To Reduce the Deficit, Tariff the Money

IDEA IN BRIEF

America’s record $1.3 trillion trade deficit persists despite the highest tariff rates in generations because tariffs target the wrong side of the ledger. Under the balance-of-payments identity, every dollar of trade deficit is matched by a dollar of net capital inflow—meaning the deficit is not a goods problem but a capital problem, driven by export-driven economies recycling their excess savings into U.S. financial markets. As foreign ownership has rotated from stable Treasury holdings toward valuation-sensitive equity, rising U.S. stock prices now automatically expand foreign claims on American corporate earnings, deteriorating the national balance sheet independently of trade flows and concentrating the gains of market appreciation among capital holders while adjustment costs fall on workers and industrial communities. A durable solution requires moving beyond tariffs on goods to address the capital account directly—tariffs on the money.

KEY FINDINGS

- Tariffs alone are not likely to eliminate the U.S. trade deficit. The most persistent driver of America’s unsustainably high trade deficits is foreign investment in the United States. Without addressing the savings–investment imbalance financed by foreign capital, tariffs alone cannot reduce the aggregate deficit.

- Globalization worsened the U.S. current account balance. By maintaining open capital and trade markets, the United States became the world’s consumer of last resort, absorbing excess savings from export-driven economies. As those countries invested their savings in U.S. stocks and bonds, the resulting inflows financed persistent trade deficits and shifted economic activity toward financial markets rather than domestic production.

- The composition of U.S. capital inflows has changed. Foreign investment has shifted from stable reserve-driven bond holdings toward valuation-sensitive equity ownership, increasing the vulnerability of the U.S. external balance sheet and expanding foreign claims on future American earnings.

- Persistent capital inflows have widened inequality. Deficits financed through asset markets inflate financial wealth, which is highly concentrated domestically and increasingly owned abroad, while tradable-sector employment and production decline.

Introduction

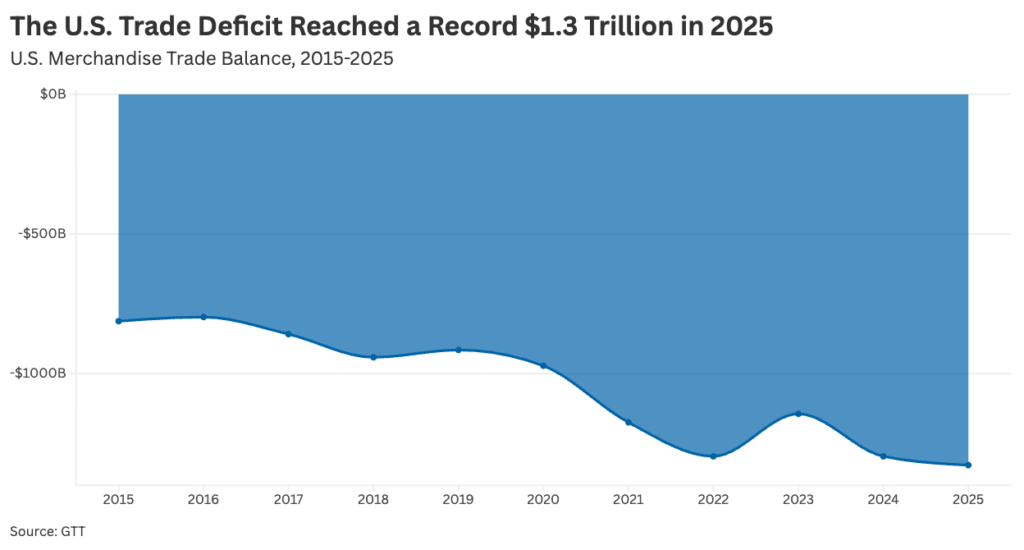

Tariffs are often described as a tool for reducing the trade deficit. It is therefore understandable that the latest data—showing a record $1.3 trillion U.S. goods trade deficit in 2025 despite the highest effective tariff rate in generations (Figure 1)—has led some observers to question their effectiveness.

FIGURE 1

But before treating this as an indictment of tariffs, it is important to clarify what tariffs can and cannot do.

Tariffs remain an essential tool for defending national security and shielding strategic industries from mercantilist cheating. They also correct distorted relative prices created by state-subsidized foreign overcapacity, redirecting capital toward domestic production and reducing the incentive to channel global surpluses into U.S. financial markets. But tariffs alone do not address the macroeconomic forces that sustain the overall trade deficit.

The reason is simple: a country’s trade balance reflects the gap between what it saves and what it invests. When national investment exceeds national saving, the difference must be financed from abroad. That financing shows up as foreign purchases of U.S. assets—stocks, bonds, businesses, and real estate. In accounting terms, that capital inflow is the mirror image of the trade deficit; every dollar used to buy an import will return back to the U.S. as either a purchase of a “good” or an “asset,” otherwise known as foreign capital.

The U.S. trade deficit is often framed as the excess of imports over exports, reckless Americans living beyond their means. But that mistakes cause with effect; our trade deficit is not the result of excess American consumption, it is the result of U.S. trading partners pushing their excess savings into U.S. financial markets.

To meaningfully address the trade deficit, the United States needs to move beyond tariffs on goods to “tariffs on the money,” using capital-side tools to moderate the inflows creating our unbalanced trade.

The Balance of Payments: A Primer

All economic transactions between residents and the rest of the world are recorded in a country’s balance of payments (BOP). Within that system, three measures are especially important:

1) the current account (CA)—which tracks the flow of goods, services, and income across borders, and reflects the difference between what a country earns and what it spends. When a country spends more than it earns, it is running a current account deficit (i.e. a savings shortfall that must be financed from abroad), and

2) the financial account—which records how that financing occurs, through foreign purchases of domestic assets such as stocks, bonds, businesses, and real estate. When the United States runs a current account deficit, the financial account must show an equal and offsetting inflow of foreign capital. These two accounts are mirror images of each other by accounting definition:

Trade Deficit ≅ Net Capital Inflows

3) the net international investment position (NIIP)—the difference between the U.S.-owned foreign assets and foreign-owned U.S. assets. A negative NIIP means foreign investors hold more claims on U.S. assets than Americans hold abroad. When the United States runs a trade deficit, foreign investors finance it by acquiring U.S. assets, which over time accumulates as a deteriorating NIIP.

Globalization Breaks the Postwar System…

The era of globalization represented a distinct break from the postwar, “Bretton-Woods” system. During the 1950s and 1960s, international capital flows were constrained by capital controls. Financial markets were smaller, cross-border portfolio flows were limited, and governments retained greater autonomy over domestic economic policy. Capital was effectively embedded within national economies, subject to domestic taxation and political compromise.

Under the Bretton-Woods framework, external deficits and surpluses were more tightly managed, and growth in advanced economies was accompanied by comparatively broad income gains. Capital controls limited the ability of investors to rapidly shift funds across borders, which reduced the pressure on governments to compete for mobile capital through lower taxes or weaker labor protections.

In contrast, the globalization era was characterized by three pillars: privatization, open capital accounts, and trade liberalization. The United States opened both its goods and capital markets under the assumption that global integration would promote shared prosperity.

