KEY POINTS

- USD Overvaluation affecting U.S. trade with the world by $364 billion, compared to only a $30 billion effect from current tariffs.

- Currency misalignment also has a larger effect in more heavily tariffed countries, such as China.

- The effective rate of U.S. tariffs with the world is only 2.3%, compared to a USD overvaluation of 16.9%.

- USD value compared to other currencies increased 12% since 2021.

- The increasing overvaluation of the USD

Effect of Current USD Misalignment Far Outweighs the Effect of Tariffs

The latest CPA Currency Misalignment Monitor for July 2024 found that the U.S. Dollar (USD) is overvalued by 16.9%, based on the latest monthly exchange rates. This overvaluation of the USD provides a hidden subsidy for importing goods into the United States. The overvaluation also essentially puts a tax on U.S. exports. Due to the higher value of the USD, U.S. goods are more expensive and consequently less competitive in foreign markets.

The total value and effect of this USD misalignment (both in the form of the import subsidy and export tax) is grossly underestimated. Tariffs are seen as one of the primary tools for policymakers to address trade issues, but even all the U.S. tariffs combined do not compare to the impact that the currency misalignment is having.

As shown in Figure 1, in the first five months of 2024, the United States has collected $30 billion in customs duties from tariff programs (both general customs duties and tariffs introduced to protect U.S. economic security, i.e. Section 201, 232, and 301). However, this $30 billion tax on imports to help protect domestic production is far outweighed by the effect of the USD overvaluation. The USD overvaluation effect has amounted to $220 billion in import subsidies and $144 billion in export penalties ($364 billion total) for January 2024 through May 2024.

Figure 1:

The data from 2023 shows the same trend. The total effect of the USD misalignment in 2023 vastly outweighs current U.S. tariff levels. It also harms U.S. industries from trade in both directions, making imports cheaper and U.S. exports more expensive abroad.

Currency Misalignment Dominant Even in More Heavily Tariffed Countries

Even when looking at U.S. trade with China (which is most affected by recent U.S. tariff increases, i.e. Section 301), the USD misalignment effect far outweighs the tariff impact. From January 2024 through May 2024, the United States imposed $18 billion in import tariff duties against Chinese goods. Nonetheless, the USD overvaluation import subsidy amounts to nearly $28 billion during the same time period, and the export penalty amounts to $10 billion (a total trade distortion of $38 billion compared to just $18 billion in tariffs).

Figure 2:

This data shows that tariffs can still have a strong effect and compete to help correct the effect of currency misalignment. However, even after the increased tariffs against China with Section 301, USD overvaluation still has more of an impact and still outweighs the effect of current tariffs.

Chinese Renminbi (RMB) Undervaluation Subsidizing their Export Dominance

In addition to the USD’s overvaluation, CPA’s Currency Misalignment Monitor also shows that China’s currency is extremely undervalued. The report shows that China’s RMB is currently undervalued by 25.8%. China’s RMB is even more undervalued than the USD is overvalued. Naturally, this not only effects U.S. trade with China, but also subsidizes China’s trade with the rest of the world.

