KEY POINTS

- Solar power deployment has increased substantially in recent years, despite claims that tariffs would substantially slow deployment.

- The strong growth in U.S. solar deployment and total demand has even been outpaced by the growth of imports.

- Trade measures, including new tariffs on imports from Southeast Asia, are essential to support the U.S. industry, in the face of duty circumvention and foreign government subsidies.

- Tariffs would have a minimal impact on the rate of U.S. solar deployment given that solar module/panel cost is only a small portion of the total cost of deployment.

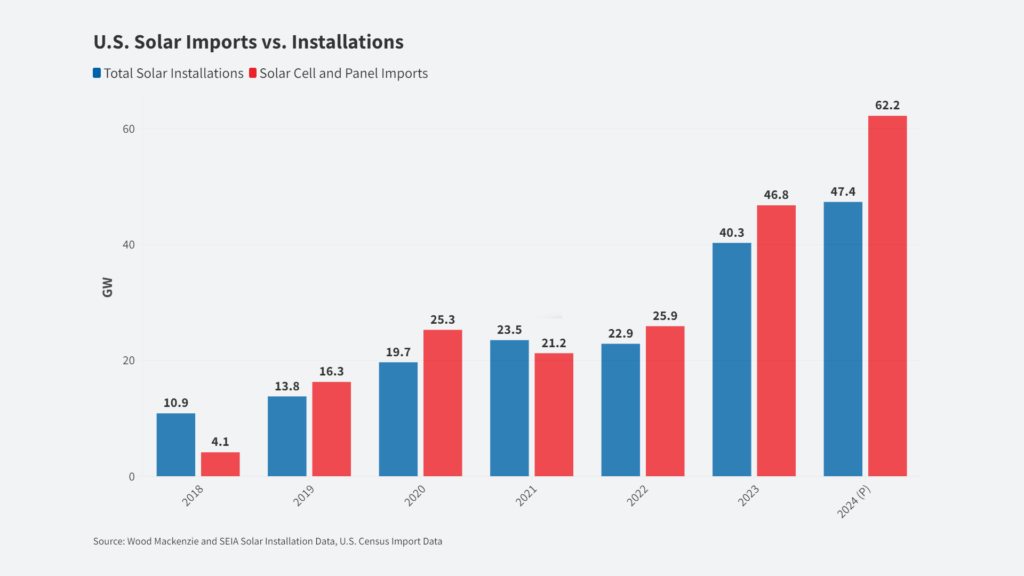

Solar Imports Outpacing Total Installations

Every solar tariff in the past 10 years has been met with opposition and claims that it will slow deployment of solar technology in the United States. However, despite this constant wolf crying, solar tariffs have never slowed down solar deployment. This has simply never been the case.

In 2018, after the Trump Administration implemented a tariff on solar cells and modules starting at 30%, various groups came forward claiming this would have a massive negative impact on U.S. solar deployment.

One group, GTM Research, lowered their forecasted U.S. solar installations by 11% as a result of the new tariff. GTM Research projected that the tariffs would reduce solar deployments “to a cumulative 61.3 gigawatts of solar deployed over the next five years compared to an original projection of 68.9 gigawatts, for a 7.6-gigawatt reduction in installed solar PV capacity between 2018 and 2022.”

In reality, solar installations blew past even GTM Research’s original pre-tariff forecast. As shown in Figure 1, solar installations between 2018 and 2022 reached 90.8 GW, 32% higher than GTM Research’s original forecast and 48% higher than GTM Research’s tariff forecast.

FIGURE 1:

The tariffs did not slow solar deployment in the United States whatsoever. Solar deployment has continued to surge since the tariffs were implemented. According to Wood Mackenzie, total 2023 solar energy installations reached 40.3 GW, and installations during Q1 2024 were 11.8 GW (an all-time high).

If anything, the tariffs did not go far enough to leave room for a strong domestic solar industry. The strong growth in solar deployment is being increasingly outpaced by solar imports, which are harming domestic solar producers. As shown in Figure 1, U.S. Census data shows solar imports are surging far above solar deployment levels.