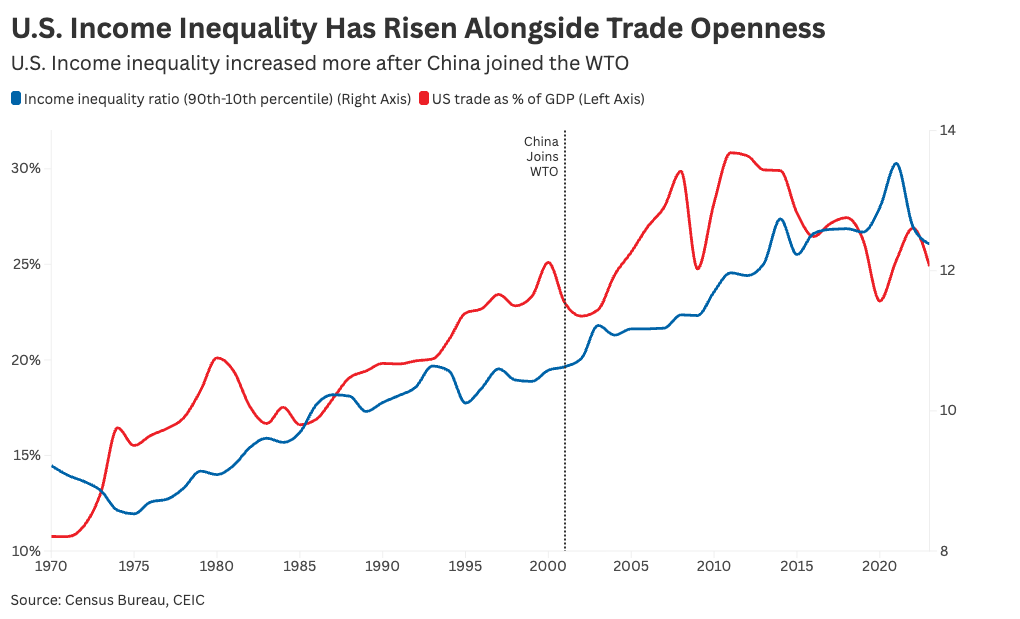

While this model succeeded in expanding the global financial sector and facilitating cross-border investment flows, it coincided with rising income inequality and the steady deterioration of the U.S. external position (Figure 2).

FIGURE 2

…and worsened the U.S. current account balance

The most notable consequence of the globalization era was a worsening of the U.S. current account balance. While the United States maintained open capital markets, major surplus economies such as China, Germany, and Japan pursued export-led growth strategies that suppressed domestic consumption. These strategies relied on wage restraint, industrial subsidies, managed exchange rates, and in some cases capital controls. The result was persistent current account surpluses abroad and corresponding deficits in the United States.

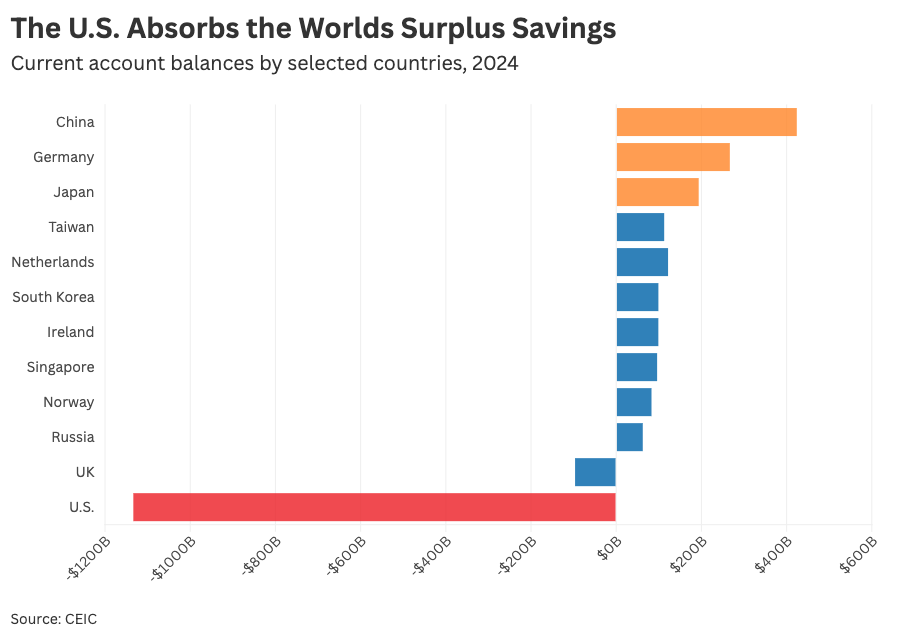

As shown in Figure 3, major surplus saving economies such as China, Germany, and Japan run persistent current account surpluses, which the U.S. absorbs in the form of the world’s largest deficit.

FIGURE 3

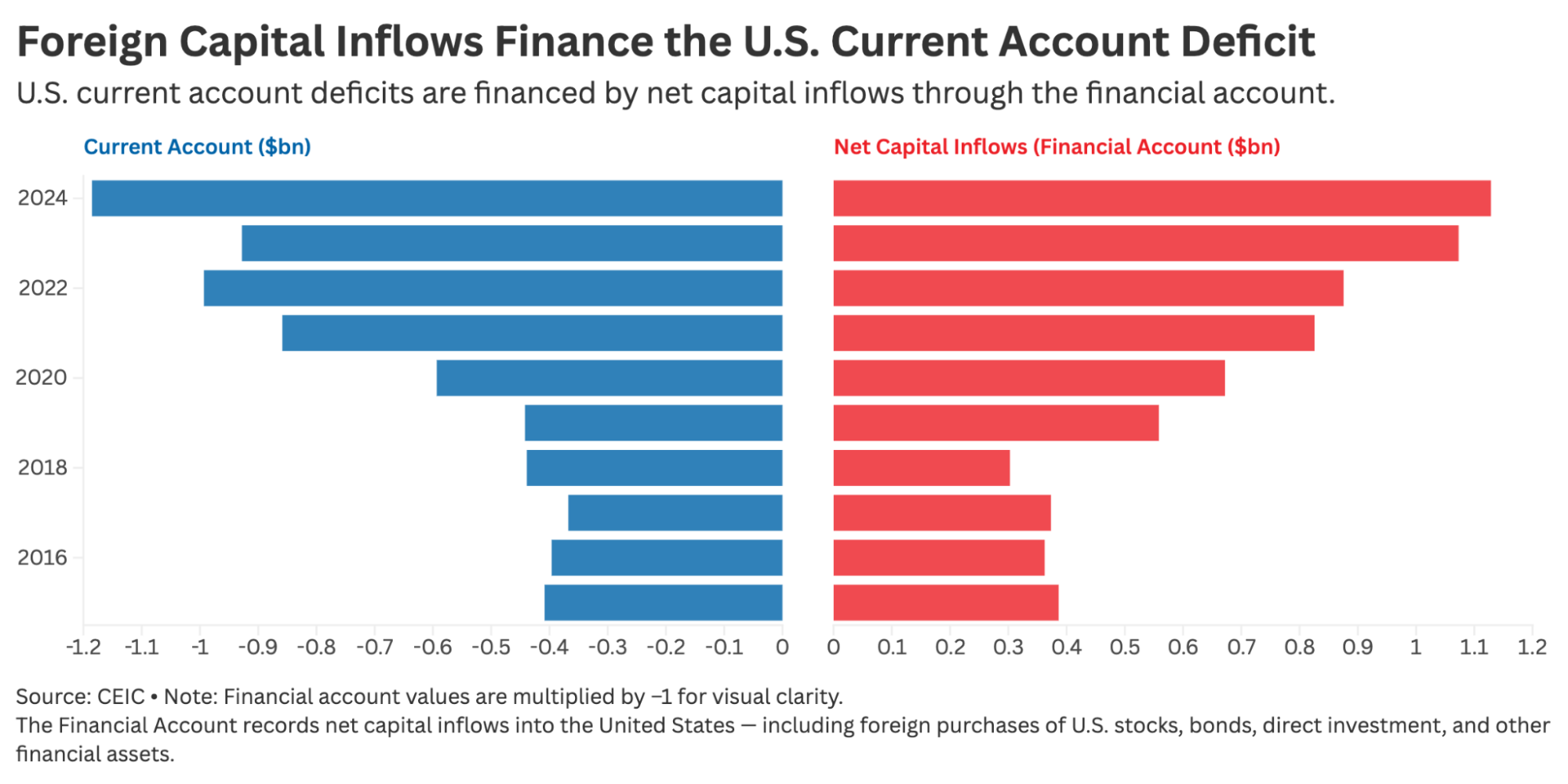

The mechanism operates through capital flows. U.S. current account deficits are financed by net capital inflows recorded in the financial account (Figure 4). When foreign investors purchase U.S. stocks, bonds, and other financial assets, those inflows finance the deficit. Trade imbalances persist not because Americans suddenly prefer imports, but because the United States absorbs excess global savings through its deep and liquid financial markets.