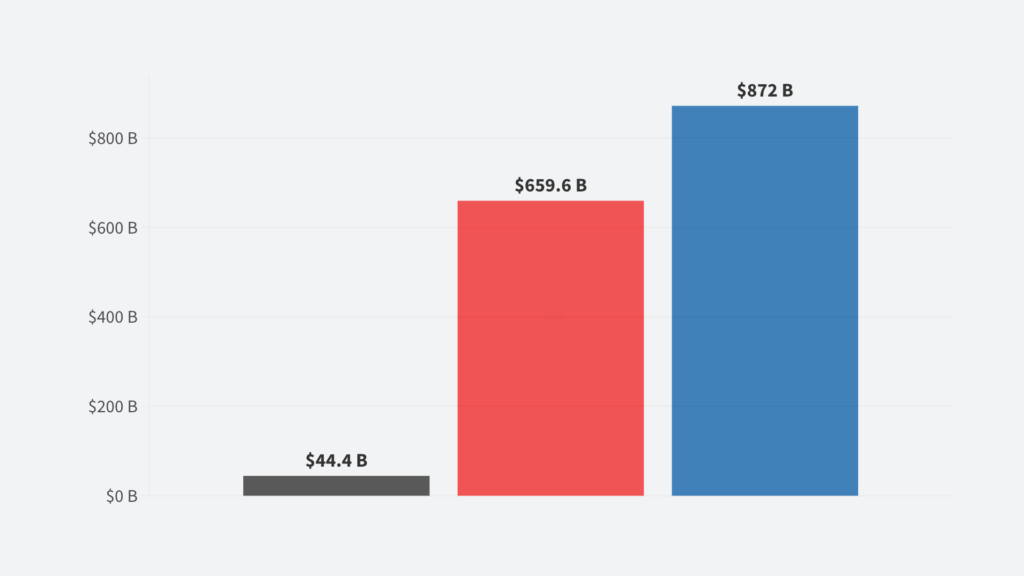

As shown in Figure 3, the 25.8% undervaluation of the Chinese currency gave the country’s industry a $872 billion export subsidy in 2023. Furthermore, it also helped keep out competition from the Chinese market with the undervalued RMB putting a $659.6 billion tax on imports, making those goods more expensive to compete in the Chinese market.

Figure 3:

The effect of China’s RMB undervaluation is massive compared to the United States’ efforts to counter Chinese trade dominance through Section 301 tariffs so far. The Section 301 tariffs have had some effectiveness in diverting trade to the U.S. and encouraging a more diversified supply chain. However, in 2023, the total value of U.S. tariffs against China amounted to $44 billion (5% of the total value of the RMB’s export subsidy effect). The effect of currency misalignment on trade cannot be understated and current tariff levels are nowhere near sufficient to address the issue.

The United States’ Effective Tariff Rate with the World Only 2.3%

The effect of the currency misalignment is so strong because it affects all goods being imported and exported to and from the United States. U.S. tariffs usually only affect specific goods and only from particular countries. For example, Section 301 tariffs apply only to China and only cover about half of Chinese goods. Section 232 duties, meanwhile, apply only to steel/iron and aluminum products, and several countries have negotiated exemptions from the tariff. The U.S. also has many negotiated free trade agreements that reduce tariffs with countries across the world. Furthermore, most current tariff rates that are in effect do not even make up for the currency misalignment for the covered product. For example, the Section 232 tariff on aluminum at 10% does not make up for the 16.9% undervaluation of the USD.

The result of this limited coverage of current tariffs results in the United States only having an effective tariff rate of 2.3% against the world and an effective tariff rate of 11.1% against China. This effective tariff rate is based on the total tariffs imposed on imported goods compared to the total goods value entering the United States.

Conversely, the USD misalignment applies to all goods since the USD’s value is an unavoidable part of conducting trade with the United States, and the scale of the current USD overvaluation at 16.9% far exceeds the effective tariff rate.

USD Overvaluation Worsening

This USD overvaluation problem has grown significantly over the past 15 years. As shown in Figure 4, there has been a long-term trend appreciation trend of the USD, especially since 2014. Overall, the Federal Reserve’s U.S. Dollar index (which measures the value of the USD compared to other countries’ currencies over time) is up 34% from 2010 levels. This USD overvaluation issue is becoming increasingly more intense with appreciation continuing into 2024. Since just 2021, the USD Index has risen 12%.

Figure 4:

As the USD continues to become more overvalued, foreign goods and imports will become increasingly cheaper compared to domestic U.S. goods, and U.S. exports will become increasingly less competitive in foreign markets. This will result in losses in the U.S.’s domestic market share and a loss in shares of key export markets.

Conclusion

While tariffs, quotas, and other trade policies remain essential tools to protect U.S. jobs, domestic production, and economic security, the importance of the effect of the USD’s overvaluation cannot be underestimated. The increasing overvaluation of the USD increasingly discourages U.S. production, U.S. jobs, and U.S. industries. This growing issue affects U.S. trade even more than current U.S. tariff levels and affects all goods both imported and exported to/from the United States. If this issue remains unaddressed, it will continue to severely undermine U.S. economic security as the country is continuously priced out of its own domestic production, industry, and jobs.

1. U.S. Census. “USA Trade Online,” n.d. https://usatrade.census.gov/.

2. “Nominal Broad U.S. Dollar Index,” July 1, 2024. https://fred.stlouisfed.org/series/DTWEXBGS.