If this continues, domestic U.S. producers will increasingly be crowded out of the market and the U.S. will become increasingly dependent on imports for its solar energy supply and deployment. This would be a tragedy, as more than a dozen U.S. and non-Chinese companies have announced or already begun building solar module production facilities in the U.S.

The U.S. is losing control of its solar energy supply and production, and this loss has been driven by the circumvention of U.S. duties and massive subsidies for Chinese solar manufacturers. In order to address these massive issues, additional trade measures such as tariffs and quotas are needed.

Solar Modules Only a Fraction of Deployment Costs

U.S. trade policy needs to step up to protect and support the domestic solar industry. The rapidly rising imports are squeezing the domestic solar industry and hindering the development of domestic solar production.

Trade measures such as tariffs and/or quotas on solar panel imports would benefit the U.S. solar market immensely by encouraging U.S. solar production, strengthening the U.S. solar supply chain, and lessening the dependence on heavily subsidized foreign manufacturers.

However, despite tariffs having never slowed down solar deployment before. Opposition continues to claim any tariffs will make solar deployment substantially more expensive, even for cases involving antidumping investigations intended to protect against below-market prices and foreign government subsidies.

One estimate from a solar developer group projects that if the current antidumping investigation against Southeast Asian solar producers were concluded at the current alleged dumping duty rates (70-270%), this would “increase the all-in cost of U.S. module assembly from 22 cents per watt to 32 cents per watt”. On its face, this estimated increase in the cost of solar module assembly (45%) seems extremely high. However, like most analyses warning that tariffs will slow deployment, this analysis fails to account for all the other costs that go into solar deployment. Solar module costs only account for a small portion of the overall solar deployment cost.

According to the National Renewable Energy Laboratory (NREL), solar module costs are only 12.6% of the total average solar installation cost in 2023. As shown in Figure 2, the vast majority of the costs of solar installation and deployment are outside of the final solar module cost. About half the costs of installation are administrative costs, which include customer acquisition, permitting, interconnection, and administration/overhead costs. Moreover, the module is not even the majority of the hardware cost. Hardware such as racking and electrical infrastructure account for even more of the end cost than the module itself.

FIGURE 2:

Based on this cost breakdown from the National Renewable Energy Laboratory (NREL), even if the 45% U.S. module cost increase turns out to be true, this would only result in a negligible 6% increase in the total solar installation cost. A change at this level would have no impact on solar deployment.

According to the U.S. Energy Information Administration, solar is already one of the cheapest forms of energy available in the United States for new deployment, with an average cost of electricity far below its rivals. The EIA estimates the average cost of electricity from new solar facilities to be $23.22 per megawatt-hour. As shown in Figure 3, this makes solar 25% cheaper than onshore wind, 67% cheaper than advanced nuclear, and 74% cheaper than ultra-super critical coal. Even if a 6% increase in the price of solar installation were to occur as a result of tariffs (which is far from certain), it would have a negligible impact on deployment given that solar energy costs are already far below other sources.

FIGURE 3:

Furthermore, tariffs and other trade measures would benefit the domestic solar industry through increased investments and increased solar production domestically, as opposed to the current solar investments largely going to foreign producers. Over the last twenty years, the cost of solar power has steadily declined due to advances in photovoltaic technology and the growing efficiency of the industry. If the U.S. industry were allowed to expand, a small increase in solar module costs would be only temporary as the cost-reduction curve would continue to reduce the cost per module and cost per watt.

Conclusion

While solar tariffs would have a negligible impact on final installation prices and the rate of deployment, they would provide a substantial and possibly life-saving boost to the domestic U.S. industry and domestic U.S. production of solar manufacturing equipment. Additional tariffs or quotas to plug the holes in the current trade policies would help protect and encourage investment in U.S. solar, increase employment, and help make the United States more energy-independent. The U.S. needs a secure energy supply chain and robust domestic production, and any increase in prices would be small and temporary and soon disappear.