FIGURE 4

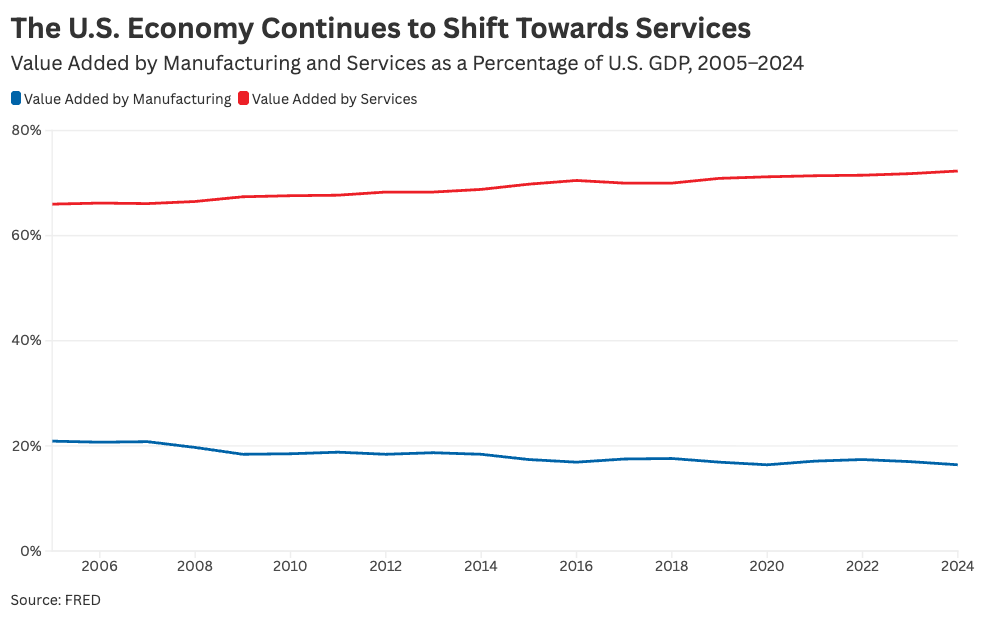

This dynamic has important distributional consequences. Capital inflows are associated with rising asset prices and expanding financial markets, particularly when debt-related flows surge. At the same time, persistent trade deficits alter the composition of domestic production, shifting resources away from tradable sectors and toward non-tradable services, which now accounts for 72% of value added production in the United States (Figure 5).

FIGURE 5

Notably, this shift is not uniform across the services sector. For example, high-productivity tradable services such as finance, software, and professional consulting have expanded alongside lower-wage non-tradable work in hospitality, retail, and healthcare. The concern is not services growth per se, but the erosion of the manufacturing base that historically anchored broad-based wage growth and supported dense regional labor markets.

Because financial asset ownership in the United States is highly concentrated, the gains from globalization accrue disproportionately to capital holders, while the adjustment costs fall on workers in manufacturing and other tradable industries.

The deficit itself is not inherently destabilizing—moderate deficits can be sustainable under the right financial conditions—but the structure through which the deficit operates has widened inequality and weakened the link between domestic production and rising living standards.

How Capital Inflows Affect the Dollar

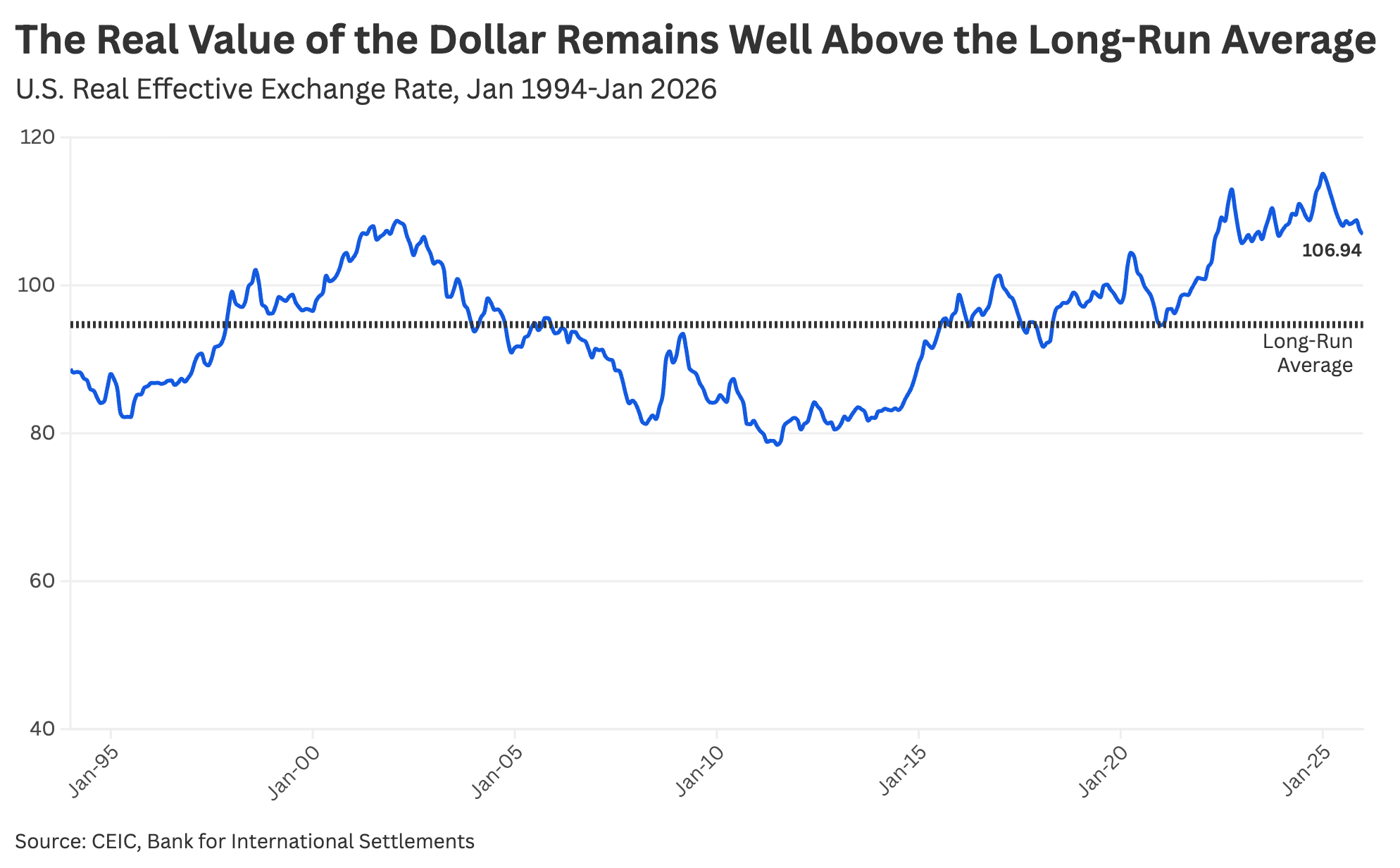

These capital inflows also influence the value of the dollar. When foreign investors purchase U.S. assets, they must first acquire dollars, increasing demand for the currency. Sustained inflows can place upward pressure on the real exchange rate, making imports cheaper and exports less competitive. In this way, capital flows shape trade outcomes not only by financing the deficit, but by affecting the relative price of American goods and services. As long as foreign savings continue to flow into U.S. financial markets, the dollar remains elevated, reinforcing the persistence of the trade deficit. As of January 2026, the real value of the dollar was trading well-above its 30-year average (Figure 6).

