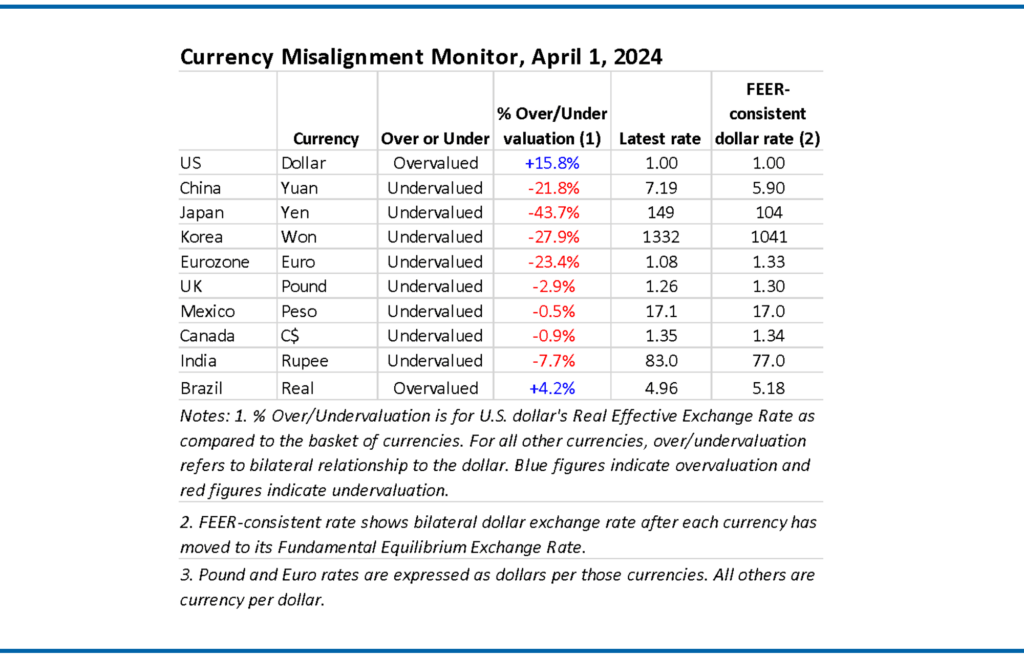

China’s undervaluation, at 21.8% is large too. The model shows that the yuan, which has been hovering around 7.20 to the dollar recently, should rise to 5.90 to the dollar to balance China’s current account. However, this may be an underestimate of China’s undervaluation. The IMF forecasts that China’s current account surplus will be just 0.6% of China’s GDP in 2028. That forecast now looks very conservative. Before the Covid pandemic, China’s trade surplus was running at between $200 billion and $300 billion. In the last two years, as China’s economy has slowed down, Xi Jinping’s Communist government has pushed hard to raise China’s exports, resulting in a $823 billion trade surplus in 2023. This huge increase in the trade surplus will inevitably raise the current account surplus. Modeling current Chinese policies’ impact on the exchange rate would indicate the need for an even more substantial increase in the yuan to dollar rate to bring China’s accounts closer to balance.

Table 1. Currency valuations from the Currency Misalignment Monitor, April 2024

The CMM is based on a mathematical model in which 34 major currencies all move simultaneously to bring global current accounts into balance over a five-year time horizon. If the dollar had to move on its own, the dollar would need to move by approximately twice as much, or around 25%, to achieve fair value for the U.S. economy, i.e., a value that eliminated the current account deficit. The current account deficit is dominated by the trade deficit, but also includes some other financial flows into and out of the U.S.

METHODOLOGY

The Currency Misalignment Monitor is based on pioneering work done by William Cline at the Peterson Institute for International Economics. The Cline model, also known as SMIM for Symmetric Matrix Inversion Method, uses IMF forecasts for current account balances for 34 nations to derive a simultaneous solution for all exchange rates that will minimize national current account balances, including surpluses and deficits. The CMM uses this methodology. However, the Cline version sets a target of plus or minus 3% of GDP for each nation’s current account. We believe this is too flexible for a properly functioning global trading system. Our model sets a target of 0% current account balance for each nation. Most nations do not achieve 0% in year five, but the model seeks to get them as close to zero as possible and in so doing gives us a realistic sense of each currency’s over or undervaluation.

Note also that this methodology is dependent on IMF forecasts, which currently run from 2023 data out to 2028. The IMF has a history of optimism, including for example expectations that the U.S. current account deficit and the China surplus will both contract over time. If those forecasts turn out to be over-optimistic, then the misalignment estimates in the Monitor could well be understated. Nevertheless the Cline SMIM model is an innovative method for incorporating a large amount of global data into a single model.

The Currency Misalignment Monitor (CMM) is published in partnership between the Coalition for a Prosperous America (CPA) and the Blue Collar Dollar Institute (BCDI).