FIGURE 6

The historically strong dollar has decimated the U.S. manufacturing sector, acting like a tax on exports and a subsidy on imports. Since its peak in 1980, the U.S. has lost 6.4 million manufacturing jobs. Meanwhile, the trade deficit has more than tripled over the past 25 years, reaching $1.3 trillion at the end of 2025, as previously noted in figure 1.

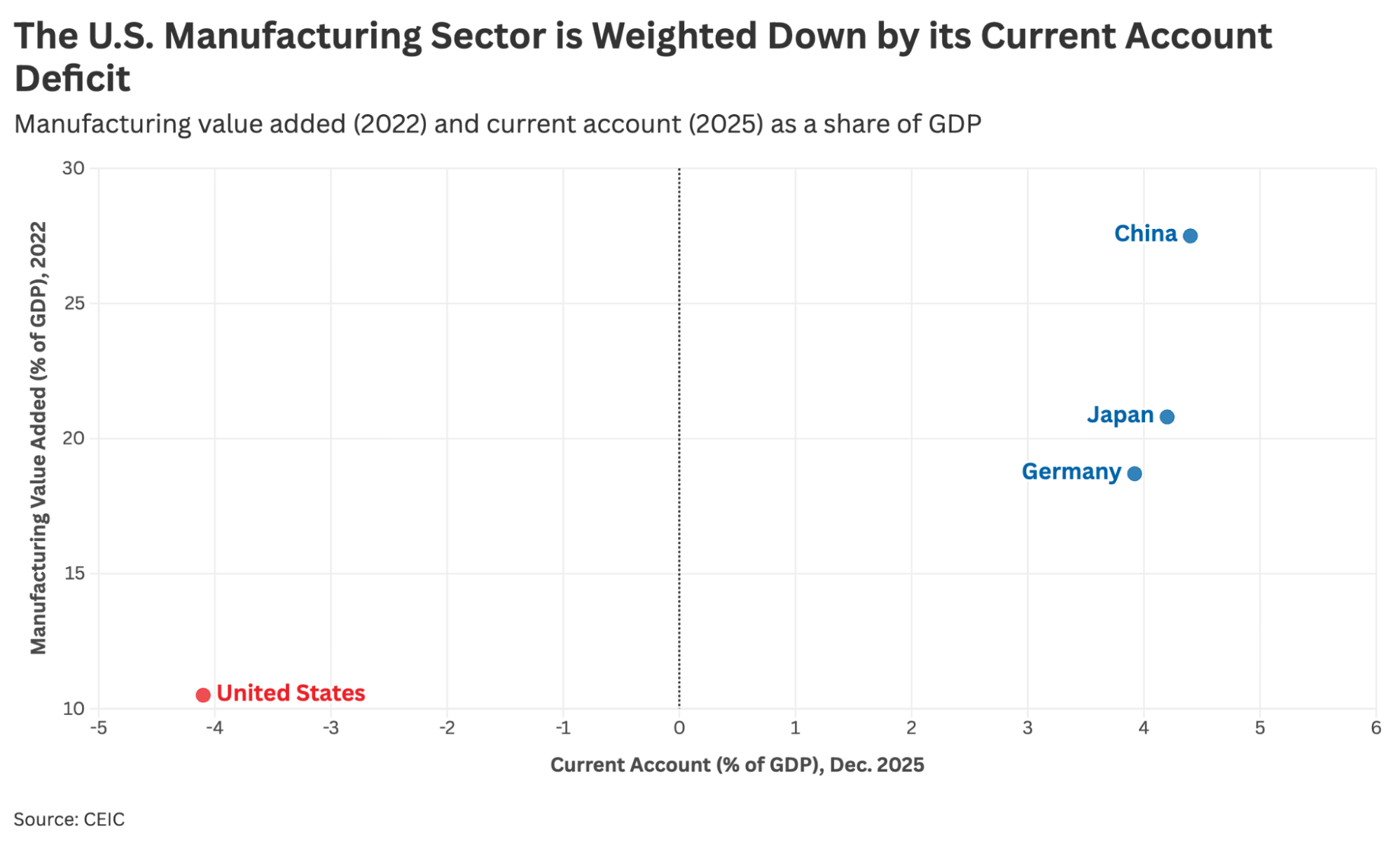

As of 2024, the U.S. current account deficit widened to 3.8%, while manufacturing value-added as a share of GDP has stagnated at roughly 11 percent. In contrast, surplus saving countries like China, Germany, and Japan continue to boast competitive manufacturing sectors, buoyed by their current account surpluses. Manufacturing value-added as a share of GDP is nearly twice as high in each of these economies as it is in the United States (Figure 7).

FIGURE 7

The Shifting Composition of Capital Inflows

The scale of capital inflows is only part of the story. The composition of those inflows matters just as much.

Foreign ownership of U.S. assets falls into three broad categories: foreign-owned stocks (equity), foreign-owned businesses (direct investment), and foreign-owned bonds (debt securities).

- Foreign-Owned Stocks represent portfolio equity holdings—foreign investors owning shares in publicly traded U.S. companies and investment funds. These are market-priced claims on corporate profits and fluctuate with equity valuations.

- Foreign-Owned Businesses reflect direct investment—foreign ownership stakes in U.S. enterprises. This includes both new investments and acquisitions. While direct investment is tied to operating companies, it also represents ownership claims on future earnings and retained profits.

- Foreign-Owned Bonds include Treasury and corporate debt held by foreign investors. These are fixed-income claims that historically made up a larger share of foreign holdings and were often accumulated by foreign central banks as reserve assets.

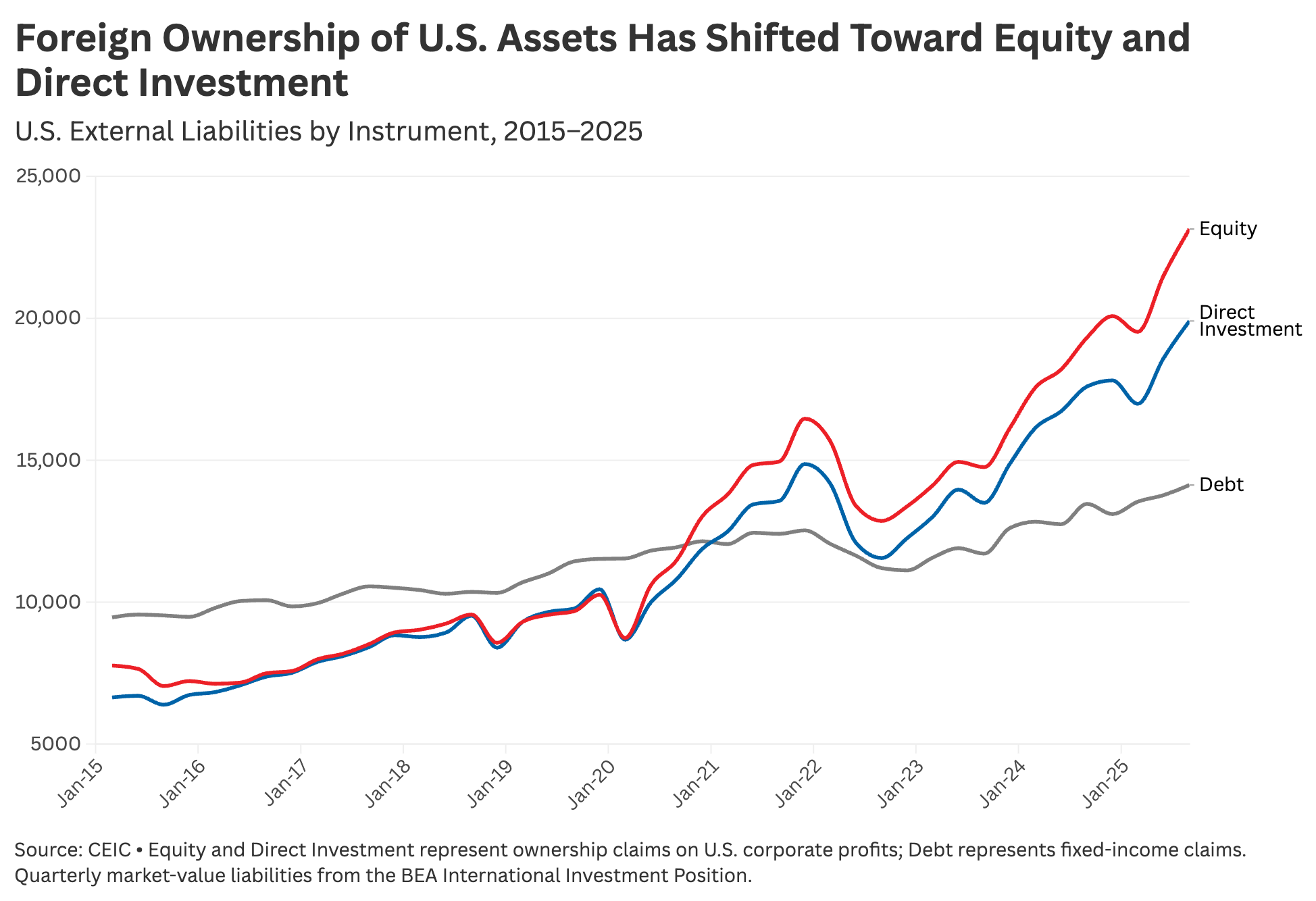

Over the past decade, movements in the U.S. external position have been driven primarily by equity assets rather than debt, increasing the sensitivity of the balance sheet to asset-prices (Figure 8). Further, the share of foreign-owned U.S. assets accounted for by stocks has nearly tripled since the aftermath of the global financial crisis, rising from roughly one-fifth to well over half of foreign portfolio holdings. In other words, foreign exposure to the U.S. is increasingly driven by profit-seeking equity investment rather than reserve-driven Treasury accumulation.

FIGURE 8

This shift has important implications. Debt holdings tend to be policy-driven and relatively stable. Equity investments are valuation-sensitive and more responsive to relative returns and market conditions. As a result, U.S. external financing is now more exposed to asset-market cycles than in the past.

How This Results in a Deteriorating Investment Position

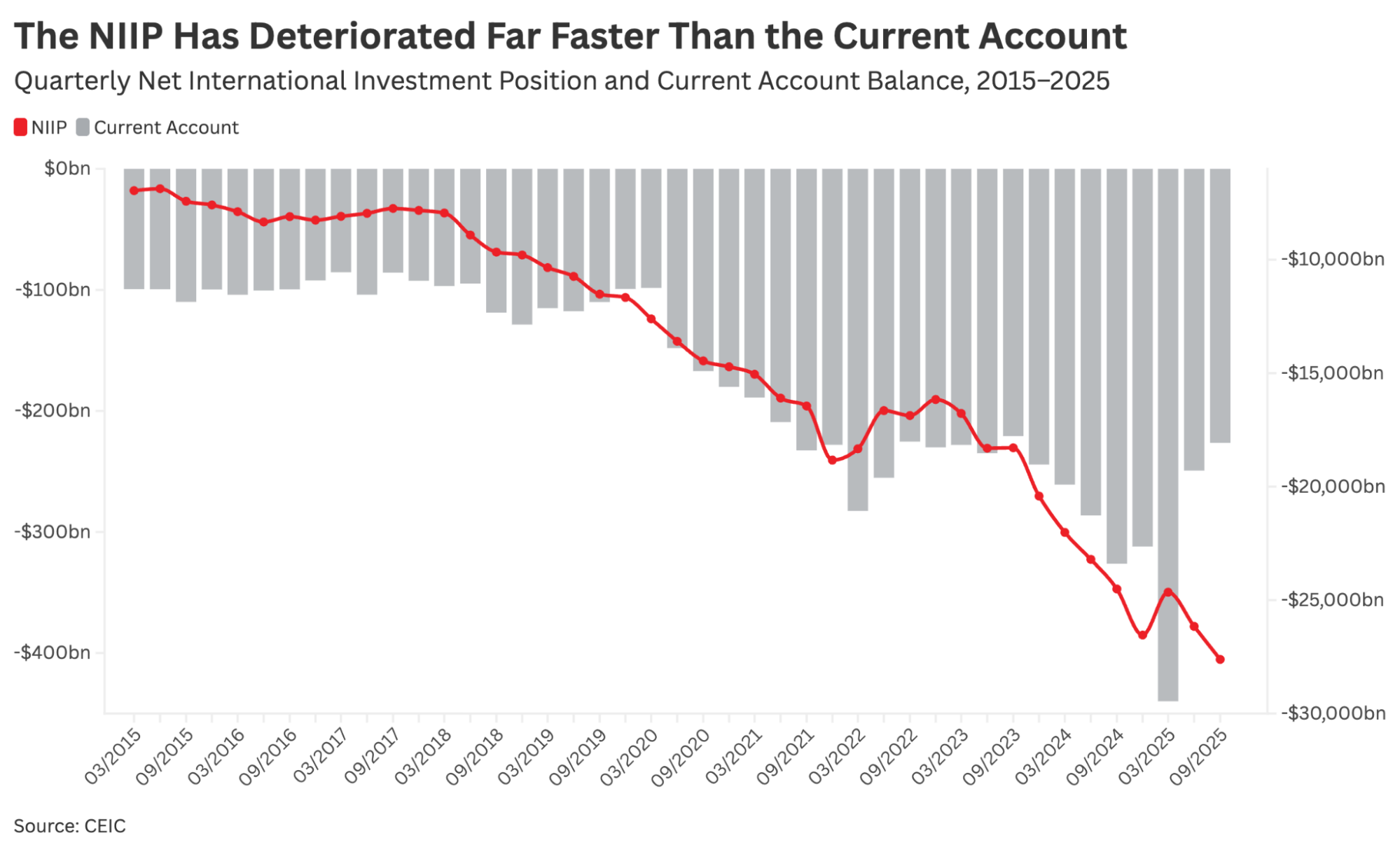

Most critically, the shifting composition of foreign capital inflows results in a deteriorating NIIP, which measures the difference between U.S.-owned foreign assets and foreign-owned U.S. assets. A negative NIIP means foreign investors hold more claims on U.S. assets than Americans hold abroad.

Historically, movements in the NIIP largely reflected the accumulation of current account deficits. However, as research summarized by the Federal Reserve Bank of St. Louis and recent academic work has shown, valuation effects—driven by asset price movements and exchange rate changes—now play a much larger role in shaping the trajectory of the U.S. balance sheet.

As shown in Figure 9, the U.S. NIIP has deteriorated sharply over the past decade, plunging toward negative $28 trillion by 2025. Yet, these declines have become increasingly decoupled from the widening of the current account deficit. The divergence reflects the growing impact of asset-price dynamics, particularly the strong performance of U.S. equity markets relative to foreign markets.

FIGURE 9

When U.S. equity markets outperform the rest of the world, the effect does not stop at higher stock prices. Because foreign investors now hold large stakes in American publicly traded companies and business enterprises, those gains automatically increase the market value of foreign-owned claims on the U.S. economy. The result is a deterioration in the net international investment position driven by rising asset valuations versus surging imports. Even if the trade deficit remains broadly unchanged, the external balance sheet weakens.

How Foreign Equity Ownership Fuels U.S. Inequality

The shift toward foreign equity ownership represents a clear break from the earlier period when valuation dynamics often worked in the United States’ favor. In previous decades, dollar depreciation and stronger returns on U.S. investments abroad helped offset trade deficits. Today the dominant valuation channel runs in the opposite direction. Strong U.S. equity performance raises the market value of foreign-owned assets inside the United States, increasing the value of U.S. external liabilities.

When U.S. equity prices outpace foreign markets, the NIIP deteriorates even if the trade deficit remains broadly unchanged. The mechanism is mechanical: foreigners hold substantial positions in American equities and business enterprises, so rising stock prices increase the value of their claims. No additional borrowing is required. Asset appreciation alone expands foreign ownership of U.S. wealth.

This valuation dynamic is compounded by how capital inflows are structured. Persistent trade deficits require capital inflows, and those inflows increasingly enter through financial markets rather than through direct productive investment. In the third quarter of 2025, the most recent period for which data are available, foreign financial transactions into the United States flowed predominantly through portfolio investment at $486.8 billion, compared to just $115.1 billion through direct investment.

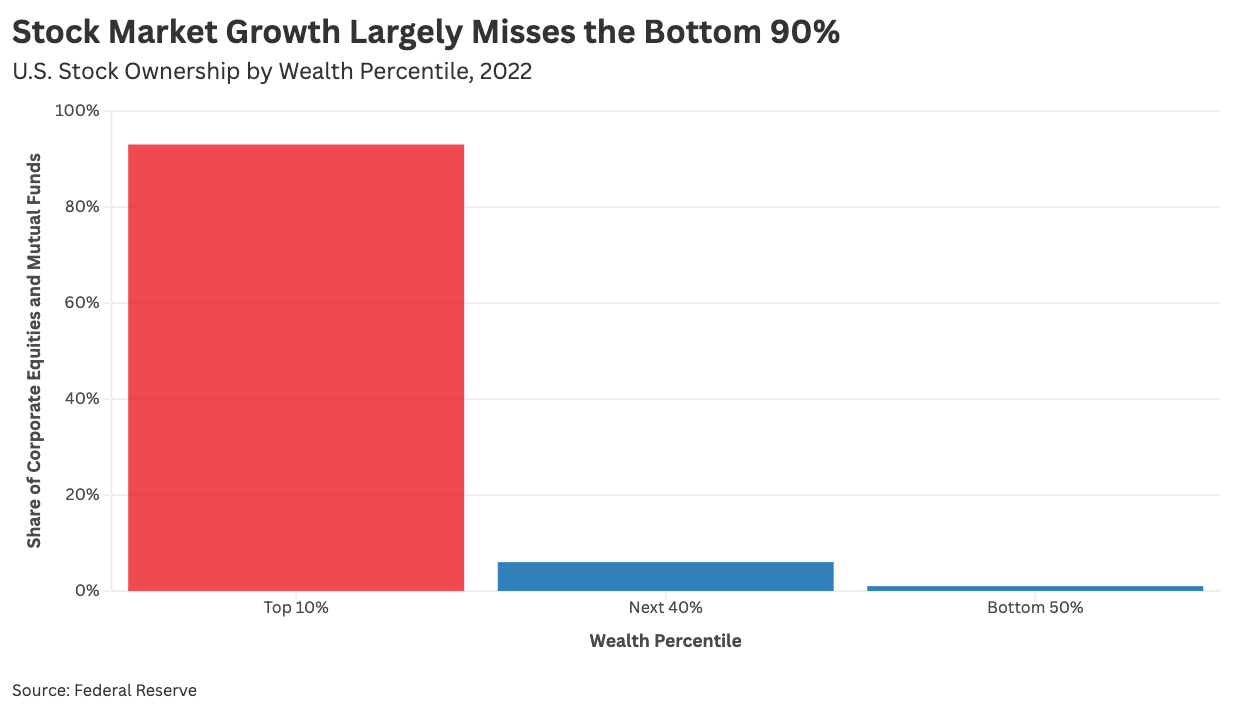

As capital bids up equities, asset gains accrue primarily to those who already own financial assets. Because stock ownership in the United States is highly concentrated, the benefits of market appreciation flow disproportionately to the top decile of households (Figure 10)—and to foreign investors who, according to the U.S. Treasury’s 2024 benchmark survey of foreign portfolio holdings held approximately $17 trillion in U.S. equities as of June 2024—representing roughly one-third of total U.S. equity market capitalization. Meanwhile, wage earners and industrial communities see little direct participation in those gains.

FIGURE 10

The result is a structural imbalance: trade deficits are financed through rising asset valuations, which expand the share of U.S. corporate profits and capital gains that accrue to foreign investors and reinforce domestic wealth concentration at the top. An external position driven more by equity ownership is also more sensitive to market cycles and global portfolio reallocations.

Balancing Trade Deficits via the Capital Account

Because persistent trade deficits are the mirror image of persistent capital inflows, a durable solution must address the capital account—not just goods flows. Tariffs defend strategic industries and can protect specific sectors from mercantilist competition, but they do not alter the financial flows that sustain structural deficits. As long as foreign investors direct substantially more capital into U.S. financial markets than Americans invest abroad, the balance-of-payments identity ensures a current account deficit will follow.

The case for a Market Access Charge

A Market Access Charge (MAC) is a variable, rules-based fee applied to foreign purchases of U.S. financial assets. Unlike a blanket capital control, which restricts flows categorically, a MAC is designed to be calibrated and adjustable—modest under normal conditions, more substantial when inflows surge beyond levels consistent with balanced trade. The mechanism is straightforward: by modestly raising the cost of directing excess savings into U.S. equities and short-term debt, a MAC reduces the financial incentive that draws surplus capital from export-driven economies into American markets in the first place.

This is precisely the instrument the diagnosis calls for. This report demonstrates that the dominant driver of U.S. external imbalance is no longer the flow of goods but the flow of capital—specifically, the surge in portfolio equity investment that inflates asset prices, deteriorates the NIIP through valuation effects, and concentrates the gains of market appreciation among capital holders at home and abroad. A MAC addresses this mechanism at its source rather than at its downstream manifestation in the trade balance.

Design and Scope

Because the objective is to reduce volatility and limit the expansion of foreign claims on U.S. corporate earnings, the MAC should be structured to target short-term portfolio equity purchases and short-duration debt securities—the inflows most sensitive to relative returns and most responsible for asset price inflation. Long-term sovereign debt (i.e. Treasury bonds) and greenfield direct investment should be explicitly exempted to encourage real investment and industrial output. This design preserves the deep and liquid market for U.S. government financing, addressing the most significant objection to capital flow management measures: that reduced foreign demand for Treasuries would raise borrowing costs at a moment of elevated fiscal deficits. By confining the charge to speculative and valuation-sensitive inflows rather than sovereign debt accumulation, the MAC moderates destabilizing surges without disrupting the financing of the federal government.

Revenue and Domestic Reinvestment

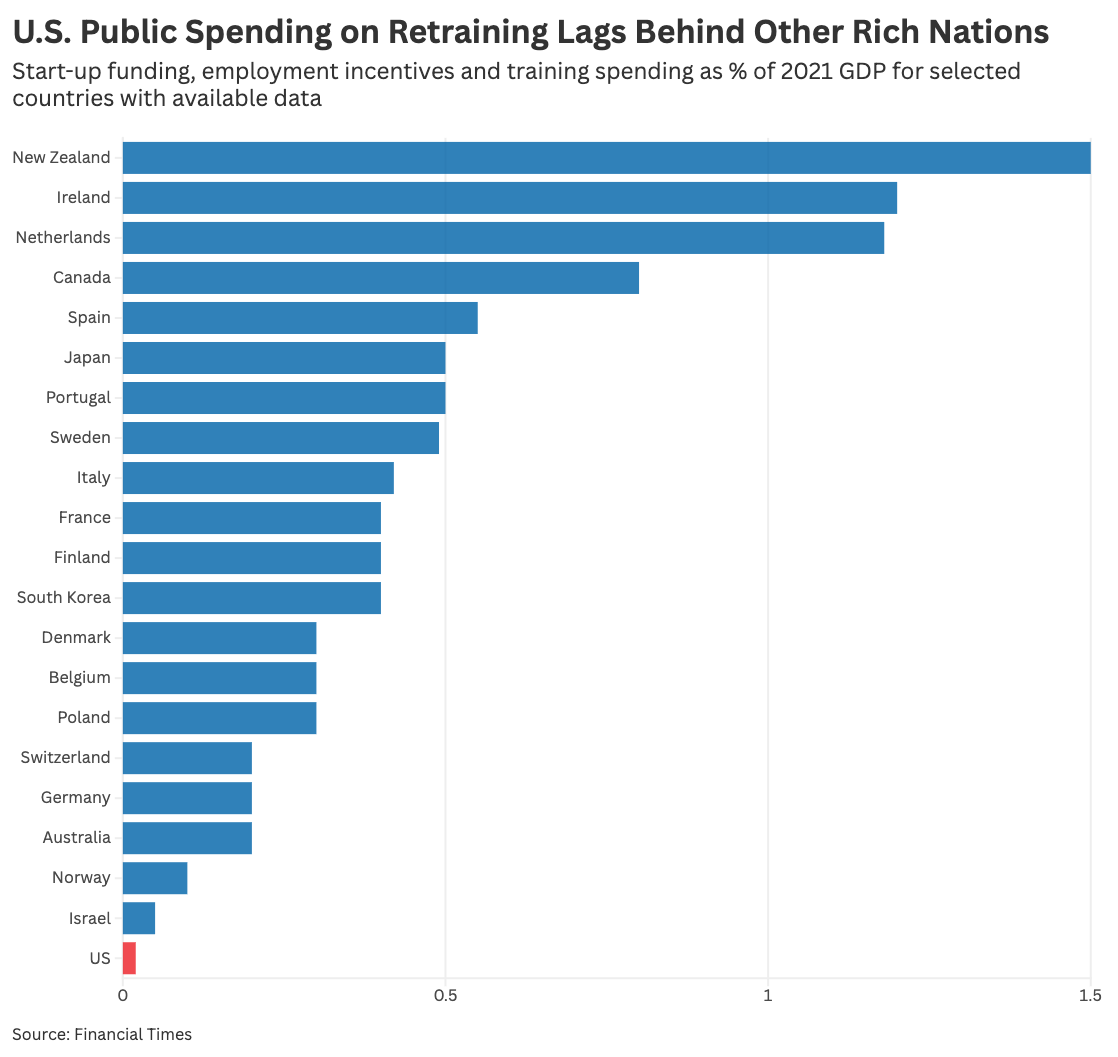

The revenue generated from a MAC represents a meaningful opportunity to redress decades of deindustrialization stemming from failed free trade policies. For example, MAC revenue could be directed towards strategic reinvestment—in advanced manufacturing, artificial intelligence infrastructure, and worker retraining programs. The United States has invested far less than peer economies in supporting workers displaced by trade and deindustrialization (Figure 11). Remedying that failure is integral to a balanced trade agenda.

FIGURE 11

Potential Tradeoffs and Other Considerations

Imposing a MAC presents several tradeoffs. First, moderating capital inflows would likely place some downward pressure on the dollar, raising the cost of imported inputs for U.S. manufacturers that rely on foreign components and capital equipment. Second, reducing foreign demand for U.S. financial assets could place upward pressure on interest rates and increase federal borrowing costs—an especially relevant concern given fiscal deficits near 6% of GDP. Third, moderating portfolio inflows could dampen equity valuations. Finally, any exchange-rate adjustment could influence energy prices, given the dollar’s role in global commodity markets.

Each of these concerns is legitimate, but none is decisive. A modest increase in input costs must be weighed against the long-term objective of restoring competitiveness in domestic production. A somewhat weaker dollar would improve export performance and reduce structural trade imbalances over time. Moreover, revenue from the MAC could be deployed to offset transitional pressures on key sectors or to support domestic investment.

With respect to borrowing costs, the proposed design explicitly exempts long-term Treasury securities, minimizing disruption to sovereign financing markets. Even if some upward pressure on rates materializes, that effect would reflect a reduction in excess foreign savings recycling into U.S. assets. Over time, narrowing the external imbalance reduces reliance on foreign financing, strengthening macroeconomic resilience.

A further concern is substitution: exempting Treasuries could redirect inflows from equities into government bonds, keeping overall demand for dollar assets elevated. Even in that scenario, however, composition matters. Equity inflows expand foreign ownership of U.S. corporate earnings and amplify valuation-driven deterioration of the NIIP. Treasury holdings represent fixed-income claims and do not mechanically increase foreign claims during equity booms. A shift toward more stable debt financing and away from valuation-sensitive equity inflows would reduce volatility and limit the feedback loop between asset inflation and external imbalance—even if aggregate inflows remain substantial.

Finally, while exchange-rate adjustments can influence energy prices at the margin, commodity markets are shaped primarily by global supply and geopolitical conditions. The incremental impact of a calibrated capital-flow measure would likely be modest relative to broader energy dynamics.

In short, a MAC entails tradeoffs. But the status quo also carries costs: persistent trade deficits, rising foreign claims on U.S. earnings, asset-price dependence, and widening inequality. The question is not whether adjustment has consequences—it always does—but whether moderating destabilizing capital inflows improves the long-run balance between financial markets, production, and national income retention.

Conclusion

The U.S. trade deficit is not the result of profligate Americans spending beyond their means. It is the accounting counterpart to persistent capital inflows into the world’s deepest and most liquid financial markets. As long as foreign investors direct more savings into U.S. assets than Americans invest abroad, the balance-of-payments identity ensures that a current account deficit will follow, regardless of the tariff levels.

The deficit itself is not inherently destabilizing. In earlier periods of American development, external deficits financed productive expansion of railroads, factories, and infrastructure that increased national output. Under those conditions, foreign capital complemented domestic investment and strengthened long-term growth.

That is not the structure confronting the United States today. Contemporary deficits are financed largely through portfolio flows that inflate asset prices rather than expand productive capacity. Rising equity valuations increase the share of U.S. corporate profits accruing to foreign investors, deteriorate the net international investment position through valuation effects, and widen domestic inequality without materially strengthening the tradable sector. The issue is less about the existence of a deficit, but rather the mechanism through which it is sustained.

If policymakers seek to rebalance trade and restore productive investment, they must address the capital side of the ledger. A rules-based MAC would moderate excess portfolio inflows, slow the expansion of foreign claims on American corporate earnings, and generate revenue to reinvest in the workers and industries that bore the adjustment costs of the globalization era. Tariffs are a necessary but insufficient instrument. They defend the border of goods trade while leaving the financial channel that sustains structural deficits entirely open.

To reduce the deficit in a durable way, the United States must do more than tariff goods. It must tariff the money.

FOOTNOTES

- The direction of causality between capital flows and the trade deficit is contested. The view advanced here is that capital inflows are the primary driver, as evidenced by the dollar’s persistent overvaluation despite decades of trade deficits. Ordinarily, sustained trade deficits would lower the exchange rate by reducing the demand for the deficit country’s currency. That this has not occurred points to capital flows as the more active variable.

Fiscal deficits also contribute to trade deficits; government borrowing reduces national savings, widens the savings-investment gap, and draws in foreign capital as a result. However, the United States has run persistent trade deficits across periods of both fiscal surplus and deficit, suggesting that the pull of U.S. financial markets on excess foreign savings is a more durable structural driver. This report focuses on that capital-side dynamic and the policy instruments best suited to addressing it.

This is a simplified representation of the balance-of-payments identity. In formal terms, the balance of payments equals zero:

Current Account + Capital Account + Financial Account + Statistical Discrepancy = 0.

The current account includes trade in goods and services, net investment income, and transfers. The financial account (often referred to as capital flows) records cross-border purchases of assets such as foreign direct investment (FDI), portfolio investment, bank flows, and changes in official reserves. For purposes of this discussion, the trade balance is presented as the dominant component of the current account, which is the mirror image of net financial inflows.

While automation accounts for a share of these losses, research by Autor, Dorn, and Hanson estimates that import competition from China alone displaced between 2 and 2.4 million U.S. manufacturing jobs between 1999 and 2011, with the dollar’s persistent overvaluation compounding those losses by eroding export competitiveness.

A MAC structured as described here falls within the capital flow management measures contemplated in the IMF’s 2022 review of its Institutional View on the Liberalization and Management of Capital Flows, which acknowledges that such measures may be appropriate in certain circumstances to address macroeconomic and financial stability risks. This represents a notable shift from the institution’s historically strong preference for open capital accounts, and lends multilateral legitimacy to targeted, rules-based instruments of the kind proposed here.

REFERENCES

“All Employees, Manufacturing.” FRED, Federal Reserve Bank of St. Louis. February 11, 2026. https://fred.stlouisfed.org/series/CEU3000000001.

“America the Tax Haven and Its Trade Deficits.” Tax Notes Federal, August 19, 2024. https://www.taxnotes.com/tax-notes-federal/tax-policy/america-tax-haven-and-its-trade-deficits/2024/08/19/7kkjf.

Autor, David H., David Dorn, and Gordon H. Hanson. “The China Syndrome: Local Labor Market Effects of Import Competition in the United States.” American Economic Review 103, no. 6 (2013): 2121–68. https://doi.org/10.1257/aer.103.6.2121.

Bureau of Economic Analysis. “U.S. International Investment Position, 3rd Quarter 2025.” BEA 26–03. January 16, 2026. https://www.bea.gov/news/2026/us-international-investment-position-3rd-quarter-2025.

“Blame Higher U.S. Equity Prices for Recent Moves in U.S. External Liabilities.” Federal Reserve Bank of Dallas, November 12, 2024. https://www.dallasfed.org/research/economics/2024/1112.

Carnegie Endowment for International Peace. “Time to Reset the U.S. Trade Agenda.” May 20, 2024. https://carnegieendowment.org/research/2024/05/time-to-reset-the-us-trade-agenda.

Coalition for a Prosperous America. “CPA Welcomes Trump Action to Restrict China’s Access to U.S. Capital and Investment.” February 24, 2025. https://prosperousamerica.org/cpa-welcomes-trump-action-to-restrict-chinas-access-to-u-s-capital-and-investment/.

Coalition for a Prosperous America. “Keynes’ Support for Broad Tariffs.” October 28, 2024. https://prosperousamerica.org/keynes-case-for-tariffs/.

Coalition for a Prosperous America. “U.S. Manufacturing’s Shrinking Share of GDP and How to Catch Up.” November 8, 2024. https://prosperousamerica.org/u-s-manufacturings-shrinking-share-of-gdp-and-how-to-catch-up/.

Economic Policy Institute. “Adding Insult to Injury: How Bad Policy Decisions Have Amplified Globalization’s Costs for American Workers.” Accessed March 2, 2026. https://www.epi.org/publication/adding-insult-to-injury-how-bad-policy-decisions-have-amplified-globalizations-costs-for-american-workers/.

Ghizoni, Sandra Kollen. “Creation of the Bretton Woods System.” Federal Reserve History. Accessed March 2, 2026. https://www.federalreservehistory.org/essays/bretton-woods-created.

International Monetary Fund (IMF). “Review of the Institutional View on the Liberalization and Management of Capital Flows.” March 29, 2022. https://www.imf.org/en/publications/policy-papers/issues/2022/03/29/review-of-the-institutional-view-on-the-liberalization-and-management-of-capital-flows-515883.

IMF. Tradables, Nontradables, and the U.S. Productivity and Inequality Divide. IMF Working Paper WP/2025/155. Washington, DC: International Monetary Fund, 2025. https://www.elibrary.imf.org/view/journals/001/2025/156/article-A001-en.pdf.

Investopedia. “What Is the Balance of Payments (BOP)?” Accessed March 2, 2026. https://www.investopedia.com/insights/what-is-the-balance-of-payments/.

Pettis, Michael. “Bad Trade.” American Compass, October 7, 2022. https://americancompass.org/bad-trade/.

Pettis, Michael. “Do Consumers Benefit from Cheaper Imports?” FT Alphaville. Financial Times, August 13, 2025. https://www.ft.com/content/89110b66-153c-47a4-a3d4-851be3c0fc93.

Ramirez, Carlos Hernan. “The Post-War Evolution of Globalisation and International Order: From Liberal to Neoliberal International Order.” Global Society 40, no. 1 (2026): 44–72. https://doi.org/10.1080/13600826.2025.2470838.

Tax Policy Center. “Who Owns US Stock? Foreigners and Rich Americans.” October 20, 2020. https://taxpolicycenter.org/taxvox/who-owns-us-stock-foreigners-and-rich-americans.

U.S. Department of the Treasury, Federal Reserve Bank of New York, and Board of Governors of the Federal Reserve System. “Foreign Portfolio Holdings of U.S. Securities as of June 28, 2024.” February 28, 2025. https://home.treasury.gov/news/press-releases/sb0037.

Voxeu/CEPR. “Capital Inflows and Booms in Asset Prices: Going beyond the Current Account.” December 7, 2013. https://cepr.org/voxeu/columns/capital-inflows-and-booms-asset-prices-going-beyond-current-account.

Waraich, Irza, and Trevor Jackson. “The Ungovernable Economy.” The New York Review of Books, January 25, 2025. https://www.nybooks.com/online/2025/01/25/the-ungovernable-economy-trevor-jackson/.

White House. “America First Investment Policy.” February 21, 2025. https://www.whitehouse.gov/presidential-actions/2025/02/america-first-investment-policy/.

“Why the Dollar May Have Much Further to Fall.” The Economist, February 5, 2026. https://www.economist.com/finance-and-economics/2026/02/05/why-the-dollar-may-have-much-further-to-fall.

Wolf, Martin. “The Old Global Economic Order Is Dead.” Financial Times, May 6, 2025. https://www.ft.com/content/49e38ee8-f37e-47da-8ee4-1631175d2224.